DraftKings’ roots are in Daily Fantasy Sports (DFS) games. In 2018, a Supreme Court decision liberalized the gambling market in the US. Since then, states have individually legalized either sports betting, casinos, or both. There are two major players in the industry, DraftKings and FanDuel. FanDuel claims to be larger by revenue, but DraftKings may be larger by other metrics.

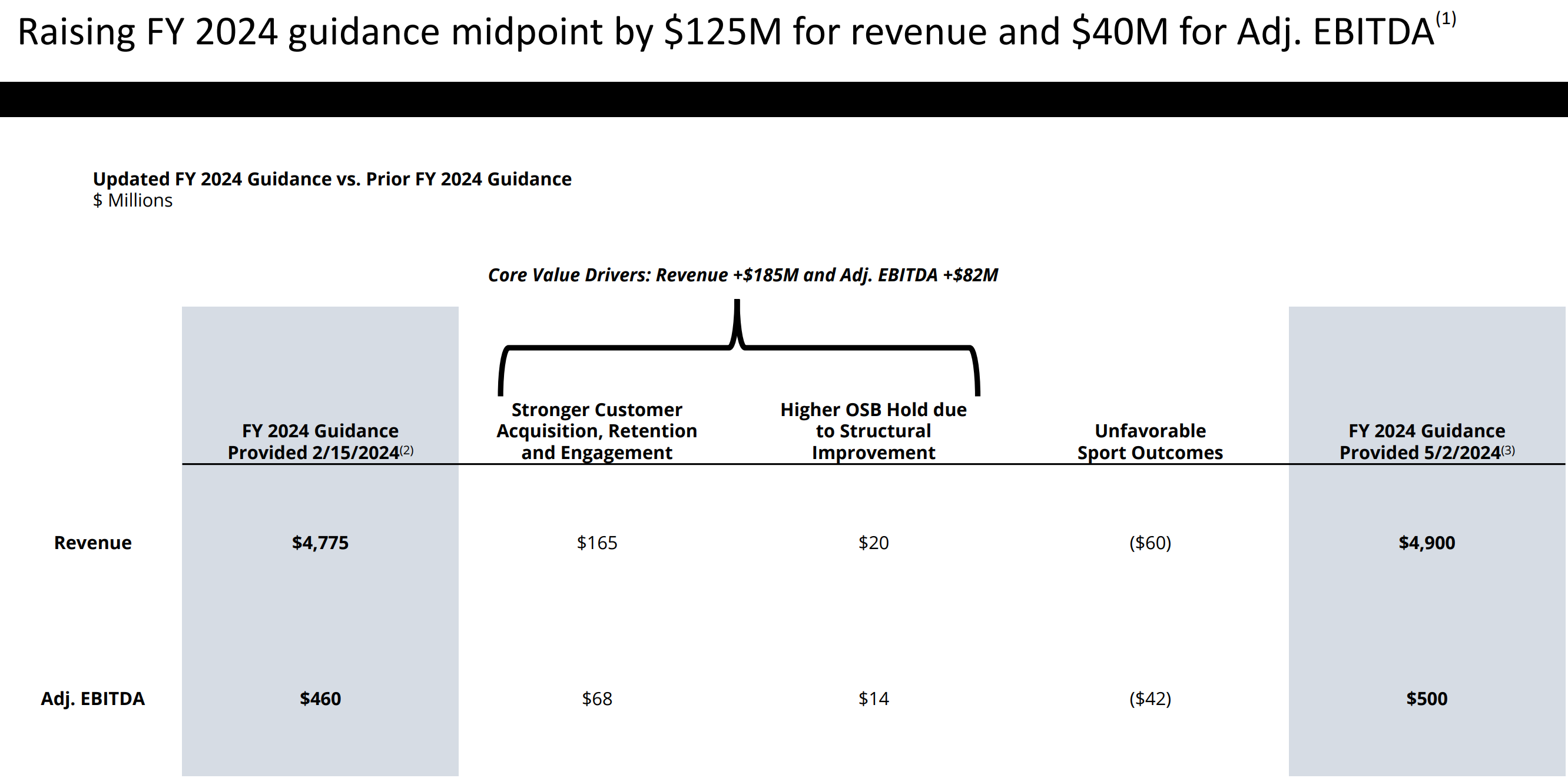

So far, the US gambling market has not yet generated a profit, due to high marketing costs. When a new state opens up, a large amount is invested in marketing and player acquisition, and profits materialize years later. That’s why DraftKings has not yet made a profit once during its stock market history. The year 2024 is expected to be the first profitable year. The company forecasts approximately $400-500m EBITDA for 2024.

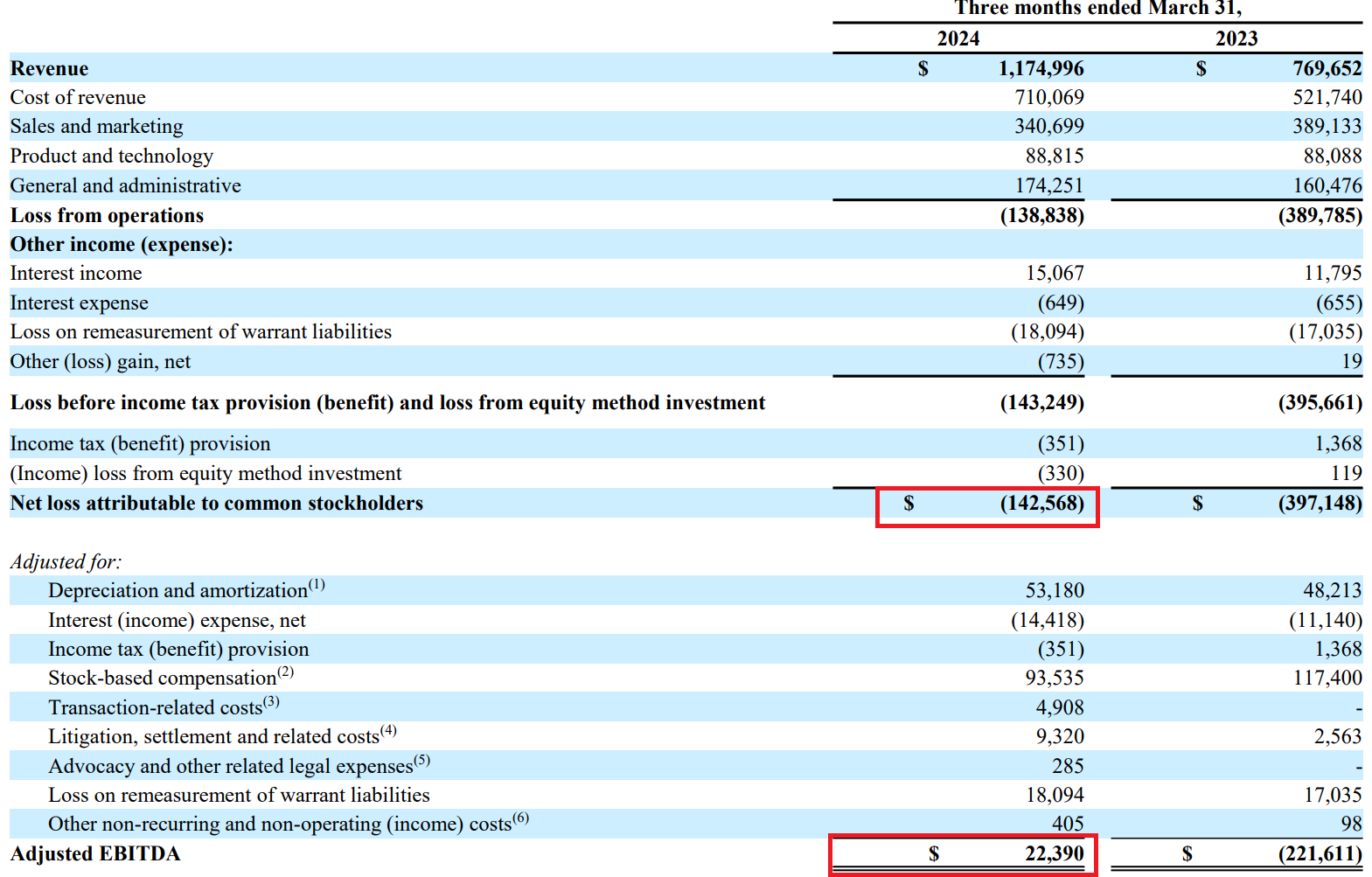

The difference between the net result and Adj. EBITDA is still 160m, so it looks like another big loss year is still ahead. In terms of cash flow, things look quite good, as most of the loss comes from stock-based compensation as usual.

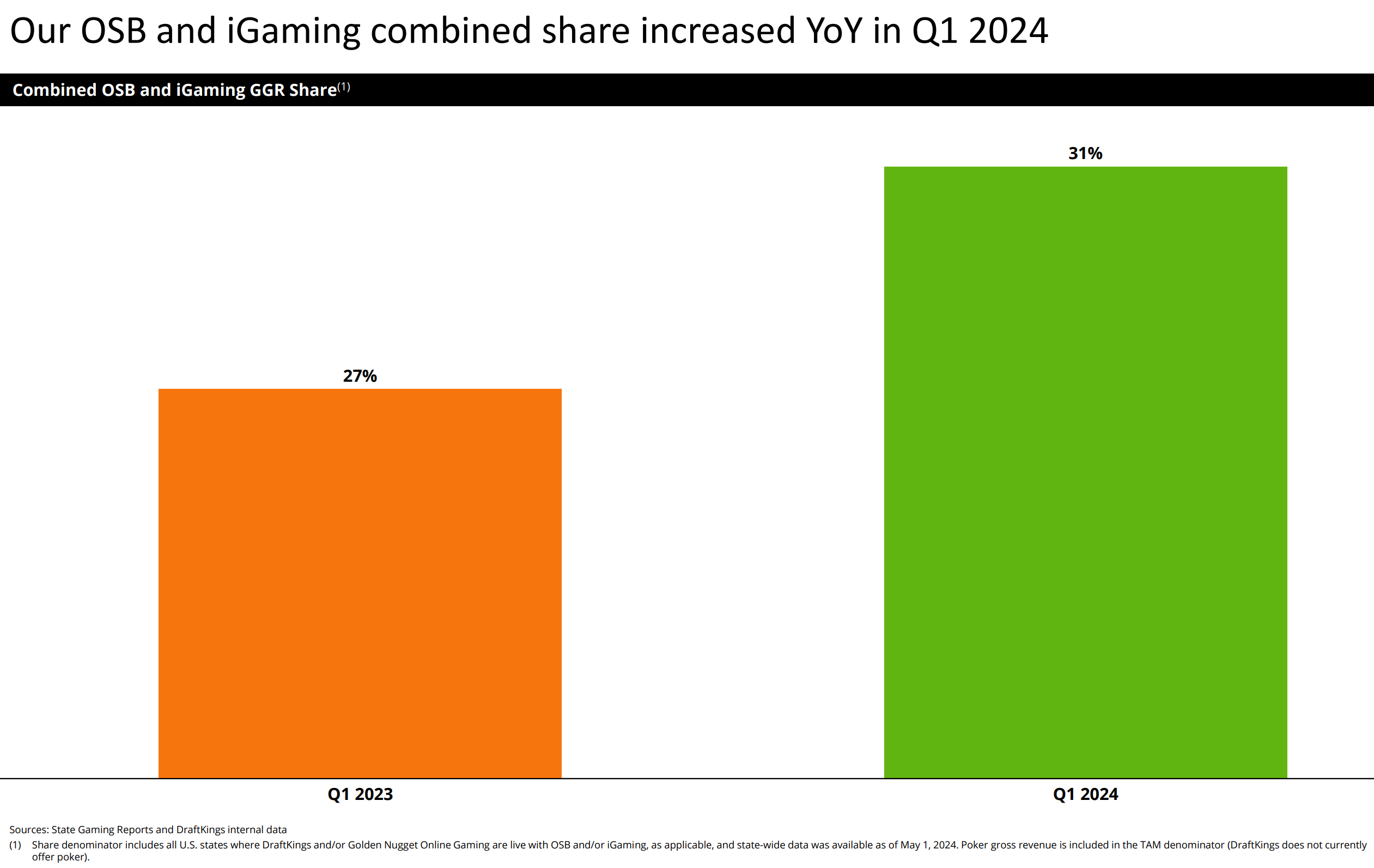

DraftKings lists a 31% market share, which seems small to me. This increases my expectations for competitor Flutter’s quarterly report.

January was a record-breaking month, February was poor, and March was okay in the betting market. Competitor Flutter’s report will indeed provide a better outlook. The risk is that DK might have to lower its targets. DK also operates in two states where Flutter does not (New Hampshire and Maine). In my view, that also makes that market share look weaker.

Let’s post some copy-paste here as well from the Flutter thread and the betting market:

Today it was in the news that there will be no online betting in Florida; it remains a tribal monopoly. The tribe has released its own platform for it.

There is speculation on forums that this would be a good decision for California. Californian tribes practically lack the resources to implement their own software, so by teaming up with major players, they would get at least some of the revenue. So, better to get some cash flow than nothing at all.

This was likely the reason for yesterday’s rally:

“ The preliminary NJ budget proposal came out and a sports betting / gambling tax hike was not included. This is an obvious relief following the progressive hike from IL last month”

DKNG has never made a profit and money just goes straight into management’s pockets. I find it funny that they talk about adjusted EBITDA; these Americans certainly know their accounting tricks. If the market cap is currently 20 billion, what should the profit margin be on over 5 billion in revenue for the investment to be attractive? For 2025, analysts expect 12%, meaning it would rise to exactly the same level as Kindred’s profit margin right now!? At least the tax rate will probably be close to 0% for the next 5 years, since the company has realized losses that can surely be deducted from those “profits”

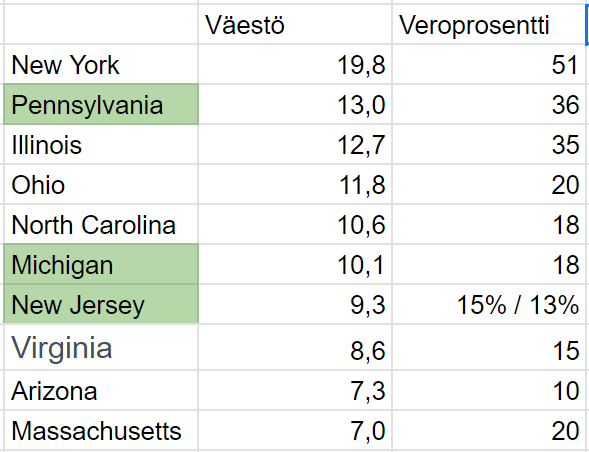

In America, competition between operators is cutthroat; what kind of loyalty do customers really have when they jump back and forth chasing different offers? If DKNG reduces marketing costs, will growth drop immediately and customers flee to competitors? For example, Kindred ended its American venture when they realized it’s impossible to compete with these other players who just burn shareholder money like that. For example, Betsson hasn’t entered this market, but is waiting patiently for the market to calm down before entering with a B2B sportsbook. And how will the high American gambling tax affect things? For example, New York already has a 51% tax rate for gambling operators.

Personally, I’ve stayed away from this company; it’s impossible to know when the company will actually become profitable. I remember well in 2020 and 2021 when people were saying that legalization would start soon and they’d turn a profit. What has happened 3-4 years later? The stock price crashed over 70% and has then risen over 100%, but operations are still loss-making. At what point do fundamentals matter?

DKNG has never made a profit and the money just goes directly into management’s pockets.

This is absolutely true. Half of DraftKings’ result (loss) has gone to stock-based compensation.

I think it’s funny that people talk about adjusted EBITDA; those Americans really know their accounting tricks.

“EBITDA = bullshit earnings” - Charlie Munger

There is a reason for this. Adjusted EBITDA allows for the separation of non-cash items. Stock-based compensation and the amortization of intangible assets from acquisitions do not affect cash flow. But yeah, it’s also a convenient way to hide excessive stock-based compensation.

what the profit margin should be

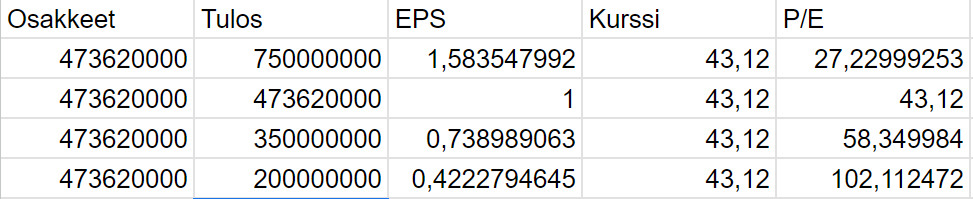

I had analyzed this as well. If the company made as much profit as there are shares, then EPS = 1 and P/E would be 43. With an operating profit of 750 million, it would reach a moderate P/E of 27.

The company made a loss of 800 million last year. Apparently, the US business will start generating profit this year.

Here are the initial comments

I don’t believe this. I personally believe that smaller operators will be forced to exit the market as unprofitable, and that DraftKings + FanDuel will continue as a duopoly. I consider Bet365 a promising example of a company with bottomless cash reserves and the ability to endure years of losses. It could succeed in the States.

If tax increases occur, there will also be fewer campaigns and less marketing. Tax increases are also a moat for new entrants.

Just as important is the “customer retention rate”. I’ve seen some statistics on this from a competitor.

Short answer: it will be passed on to customers in the form of worse odds.

Tax increases are certainly coming, and the company just needs to prepare for them. Tax increases eat into earnings to some extent, so investors are quite right to be nervous about them. Industry players say that a low tax percentage is best for both the market and consumers. We’ll see if they manage to lobby for that idea.

Below are the largest markets and their tax percentages.

Fundamentals don’t matter. DraftKings is a story stock. Speed blindness sets in when the future is being painted, and in the world of Adjusted EBITDA, comparable earnings are not available.

I don’t own DraftKings myself. Competitor Flutter is my largest holding.

Regarding fundamentals, I’d also say that this year should be cash-flow positive. From there, stock-based compensation and acquisition items are deducted to get the real result.

On what grounds would the market be a duopoly in the future? Currently, this might be the case as these firms are spending large sums of money, but what real competitive advantages do these two operators have compared to others? It is unlikely that DKNG or FanDuel could offer better odds than, for example, Betsson or Kambi; I believe the latter even have better odds. Almost all operators also use EVO’s services, so how does the offering really differentiate itself? I repeat, customers have no particular loyalty towards these operators. The only possible differentiator could be the brand, but I don’t believe it carries as much weight in the gambling industry. Would it be some kind of status symbol that someone bets on the DKNG site? People don’t flex about these things.

DKNG and FanDuel are not comparable to companies like Amazon, Uber, Airbnb, or DoorDash, where network effects are prominent and one must run loss-making operations to crowd out competitors, only raising prices once they are the sole operator. I believe the market will evolve like the European one, with many different operators and fierce competition. Why couldn’t other European operators obtain a license through an acquisition and come in to compete? This is a very common strategy for many, such as Betsson.

High gambling taxes encourage customers to play with unlicensed foreign operators. It is unlikely that DKNG will ever be able to turn a significant profit in New York with these taxes. Generally, industry players always paint such a rosy picture because it’s in their interest to say that taxes are falling and legalization is progressing. Just look at what happened in the case of California.

I would argue that the customer retention rate metric cannot be fully relied upon until DKNG is a profitable outfit and other competitors have entered the market.

The US market differs from Europe and especially Finland in that there is a smaller number of licenses available. I read an article about Illinois, which has 8 operators now. This is because in many states, Native American tribes have exclusive rights to gambling activities. Betting companies then make agreements with the tribes. Or with land-based casinos in states where this does not exist.

Competitor Flutter (FanDuel) has 30 years of experience in the industry. They know the betting market well and can offer better odds. Data analytics is important, and for that, you need large masses of data. It certainly shows in operational activities when you’ve been running numerous different sites for decades. DraftKings is in its infancy in this regard.

Betting markets are the main focus in the US because casino gaming is open in only 5 states.

Word-of-mouth, brand. The fact that the brand becomes synonymous with betting—i.e., if you want to place a bet, FanDuel/DraftKings is what forms in people’s minds.

There are no signs of this so far. I don’t, however, follow the smaller operators with a very close eye.

Money. You need deep pockets to withstand hundreds of millions in losses before states start to become profitable. And repeat this same process for every new state you open in. You should reach profitability in 2-3 years.

I would also argue that it was easier to start in a state when it first opened than to open as a new player later. Those marketing costs will be massive.

Bovada is the main player in the gray market, and it has already been banned in many states, Michigan being the latest.

And the main incentive would be better odds. I don’t believe gray market operators would be operationally better in that regard.

I wouldn’t be quite that bullish on DK yet. There are many states where DK is the most popular operator. If smaller operators start eating market share, then I would be worried. I haven’t really seen significant signs of this.

And finally: In my opinion, DraftKings is a hype stock that has been well-marketed to investors (the Jim Cramers, etc.).

There are no signs that it is an operationally superior company in any way. Almost the opposite, due to large stock-based compensation. Flutter is indeed my main investment, the owner of FanDuel. It is the operationally best company in this field.

Edit: I’ll also add that nothing really prevents old incumbent operators from handing out good promos to old customers, so-called “generosity offers”

I disagree with you on this. You apparently believe that ROIC will be incredibly good in the American market in 3-5 years. We’ll see, but has anyone actually calculated how much money has already been lost in America over the last five years?

You also apparently believe that this is a “winner takes all” market and that in 3 years, the big profits will start rolling in. Meaning that in 3 years, other players won’t be able to enter, for example through an acquisition, and win market share from these two giants.

It’s also worth remembering that sportsbook margins usually range between 6–11% (for example, at Betsson and Kindred). In the end, this isn’t a high-margin business; the big money is made with casino products.

I still stand by my thesis that first movers have the largest customer bases and thus a competitive advantage. Acquiring new customers is expensive. Acquisitions would only increase the need to raise margins, meaning worse odds for customers.

I can write a longer response, e.g., about how much the US revenue has grown (from zero). In H1/2024, we will know more precisely where we stand regarding the bottom line.

I’ll also add that US operators like BetMGM, Caesars, etc., are primarily land-based casino operators who are now dipping their toes in the water regarding online business.

Regarding the size:

Betsson’s 2023 sportsbook revenue was 267m. Casino 672m. You are right that casino generates better income.

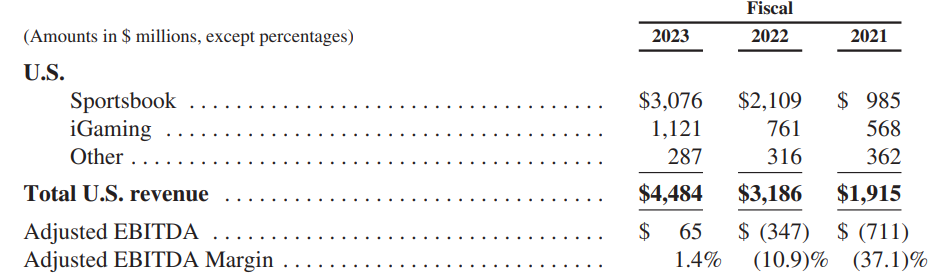

Let’s then compare these to FanDuel. FanDuel’s US revenue for sports betting alone was €2.9bn. Casino generated €1.05bn in revenue.

DraftKings reported €3.43bn in revenue. DK does not break down casino and sportsbook results.

So the US is a massive market. Even if betting has a lower margin, economies of scale are achieved from large numbers of players. Marketing theoretically costs the same whether you are the industry’s largest or smallest operator. This benefits large players with a large cash position.

These are FanDuel’s statistics. They provide an indication of how fast the industry is growing. This year, the North Carolina market opened, which is close to the top 5 states by revenue.

Adjusted EBITDA is practically cash flow in this case. Money flows into the cash reserves, but from that, the amortization of intangible assets from acquisitions, as well as share-based compensation, etc., are deducted.

The cash reserves are no longer depleting for these two big players. DraftKings, by the way, still has a large cash pile from its listing.

FanDuel’s statistics also show that the US sportsbook margin is 7.5%, while in the rest of the world, it is 12% or more. This indicates a high tax rate. But Americans bet a massive amount, which is why the market is profitable.

Below is a comparison of the British Isles and the US. The number of players is almost the same. Americans bet 3.3x more, but only 2x more makes it to the bottom line.

“To put this into perspective, the top seven companies control approximately 98% of sports betting revenue and 90% of iGaming revenue, with the remaining 36 active operators competing for a small pool of players,” the analysts noted.

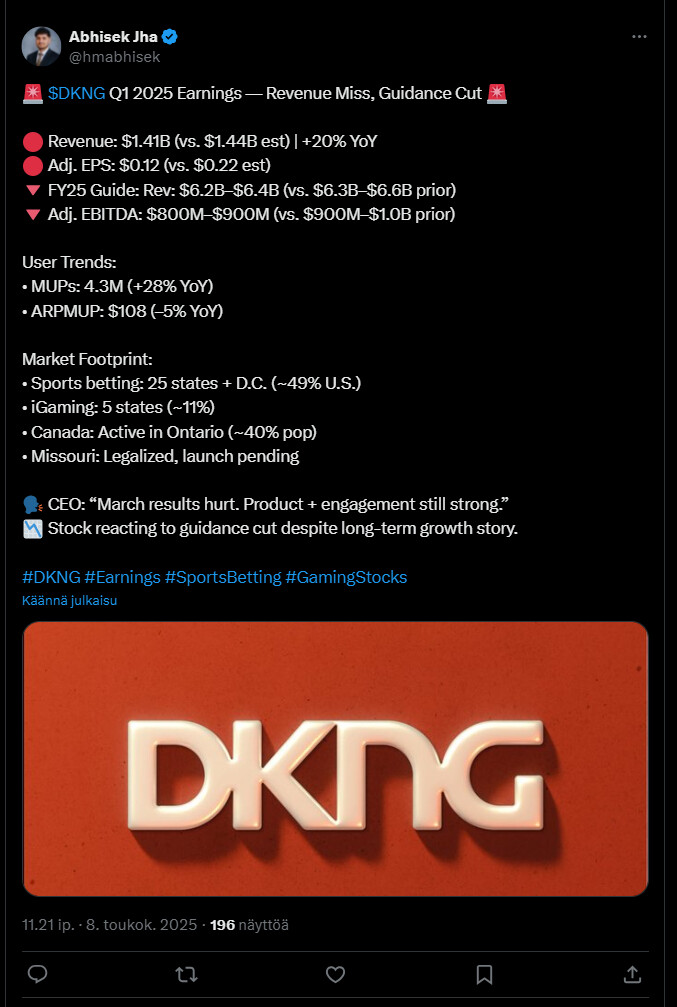

DraftKings lowered its guidance in Q3/24. The company got greedy after a strong Q1 and has now been forced to backpedal. The adjusted EBITDA guidance had already been lowered in Q2.

In post-market trading, the stock briefly dipped -16% but quickly recovered to around the -5% range. The market has the memory of a goldfish, and the stock is now more expensive than it was before the earnings report.

Americans are fine with a company that burns its earnings on stock-based compensation.

DraftKings is revising its fiscal year 2024 revenue guidance due to the impact of customer-friendly sport outcomes early in the fourth quarter of 2024 to a range of $4.85 billion to $4.95 billion from the range of $5.05 billion to $5.25 billion, which the Company previously announced on August 1, 2024. The Company’s updated 2024 revenue guidance range equates to year-over-year growth of 32% to 35%.

DraftKings is revising its fiscal year 2024 Adjusted EBITDA guidance due to the impact of customer-friendly sport outcomes early in the fourth quarter of 2024, partially offset by promotional optimization and expense efficiency. The Company now expects fiscal year 2024 Adjusted EBITDA of between $240 million and $280 million compared to its prior fiscal year 2024 Adjusted EBITDA guidance of between $340 million and $420 million, which the Company previously announced on August 1, 2024.

DraftKings significantly increased its revenue in the last quarter of 2024, even though the average revenue per user decreased.

The company successfully acquired and retained customers and improved profitability by optimizing marketing investments. Last year, the company achieved a positive adjusted EBITDA for the first time and also launched a share repurchase program.

For this year, the company raised its revenue forecast and confirmed its earnings guidance, continuing to focus on sustainable growth and improving profitability itself.

DraftKings significantly increased the number of paying monthly users in the first quarter of the year, which was apparently due to both strong customer loyalty and new customer acquisition.

Growth was also boosted by the acquisition of Jackpocket, although its customers generated less revenue on average than the company’s previous users.

According to the company, some product improvements have improved efficiency + metrics, so the financial situation remains stable.

Without unfavorable sports results (?) in March, DraftKings would have raised its full-year earnings forecasts.

The company repurchased its shares as part of a previous buyback program.

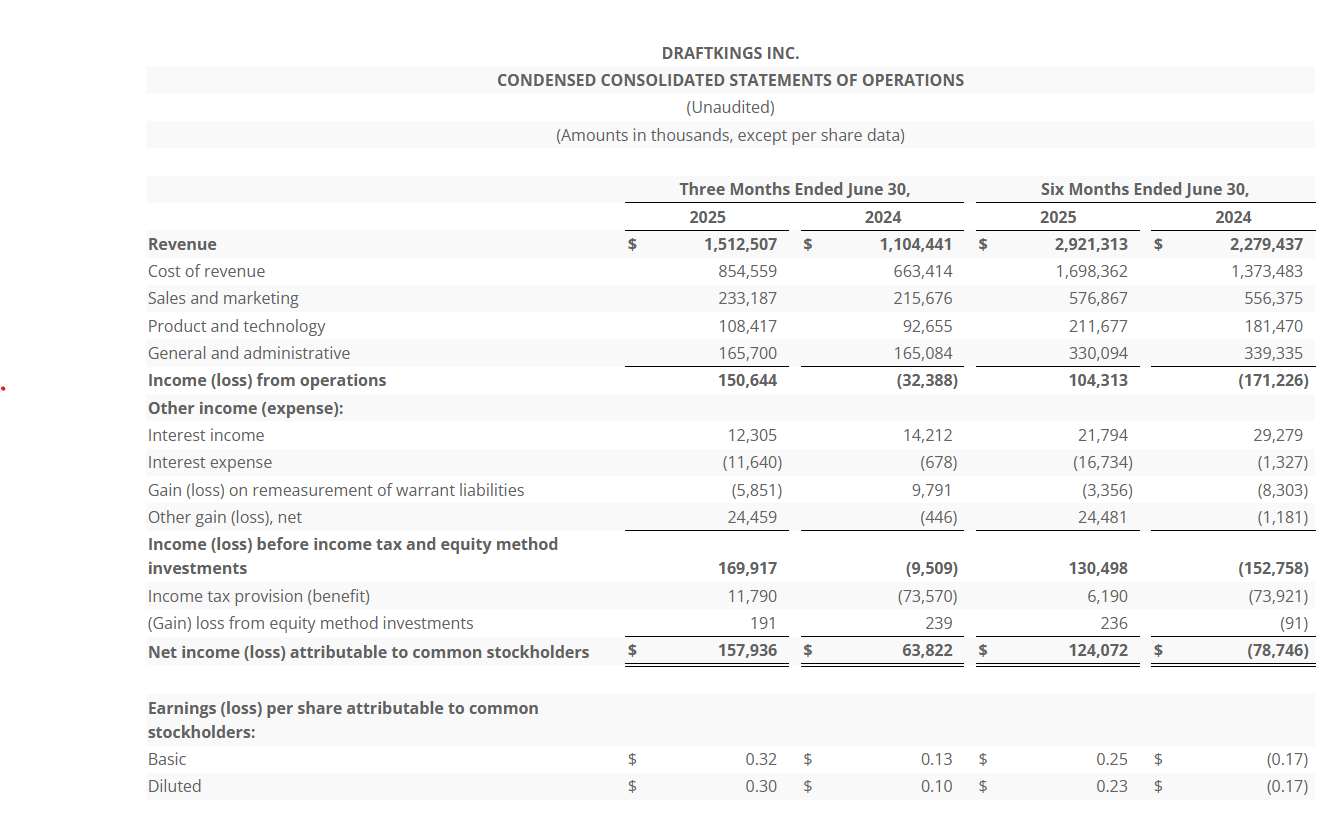

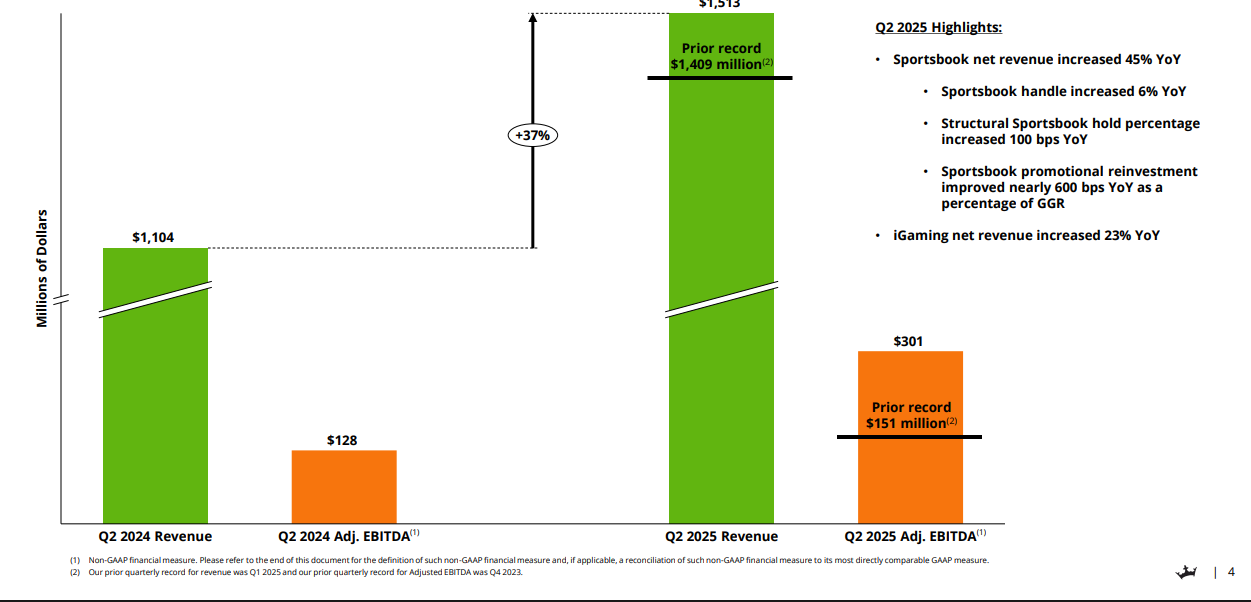

DraftKings is expected to have set some records in revenue, earnings, and EBITDA in the second quarter. Growth was particularly driven by sports betting and iGaming. In addition to these positive developments, the number of paying monthly users increased, as did the revenue per user.

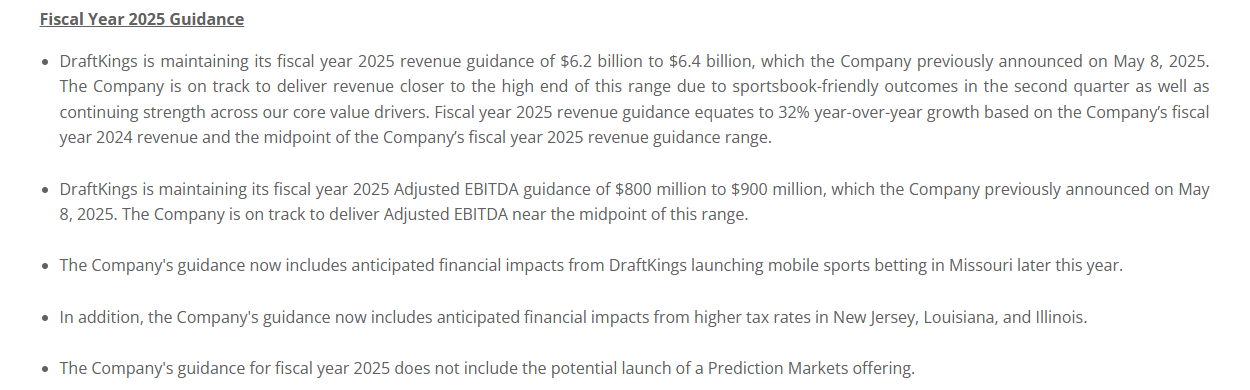

The company maintains its full-year guidance and expects a strong end to the year.

The article below describes how DraftKings CEO Jason Robins criticized a new tax rule included in “Trump’s megabill,” according to which bettors can no longer deduct all their losses from winnings. According to the CEO, the rule is illogical and unfair.