Yritys tai ala ei ole itselleni ei ole kovin tuttu, mutta tutustuin yhtiöön lisää eri tavoin. ![]()

Lyhyesti:

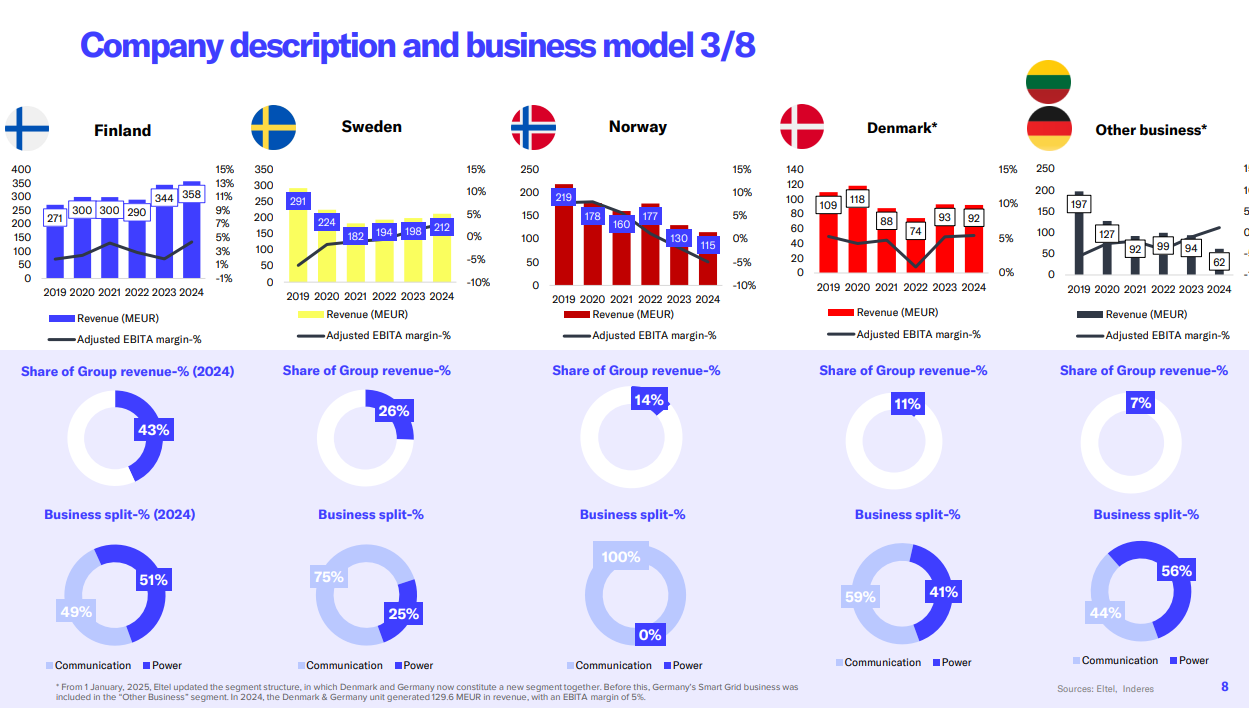

Eltel on teknisten palveluiden tarjoaja energian ja viestintäsektorilla. Suurin painopiste on siirtojärjestelmien, infrastruktuurin ja verkkojen korjauksessa sekä kehittämisessä. Liiketoimintaa harjoitetaan useimmilla liiketoiminta-alueilla globaalisti. Suurimmat toiminnot ovat Pohjoismaissa. Yritys perustettiin vuonna 2004, kun Swedia Networks ja Eltel Networks fuusioituivat. Pääkonttori sijaitsee Tukholmassa.

Yleistä asiaa lisää ja sijoittajan näkökulmaa

Eltel on johtava palveluntarjoaja kriittisille energia- ja viestintäinfrastruktuureille Pohjoismaissa. Yritys on kamppailut pitkään kannattavuutensa kanssa, ja sen nykyinen strategia keskittyykin kestävän kannattavan kasvun rakentamiseen. Eltel on mennyt oikeaan suuntaan, mutta käänteen varmistuminen ja toteutuminen voi viedä aikaa. Inderes odottaa yhtiön parantavan kannattavuuttaan asteittain tulevina vuosina.

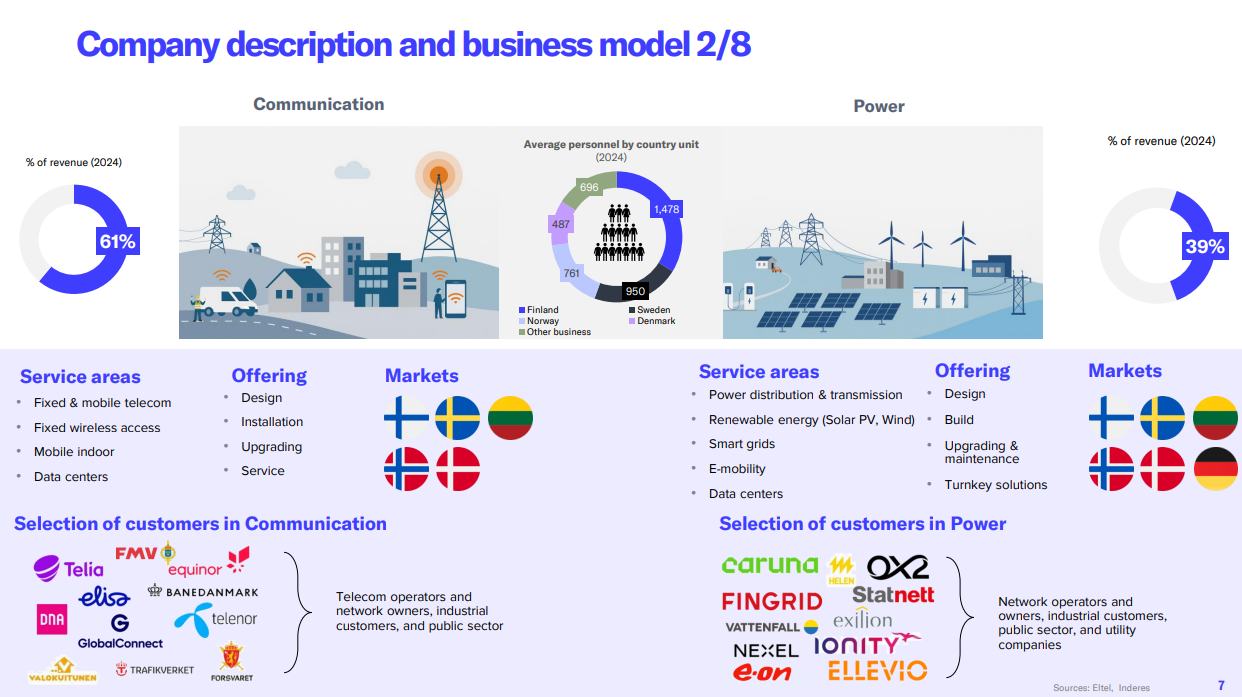

Eltelin tärkeimmät palvelut sisältävät sähköverkkojen ylläpidon, päivittämisen ja projektityöt kansallisille siirtojärjestelmän operaattoreille sekä jakeluverkkojen omistajille, samoin kuin viestintäverkkojen ylläpitopalvelut. Yrityksen päämarkkinat ovat “kovin kilpailtuja”, mikä on johtanut perinteisten liiketoimintojen tuotteistumiseen. Eltel onkin kehittänyt palvelutarjontaa ja hinnoittelumalleja yksilöllisemmän liiketoimintamallin luomiseksi ja pyrkii laajentamaan asiakaskuntaa myös uusille alueille, kuten mm. vihreään energiaan. Lisäksi Eltel toimii Saksassa, Liettuassa ja toistaiseksi Puolassa, mutta on ilmoittanut myyvänsä Puolan liiketoiminnan, ja kaupan odotetaan toteutuvan Q2’24 aikana.

Ainakin Inderes odottaa Eltelin parantavan marginaalejaan strategisten aloitteiden avulla tulevina vuosina. Yrityksen historia on ollut haastavaa, niin viime vuosien haasteet, kuten inflaatio ja asiakkaiden investointien lykkääntyminen ovat rasittaneet kannattavuutta. Eltelin strategiat näyttävät olevan järkeviä, mutta kuten todettua käänteen toteutuminen vienee aikaa.

Orgaanisen kasvun odotetaan olevan alhaisissa yksinumeroisissa luvuissa seuraavina vuosina, mutta kannattavuudelta odotetaan enemmän. Odotuksia ja käännettä on osin hinnoiteltu osakkeen hintaan sisälle, joten halvaksi osaketta ei ehkä voida sanoa.

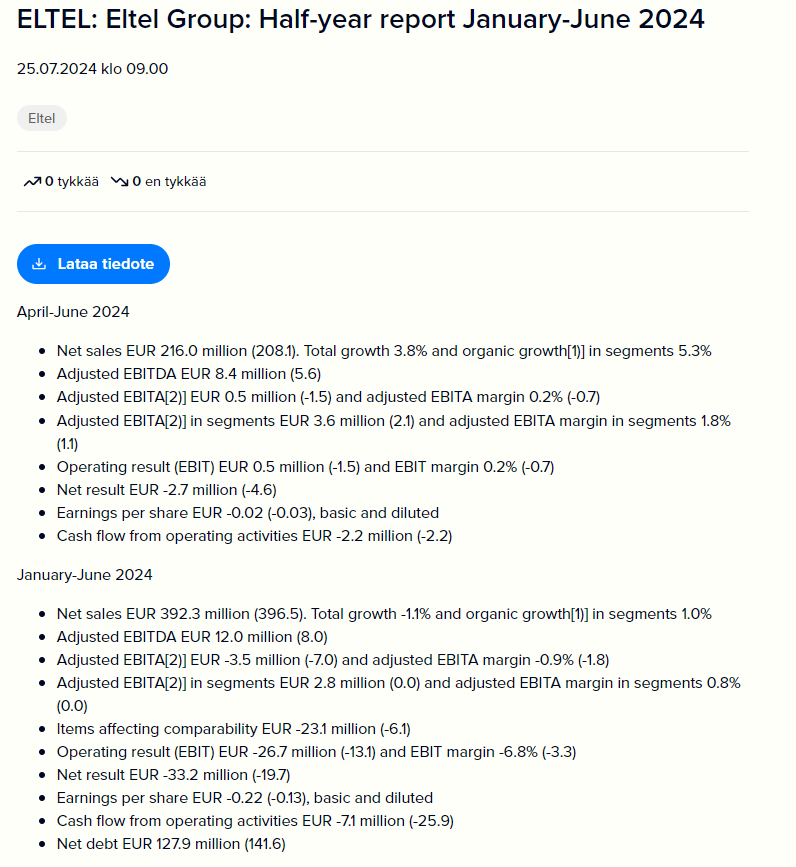

Sopivasti tuli Q2-tulos, joten laitetaan sen tiedot tähän: