Laitetaan nyt tällekkin suht tuoreelle länsinaapurin listautujalle uutta ketjua pystyyn.

Yritys on perustettu vuonna 2011 ja toimii photocromic (valokrominen?) indikaattoreiden parissa. Listautuminen tapahtui kesän 2021 huumassa Tukholman First Northiin.

Kiitos @jaska7 että toit tämän esiin. Vaikuttaa omiin silmiin todella lupaavalta. Pitää tehdä vielä enemmän tarkempaa selvittelyä ajan kanssa. Piti kuitenkin fomottaa tätä ja ostin 500kpl:ta salkkuun 26,85SEK kun näyttää liikkuvan todella rivakasti. Arvostushan on viime vuoden tuloksella ihan naurettavan halpa yhtiöstä joka kasvaa näin kovaa. Eikä tarvitse paljoa kasvaa niin silti näyttää halvalta (kunhan ei liikaa osakkeita printattaisi). Mitäköhän kaikkia pommeja vielä tuleekaan eteen? Tuli mitä tuli niin omalla vastuulla mennään tietenkin. Yleensä teen tarkempaa tutkimusta ennen ostoa, mutta tein tällä kertaa poikkeuksen.

Muutamia huolenaiheita löysin raporttia tutkiessa.

Osakkeiden määrä on noussut vuodessa 6,6 miljoonaa eli +33,5% (Number of shares average 26 305 282 vs 19 702 660). Ihan järkyttävä määrä uusia osakkeita vuodessa. Onko Jaskalla tiedossa liittyykö nämä johonkin yritysostoon vai onko kannustinpalkkioita?

Lisäksi kun laskeskelin noita kannustuspalkkioita niin sieltäkin joku pari miljoonaa lisäosaketta olisi maksimissaan kai tulossa. Mikäli oikein ymmärsin niin näistä saajat maksavat kuitenkin itsekin eli ei olisi täysin ilmaisia kuitenkaan. Toivotaan jatkossa maltillisempaa politiikkaa.

Kassavirta oli pakkasella, mutta kun kasvetaan niin ei ollut kovin yllättävää. Myyntisaamiset on nousseet kovasti joka ei kuulosta myöskään oudolta kun kasvetaan, mutta toki tulee helposti vähän Tecnotree fiilikset jos saamiset nousee. Kuitenkin raportissa manitaan. Receivables continue to be paid according to plan and, as Intellego grows, we are shortening payment times for our customers. Intellego does not currently have any past due receivables. In 2024, the Intellego group expects receivables to stabilise at around 25-35% of annual revenue.

Ei siis mielestäni mikään red flag, mutta ehkä sellainen mitä tulee seurailla. Uskotaan että kaikki kunnossa saamisien suhteen kunnes toisin todistetaan.

Nopeasti vastaan, koska sen verran yhtiötä aikaisemmin pöyhin, että muistaakseni tehtyä yritysostoa maksetaan liiketoiminnan tuloilla ja uusilla osakkeilla. Muistaakseni luokkaa 50MSEK vaikutus kokonaisuudessan, että kauppa on hoidettu loppuun asti. Nämä ihan ulkomuistista, korjatkaa ja täsmentäkää.

Intellego todellakin pari vuotta vanha pörssiyhtiö ja kasvanut kovaa. Mukaan mahtunut myös epätarkkuuksia pörssitiedotteissa joista mm. Dangen industi kirjoitti viime vuonna. Näiden johtosta kurssi sukelsi viime vuoden kesällä. Linkistä löytyy nuo dagens industri uutiset.

Myyntisaamiset todella kasvaneet ja niitä pitää jatkossa tarkkailla.

“Intellego Technologies announces a significant financial milestone as its Q1 revenue exceeds 70 million SEK (43) with an expected EBIT above 32 million SEK. This achievement underscores the company’s robust sales strategy and the strong market acceptance of its product offerings.”

Kertoo mun mielestä törkeän halvasta arvostuksesta että yritysarvo on noin 785MSEK ja annetaan pientä vihjettä että 32MSEK Ebitiä olisi saatu jo kasaan Q1:llä. 785M/32M ->EV/EBIT 24,5 vaikka loppuvuosi tehtäisi nolla Ebitiä

Tässä olisi ihan mahdollinen ten bäggeri imo, mutta aika näyttää.

Esim. Kempower koko vuoden ennusteella EV/EBIT 33,2

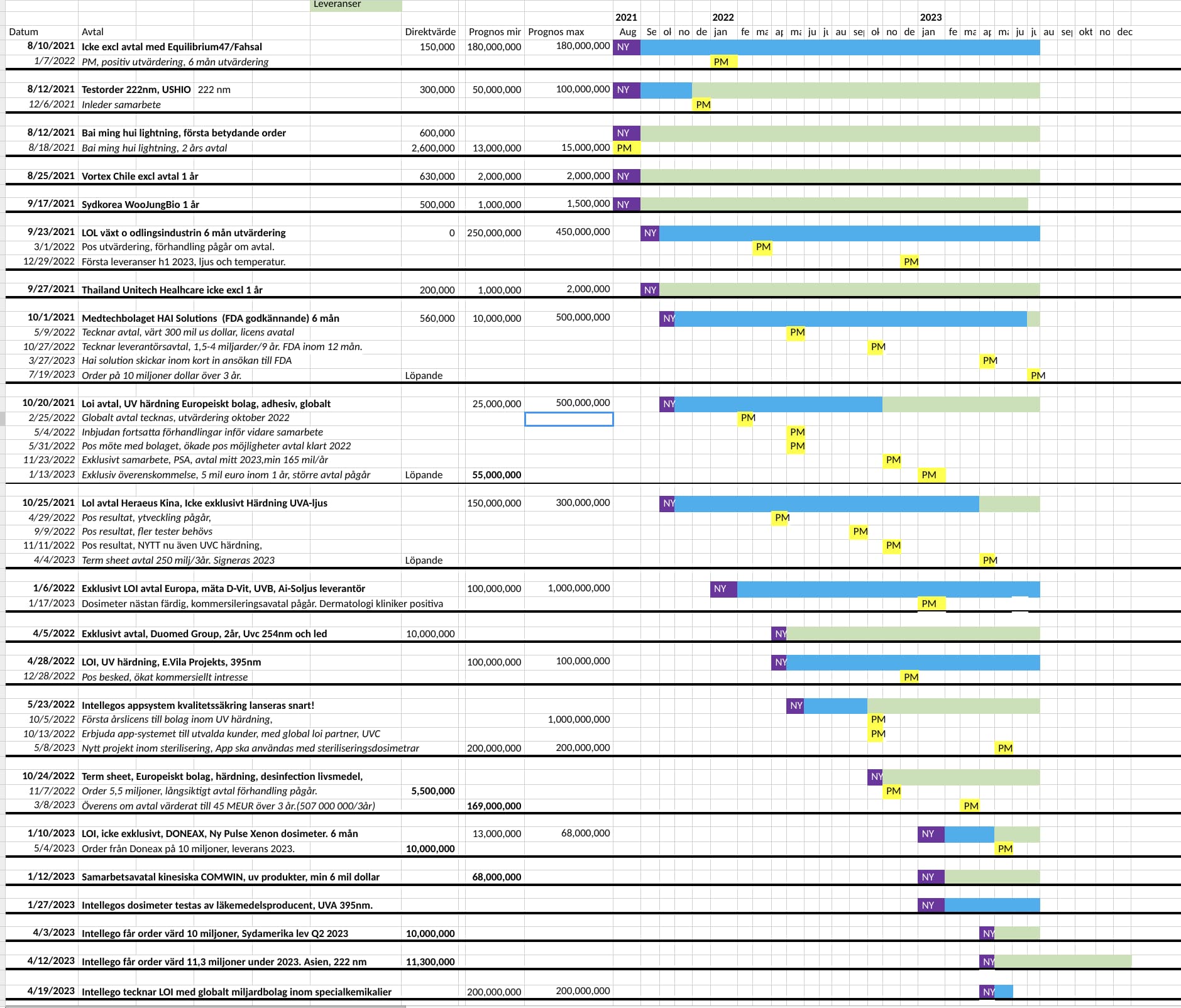

Yksi mielenkiintoinen intellegon yhteistyökumppani/asiaka on HAI solutions jenkkiläinen startup jolla oma neulaton patentoitu IV- portti. Tuohon on tarkoitus integroida intellegon indikaattorit jolloin voidaan seurata että bakteereita ei pääse verenkiertoon. HAI solutions lupaprosessi käynnissä FDA käynnissä. Markkinat näyttäisivät olevan isot.

Lehdistötiedotteessa toimitusten arvoksi 9 vuoden ajalla arvioitiin 1.5 - 4.0 miljardia SEK. FDA luvan piti tulla jo viime vuoden lopulla mutta on näköjään venynyt.

Pari muutakin uutista linkedin puolella. Briteissä myönnetty patentti ja julkaisivat 395 nm aallonpituudella toimivat annosmittarin. Tämä erityisesti muovi ja autoteollisuuteen kun tarvitaan valvoa UV kovettumista tarkasti.

Intellego ja asiakas saaneet aikaan positiivisen selvityksen UV -kovettumis -markkinoista. Discord huhutaan että asiakas olisi Saksalainen Henkel jolla myyntiä yli 160 maassa. Näyttää ihan hyvältä.

On January 26, 2024, Intellego announced that it and one of its curing partners — a leading global multinational —were conducting a global market evaluation for a category of Intellego’s curing dosimeters.

This evaluation has now been concluded, and the results are positive. This means that the global launch of Intellego’s new curing dosimeters and app is now being planned. Intellego and its as yet unnamed partner will engage further in contractual discussions to expand their existing agreement to include global, exclusive market rights for certain products and applications in the curing industry.

Exactly when these discussions might result in a newly signed agreement can not be said now.

Tuli hankittua eilen seurantapositio, joten tässä tämän päivän osari.

Summary of the period 1 January to 31 March 2024

Net sales was TSEK 79 609 (42 869)

Cash flow from operating activities was TSEK 34 093 (-16 325)

Profit after financial items was TSEK 38 948 (15 176)

Profit after tax was TSEK 35 667 (13 887)

Earnings per share, before dilution, were TSEK 1,35 (0,59)

“Approximately 70% of the group revenue in Q1 came from reoccurring customers”

Osakkeen hinta 30sek tasolla, joten jos tulos pysyy muina kvartaaleina vähintään samalla tasolla niin tämän vuoden P/E on jossain alle 6.

Joku pieni yritysosto tehty, mutta vaikuttaa suorastaan naurettavan halvalla ostetulta

“in Q1, Daro made a small acquisition of UV Light Technology Limited which will accelerate the business across the UV spectrum including UVC disinfection and sales of relevant equipment together with dosimeters. UV Light Technology contributed 45,000 GBP in revenue during Q1 (March only). Its agreed purchase price was 437 500 GBP. The actual payment made was 496 902,81 GBP once all adjustments were agreed and accounting to the cash in the business and UV Light Technology had annual revenue of approximately 510 000 GBP in 2023 and made a profit of 82 500 GBP. The intention with this acquisition is to accelerate growth in the group. Daro sees significant opportunities to increase both revenue and profit in UV Light Technology.”

Näkymät ennallaan

“Growth is expected to continue in 2024 and Intellego and Daro see several attractive expansion possibilities which we are keen to capitalise on, both organically and through acquisitions, using existing sources of funds. The year continues to develop well for the group and market interest continues to grow, which is evident from the increasing, larger commercial discussions the group

has with customers. The Intellego group continues to grow into a global company, and we are investing heavily in that growth. This will be our focus for the foreseeable future. As a sign of this, we have previously communicated 2024 financial goals for the group of over 300 million SEK in revenue and over 110 million SEK in EBIT, which we hereby reaffirm.”

Ja uusi CFO saatu, joten sekin epävarmuus poistunut.

Hyvä osari. Myyntisaamiset kasvoi 115 miljoonaa SEK mutta Q1 aikana kotiutettiin 55 miljoonaa SEK eli ihan hyvä saavutus. Liikevaihdosta 70 % todellakin vanhoilta asiakkailta mikä erittäin hyvä.

Mielenkiintoinen lause toimitusjohtajan kertomuksessa että intellego harkitsee listausta Nasdaq tai joku muu markkina (up-listing). Tällä hetkellä Intellego First North Sweden. Tämä voisi lisätä osakkeen vaihtoa ja kiinnostusta rahastoissa. Myös CFO palkattiin.

Myös sopimus UV-kovettumispuolella etenee intellego on kutsuttu aloittamaan sopimuksen teko kansainväliseksi toimttajaksi. Discord mukaan tämä asiakas on mahdollisesti Henkel jonka maailman laajuinen liikevaihto 22 miljardia euroa eli erittäin iso yritys. Tämä erittäin positiivista.

Tulee mielenkiintonen vuosi. Milelenkiintonen yksityiskohta Discord mukaan Avanza palvelussa intellogon osakkeita omistavien määrä kasvanut viimevuoden noin 1 600 tämän vuoden 3 600. Eli kiinnostusta myös ruotsissa.

Huono uutinen. Myös intellegon tilit tarkastava tilintarkastaja saanut huomautuksen tilintarkastaja virastolta. ilmeisesti jo toinen kerta. Ei siis liity mitenkään intellegoon tai intellegon tileihin tarkastaa vain myös intellegon tilit. En yhtään ihmettelisi jos tilintarkastaja jossain vaiheessa vaihtuisi.

Placera forumilla spekuloidaan “pienellä” osakeannilla yhtiökokouksen jälkeen turvaamaan kasvuinvestoinnit.

Intellegolle tulee maksuun Daro kaupan jälkimmäinen kauppahinta 1.25 miljoonaa GBP elokuun lopulla. Tämä on ilmoitettu maksettavan intellegon kassavirrasta. Alunperin tämä oli tarkoitus maksaa tammikuussa mutta lykättiin yhteissopimuksella. Daron myyjät ovat intellegon merkittäviä osakkeen omistajia.