A queue at First North’s door, Digital Workforce announced its interest today.

Growth, recurring billing, software, robotics, intelligent automation…

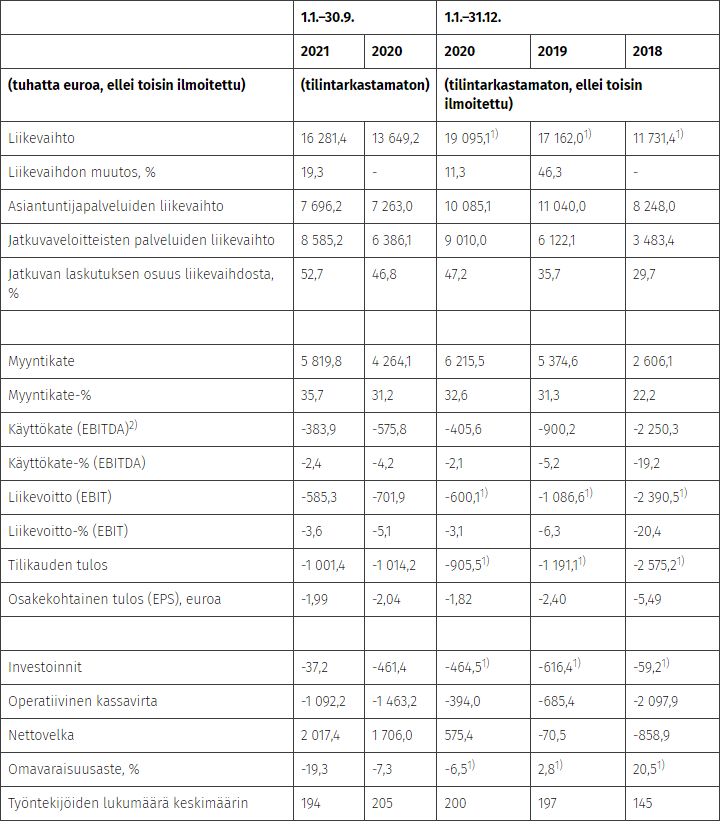

However, losses are already being made at the EBITDA level.

The company is seeking 20 MEUR in gross proceeds, and old owners are selling their shares. Subscription commitments for just under 10 MEUR, if the valuation of the share capital BEFORE the offering proceeds is at most 50 MEUR.

With my math, the company’s future market value can’t yet be calculated with the above information, so anchor investors probably have more info on, e.g., the size of the offering.

LEADING INTELLIGENT AUTOMATION SERVICE COMPANY

Digital Workforce is one of the world’s leading software robotics and intelligent automation service companies measured by both revenue and number of employees. Our company offers services to a wide customer base across different industries. We focus solely on intelligent automation. Our continuous goal is to earn our leading position by being the best player in the industry.

Financial targets and dividend policy

Digital Workforce’s target is 100 million euros in annual revenue by the end of 2026. Approximately 30 million euros of the annual revenue growth is expected to come from the Nordics and 50 million euros from the USA and UK.

In addition, the Company’s goal is a clearly positive adjusted EBITDA margin%[2] by the end of 2026. In the longer term, the Company targets an adjusted EBITDA margin% of over 20 percent, but during the period 2021–2026, the Company prioritizes investing in growth over profitability.

Digital Workforce does not have a confirmed dividend policy.

The planned IPO is expected to consist of an approximately 20 million euro share issue by the company (gross proceeds) and a share sale in which certain Digital Workforce shareholders sell their shares. The proceeds from the share issue are intended to be used to support Digital Workforce’s international growth strategy by strengthening international sales and delivery resources, as well as to fund potential acquisitions. Additionally, the proceeds from the share issue are intended to be used for investments related to the adoption of new technologies and to ensure production resources and scaling.

Anchor investors, namely certain funds managed by entities owned by Aktia Bank Plc, Handelsbanken Fonder, and certain funds managed by SP-Fund Management Company Ltd, have, under certain customary terms and conditions, committed to subscribing for shares in the IPO, provided that the company’s equity valuation before the proceeds from the IPO is at most 50 million euros. The anchor investors’ commitments total 9.4 million euros.

https://digitalworkforce.com/fi/etusivu/

https://digitalworkforce.com/fi/listautuminen/

https://www.sttinfo.fi/embedded/announcement?publisherId=69819009&announcementId=861&widget=true