@christoffer.jennel on antanut ennakkokommenttinsa, kun Eltel julkaisee Q3-tuloksensa torstaina.

Odotamme Ruotsin julkisten infrastruktuurihankkeiden jatkavan hyvää kehitystä ja Suomen Power-segmentin kasvavan vakaasti. Yhdistettynä myydyn Puolan liiketoiminnan negatiivisten vaikutusten puuttumiseen ja valuuttamyötätuuliin odotamme näiden tekijöiden tukevan vankkaa liikevaihdon kasvua Q3:lla. Jatkuvan strategian toteuttamisen ja kannattavuuteen keskittymisen ohella ennustamme jälleen yhtä vuodentakaista parempaa EBITA-kannattavuutta. Kuten aina, johdon kommentit markkinanäkymistä ja strategian toteutuksesta ovat raportin keskeisiä kiinnostuksen kohteita.

Christoffer Jennel on tehnyt uuden yhtiöraportin Q3:n jäljiltä.

Vaikka Eltelin Q3-liikevaihto jäi ennusteemme alapuolelle, kannattavuus oli hyvin linjassa odotustemme kanssa. Pidämme Q3-kannattavuutta, alhaisemmasta liikevaihdosta huolimatta, merkkinä korkeammasta resilienssistä ja lisätodisteena siitä, että Eltelin operatiiviset ja kaupalliset tehostamistoimenpiteet tuottavat tuloksia. Uusien liiketoiminta-alueiden jatkuva hyvä kehitys (24 % Q3:n sopimusarvosta) tukee mielestämme myös kannattavuuden paranemista jatkossa. Eltelin kaltaisessa käänneyhtiössä kannattavuuden kehitys on edelleen keskeistä sijoituscasessamme, sillä se on tärkein kestävän arvonluonnin ajuri. Mielestämme yhtiö on ottanut selkeitä ja johdonmukaisia askelia oikeaan suuntaan ja on nyt paremmin asemoitunut ylläpitämään ja jatkamaan kannattavuutensa parantamista. Q3-raportin valossa olemme kuitenkin tarkistaneet liikevaihtoennusteitamme alaspäin, mutta pitäneet marginaalit pitkälti ennallaan. Tuloksen jälkeisen osakekurssin laskun jälkeen uskomme nykyisen arvostuksen tarjoavan hyvän riskikorjatun tuottopotentiaalin seuraavan 12 kuukauden aikana. Toistamme siis lisää-suosituksemme ja nostamme tavoitehintamme 9,9 SEK:iin (oli 9,7 SEK).

Hei kaikki! Jesper Ruotsin yhteisöstä täällä. Nauhoitimme tänään haastattelun analyytikko @christoffer.jennelin kanssa päivitetystä Eltel-analyysistämme Q3-raportin jälkeen. Joten katsokaa se, tosin ruotsiksi. Jos teillä on kysyttävää Christofferilta, voitte kirjoittaa ne tähän!

Tässä on Christofferin ennakkokommentit, kun Eltel kertoo Q4-tuloksestaan perjantaina 13.2.

Odotamme raportin korostavan jatkuvaa marginaalien kestävyyttä huolimatta vaihtelevasta kysyntäympäristöstä eri maantieteellisillä alueilla. Vaikka perinteiset televiestintämarkkinat pysyvät heikkoina, erityisesti Norjassa ja Suomen kuitu kotiin (FTTH) -segmentissä, odotamme Power-segmentin ja julkisten infrastruktuurihankkeiden kasvun tukevan liikevaihtoa. Keskeisiä painopisteitä vuosineljänneksellä ovat kassavirran kausiluonteinen huippu, Norjan kannattavuuden palautumisen kestävyys ja tilauskertymä.

Tässä on Christofferilta uusi yhtiöraportti Eltelistä Q4-tuloksen jäljiltä.

Eltel päätti vuoden 2025 vahvasti, sillä Q4:n liikevaihto oli 4 % ennusteitamme korkeampi ja kannattavuus parani edelleen vertailukaudesta kymmenennen peräkkäisen vuosineljänneksen. Tärkeää on, että Norja jatkoi paluutaan kannattavuuteen toisen peräkkäisen vuosineljänneksen, mikä on ratkaisevan tärkeää koko käännetarinan kannalta. Uskomme, että uusien liiketoiminta-alueiden jatkuva kehitys (11 % tilikauden 2025 liikevaihdosta vs. 4 % viime vuonna) yhdistettynä osoitettuihin operatiivisiin ja kaupallisiin parannuksiin tukee kannattavuuden paranemista. Johto ilmaisi luottavansa 5 %:n oikaistun EBITA-kannattavuustavoitteen saavuttamiseen 12–18 kuukauden kuluessa, antaen aikataulun ensimmäistä kertaa sitten sen peruuttamisen Q3’24:llä. Vaikka tämä on rohkaisevaa, pysymme varovaisempina ja uskomme, että todistustaakka on Eltelillä sen osoittamiseksi, että tämä on saavutettavissa. Nostamme kuitenkin vuosien 2026-27e liikevaihtoennusteitamme 1–2 %, mikä heijastaa ensisijaisesti Ruotsin vahvempaa kehitystä, samalla kun pidämme kannattavuusennusteemme suurelta osin ennallaan.

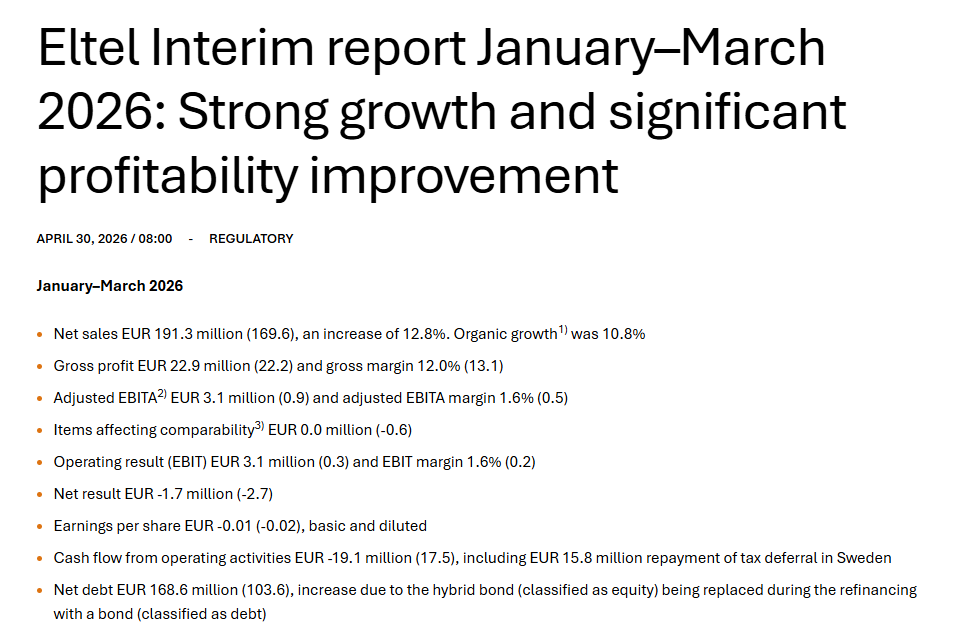

Tässä on Christofferilta ennakkokommentit, kun Eltel julkaisee Q1-tuloksensa torstaina 30.4.

Odotamme raportin osoittavan yhtiön positiivisen kannattavuustrendin jatkuvan, mikä olisi yhdestoista peräkkäinen vuosineljännes, jolloin kannattavuus paranee edellisvuodesta. Vaikka Q1 on Eltelille kausiluonteisesti hiljaisin ajanjakso sääolosuhteiden vaikuttaessa rakennustoimintaan, ennustamme Ruotsin markkinoiden vahvan kehityksen ja uusien liiketoiminta-alueiden, kuten datakeskusten ja aurinkosähkön, kasvun tukevan maltillista liikevaihdon kasvua. Raportissa keskitymme Norjan käänteen kestävyyteen, uusien liiketoimintasegmenttien kehitykseen sekä laadullisiin kommentteihin markkinanäkymistä neljänneksen turbulentin geopoliittisen tilanteen jälkeen.

Tässä on ABG:n ennakkoajatukset Eltelin Q1:stä ajatellen.

We expect Eltel to report Q1 net sales of EUR 178m, up 5% y-o-y, of which +3% organic. We expect to see mixed demand signals from Eltel’s end-markets, with Communications expected to remain subdued, especially in Norway, while the order momentum in Power seems to be clearly better. Profitability should improve y-o-y, partly due to more contracts rolling over to new, better commercial terms as of 2026, and partly due to growth in “new business areas”, which according to the company are also margin-accretive. However, we remind that Q1 is a seasonally small quarter, and we therefore see the y-o-y trend as more important than the absolute EBITA number. That being said, we model an adj. EBITA of EUR 2.0m (up from 0.9m in Q1’25), for a margin of 1.1% (0.5%).

Christoffer on antanut kommenttinsa, kun Eltel on tehnyt 60 millin sopparin Ellun kaa.

Eltel tiedotti uudesta puitesopimuksesta suomalaisen telekommunikaatiojohtajan Elisan kanssa, jonka arvo on noin 60 MEUR. Suhtaudumme sopimukseen positiivisesti, sillä se rakentuu olemassa olevan strategisen suhteen päälle ja lisää näkyvyyttä Eltelin Suomen toiminnoille vuoteen 2029 asti. Pidämme ennusteemme ennallaan ennen tänään myöhemmin julkaistavaa Q1-raporttia.

Tätä on tullut osteltua kohtalainen positio kuluneen vuoden aikana (kasilla alkavalla keskihinnalla) ajatuksella, että markkina kehittyy kohdemarkkinoilla, eli Pohjoismaissa, sähköistymisen, datakeskusten ja muiden trendien vuoksi suotuisasti seuraavat vuodet, vaikka communication-puoli olisikin toistaiseksi enemmän päivitys- ja ylläpitotyyppistä. Toinen peruste on sitten tuo firman mahdollinen turnaround kannattavuuden suhteen. Johdon osakeostot ovat antaneet lisäluottoa käänteeseen ja mielestäni molemmat teesit alkaa viimeistään tämän tuloksen (mutta myös aiempien kvartaalien) perusteella näyttää erittäin todennäköisiltä. Yhtiöhän ei ole kovin seksikäs ja sitä ei tunnu seuraavan juuri kukaan esim. tämän ketjun hiljaisuuden perusteella. Ja tämä varmaan osin pitänyt osakurssin maltillisena.

Kyllä nyt kelpaa ja varsinkin tämä toimitusjohtajan kommentti lämmittää: “In Q4, I stated that I was confident that we would reach our profitability target of 5% within 12 to 18 months’ time and now, one quarter later, the positive start of 2026 strengthens my belief in this.”

Josko tässä kohta aletaan tehdä pientä re-ratingia.

Christoffer on tehnyt uuden yhtiöraportin Eltelin Q1:n jälkeen

Eltelin Q1’26-raportti ylitti selvästi ennusteemme sekä ylä- että alarivin osalta, mikä osoittaa, että käänne ei ainoastaan pysy ennallaan, vaan etenee ennustamaamme nopeammin. Vaikka Q1 on kausiluonteisesti hiljaisin jakso, Eltel saavutti 11 %:n orgaanisen kasvun ja odotettua vahvemman kannattavuuden parantumisen, mitä tuki vahva toteutus Suomen Power-segmentissä ja Norjan kannattavuuden säilyminen kolmannen peräkkäisen vuosineljänneksen ajan, mikä vahvistaa entisestään yksikön jatkuvaa käännettä. Johto toisti luottamuksensa 5 %:n oikaistun EBITA-marginaalitavoitteen saavuttamiseen aiemmin ilmoitetussa 12-18 kuukauden aikataulussa, ja vahva Q1-tulos vahvisti tätä vakaumusta. Vaikka tämä on rohkaisevaa, olemme edelleen varovaisempia ja uskomme, että Eltelin on todistettava, että 5 %:n tavoite on saavutettavissa johdon aikataulussa. Nostamme kuitenkin vuosien 2026-27e tulosennusteitamme raportin jälkeen, mikä heijastaa ensisijaisesti odotettua vahvempaa Q1-suoritusta. Nykyisellä arvostuksella näemme edelleen hyvän riskikorjatun tuottopotentiaalin ja toistamme Lisää-suosituksemme tavoitehinnalla 11,2 SEK (oli 10,2 SEK).

Mukavan kokoista sopparia sisään: 275 M€ / 8 vuotta. Kurssikin otti pienen pompun uutiseen tänään. Toivottavasti on taas osa sitä uusiutuvaa sopimuskantaa, jossa terveemmät marginaalit. Hyvältä näyttää Eltelin meno.

Tässä on Christoffer Jennelin kommentit Vattenfall-sopparista

Eltel tiedotti maanantaina Vattenfall Eldistributionilta saamastaan palvelu- ja kunnossapitosopimuksesta, jonka arvo on noin 138 MEUR neljän vuoden alkuperäisellä sopimuskaudella ja joka voi nousta 275 MEUR:oon sisältäen neljä optiovuotta. Sopimus edustaa uutta volyymia Eltelille, jonka aiempi työ Vattenfallin kanssa oli keskittynyt älymittareiden käyttöönottoon, ja uskomme sen merkitsevän merkittävää laajennusta tähän suhteeseen. Näkemyksemme mukaan sopimus parantaa Ruotsin yksikön keskipitkän aikavälin ennusteidemme näkyvyyttä ja aiheuttaa nousupainetta ennusteisiimme, vaikkakin odotamme lopullisen sopimuksen allekirjoittamista ennen niiden tarkistamista.

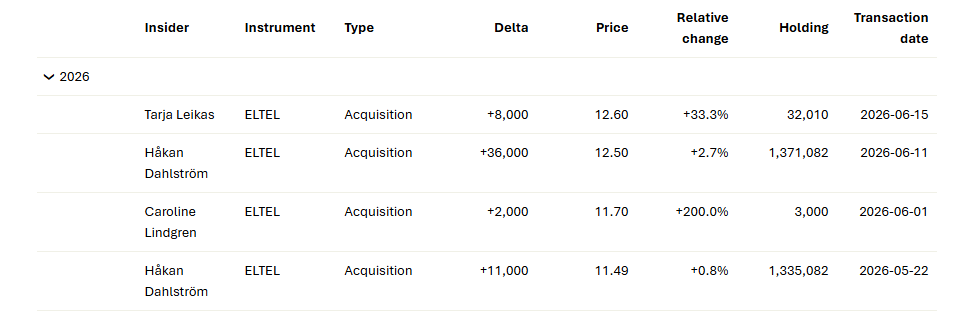

Kyllä se luo mukavasti luottamusta käänteeseen, kun toimitusjohtajan lisäksi muukin sisäpiiri ostaa. Toki muiden summat vielä aika vaatimattomia Dahlströmiin verrattuna, joka osti vuonna 2024 n. 300 000 osaketta, viime vuonna n. 530 000 osaketta ja tänä vuonna toistaiseksi 47 000 kpl.

Christoffer on tehnyt uuden yhtiöraportin Eltelistä

Nostamme Eltelin tavoitehinnan 13,8 kruunuun (aik. 11,2 kruunua). Nousu heijastaa päivitettyjä pitkän aikavälin arvostusoletuksia, joissa on alhaisempi pääomakustannus ja hieman korkeampi terminaalinen liiketulosmarginaali, eikä niinkään muutoksia lähiajan operatiivisiin ennusteisiimme, jotka jätämme pääosin ennalleen. Q1:n jälkeisen voimakkaan osakekurssinousun jälkeen katsomme kuitenkin arvostuksen karanneen liian pitkälle, eikä riskikorjattu tuotto ole enää houkutteleva nykyisillä tasoilla. Laskemme siksi suosituksemme vähennä-tasolle (aik. lisää). Pidämme vireillä olevaa Vattenfallin puitesopimusta Roslagenin ja Upplandin sähköverkosta selkeänä positiivisena asiana, joka virallisesti allekirjoitettuna lisäisi nousupainetta keskipitkän aikavälin ennusteisiimme. Koska sitä ei ole vielä allekirjoitettu, emme tee ennustemuutoksia tässä vaiheessa. Korostamme kuitenkin, että itse sopimus ja sen sisällyttäminen ennusteisiimme eivät muuttaisi arvostusnäkemyksiämme nykyisillä tasoilla.

Tässä on Lucaksen kommentit Eltelin Suomesta saamistaan soppareista

Eltel tiedotti perjantaina 34 MEUR:n voimajohtoprojektista Fingridille ja erillisessä tiedotteessa 20 MEUR:n sähköverkon liityntäsopimuksesta FCDC:n uudelle datakeskukselle. Näemme nämä yhteensä 54 MEUR:n arvoiset voitot positiivisina, sillä ne korostavat Eltelin vahvaa kilpailuasemaa Suomen Power-segmentissä ja vahvistavat tunnistamiamme rakenteellisia kasvuajureita verkon vahvistamisessa ja datakeskuksissa. Pidämme tilauksia positiivisina, sillä ne tukevat ennusteitamme, ja tarkastelemme ennusteiden päivitystarvetta yhtiön tulevan Q2-raportin yhteydessä 21. heinäkuuta, kun saamme paremman kokonaiskuvan yhtiön näkymistä ja kehityksestä.

Christoffer on tehnyt ennakkoyhtiöraportin Eltelistä, kun yhtiö julkaisee Q2-rapsansa ensi viikon tiistaina.

Nostamme Eltelin suosituksen lisää-tasolle (aik. vähennä) ja tavoitehintamme 14,0 kruunuun (aik. 13,8 kruunua) ennen yhtiön Q2-raporttia 21. heinäkuuta. Suosituksen nosto johtuu ensisijaisesti osakekurssin noin 15 %:n laskusta kesäkuun lopun päivityksemme jälkeen, mikä on mielestämme tuonut arvostuksen takaisin houkuttelevammalle tasolle. Tämän ohella nostamme hieman vuosien 2026-2028 ennusteitamme heijastamaan ensisijaisesti äskettäin tiedotettuja 54 MEUR:n arvoisia Suomen sopimusvoittoja, kun taas Q2-ennusteemme pysyvät ennallaan. Odotamme edelleen vankkaa, Power-segmentin vetämää liikevaihdon kasvua ja edelleen paranevaa vuotuista kannattavuutta. Raportissa keskitymme Norjan käänteen kestävyyteen, johdon laadullisiin markkinanäkymiin ja kommentteihin sen 5 %:n oikaistun EBITA-marginaalitavoitteen saavuttamisesta.