Perhaps there’s plenty of work to be done there for DWF:

The organization is internationally respected, and its scale is exceptional from a European perspective, as its operational revenue is close to the same magnitude as the total public healthcare expenditure of Finland,” describes Jussi Vasama, CEO of Digital Workforce

Who knows how much of that is suitable work for Digital Workforce, but it’s a quite nice reference (especially from the USA) and it will likely contribute something to the bottom line, too.

Here is Joni’s preview ahead of Digital Workforce’s results release on Wednesday, February 18.

We forecast strong revenue growth driven by acquisitions and also solid organic growth. Additionally, we expect profitability to be strong, fueled by efficiency measures and growth in higher-margin recurring revenue. In the report, our attention will be focused particularly on the 2026 guidance and comments on the organic growth outlook in light of the recent major US contract. Our comprehensive report on the company, published in December and still very relevant, can be read here.

Financial statement report released, we got close to Joni’s forecasts. Outlook shows at least 15% growth for 2026, and the dividend proposal is a hefty €0.09. This looks good to me.

It also occurs to me that the categorically low valuations of IT service companies will likely lead to DWF being bought out of the stock market in the near future. Capman’s fund ownership is also already overdue; the fund has a slice of just over 15% of the company.

Right now certainly wouldn’t be the best time for realization, in the middle of the AI frenzy. Would they transfer the ownership to their newer Growth fund? I wonder how profitable an investment DWF is for Capman?

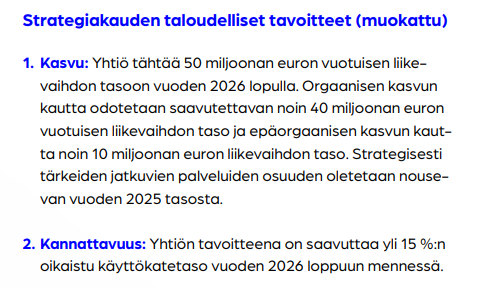

The ambitious financial targets for the strategy period were slightly modified regarding revenue, where the goal is now for revenue to be at the 50 million level by the end of 2026. Previously, the target was a revenue of 50 million in 2026.

The targets remain tough compared to, for instance, Joni’s forecasts (revenue under €40 million still in 2027). It will be interesting to see how and how close they eventually get.

Digital Workforce announced its 2025 financial statements this morning. Revenue grew strongly, driven by an acquisition, and was in line with our expectations. Profitability improved significantly but fell short of expectations. The company has won promising new and strategically key contracts in the early part of the year, which improves confidence, but there is still work to be done. The company’s guidance is well in line with our forecasts and even a slight positive surprise in terms of profitability. The dividend proposal exceeded our forecasts, and as a decision for a growth company, the high dividend proposal is a bit puzzling.

By the way, they could have used the dividend amount to buy out the shares of the weak hands. A share buyback via a tender offer would have been a better option.

Proposed dividend amount - tender offer supply at e.g. €2.5 / share = dividend for 2025. There would still have been something left for the dividend payment after the share acquisitions, I believe.

Joni interviewed Digital Workforce CEO Jussi Vasama regarding Q4

Topics:

00:00 Introduction

00:21 Q4 summary

01:45 Revenue growth drivers

03:34 Improved profitability level

04:23 Increase in capitalizations

06:50 Contracts won at the beginning of the year

09:54 Market outlook

13:51 Background assumptions for guidance

15:24 Reaching financial targets

16:43 Dividend payment

A fresh report from Joni regarding the financial results:

We reiterate our Add rating for the share and a target price of EUR 3.2. Digital Workforce’s Q4 figures were overall slightly softer than our expectations. The strategy resonates, and strategically important wins have been seen in the early part of the year. Now, clearer confirmation regarding growth is still expected, as well as its scaling into profitability. In our view, the valuation (2026e EV/EBIT 13x with an EBITDA-% of 8%, sum of parts €3.4) is attractive.

I’ve been following DWF with half an eye for a while, as this activity raises so many questions about what the goal is.

A while ago, ambitious targets were set for the coming years, which have now already been slightly moderated in their wording.

Dividends are paid out relatively generously, and one reason for that is to attract new owners.

Capitalizations have increased, which makes the guided EBITDA look perhaps better than it actually is.

Management, however, isn’t buying the stock even though there should be a growth path and the valuation is cheap relative to the targets.

Somehow, it creates the impression that they are trying to support the share price through various means. The operations are somewhat vague, and the outcome isn’t as desired either. DWF seems like a lucrative investment, but there is no real concrete evidence that the direction is correct. Even the partnership announced this morning is just a partnership without any minimum commitment level.

I wonder if it is possible to deduce from these recent deals whether these agent-based implementations were built on UiPath’s platform or something else?

Digital Workforce’s number of NHS trust customers seems to be growing at a brisk pace. In the 2025 financial results release on February 18, 2026, more than 60 NHS customers were mentioned; on February 27, 2026, a LinkedIn post spoke of 65+ customers, and now on March 4, 2026, the website of e18 Innovation, part of Digital Workforce, already mentions 70+ NHS customers. There are just over 200 NHS trusts in total, so there will likely be more to come.

I got a really positive vibe from Jussi’s Q4 interview and the releases from the beginning of the year. If we get even close to, for example, Inderes’ forecasts, then this is a ridiculously cheap stock:

P/E 26-28: 11.5 → 7.1

P/S 0.7 and dividend yield around 4%

Profitable international growth (they are promising over 15% growth for this year themselves) and the stock is hitting new ATLs daily. It’s unlikely that you’ll find similar figures—admittedly forecasts—very easily on any stock exchange.

It’s definitely appropriate to wake up the markets. Remember to be online on Thursday.

In practice, the profitability target for the strategy period was lowered by keeping it unchanged, because the relative EBITDA margin improves due to the change in accounting policy.

In addition, the company’s financial targets for the strategy period are specified in accordance with the new accounting practice as follows:

Growth (amended): The company aims for an annual revenue level of EUR 40 million at the end of 2026, including potential acquisitions. The share of strategically important recurring services is expected to increase from the 2025 level.

Profitability (unchanged): The company aims to achieve an adjusted EBITDA margin of over 15% by the end of 2026.

For the first time, Digital Workforce looks like a truly interesting investment opportunity to me. Valuation levels are at historical lows, and in addition, the Q1 news flow has seemed very positive commercially:

14.1: The wellbeing services counties of Pohjois-Savo and Pirkanmaa acquire Finland’s leading automation solution for archiving Uranus systems – total value of contracts €2M

28.1: Digital Workforce delivers a transformative agent automation solution to a leading Nordic large corporation

11.2: Digital Workforce signs a $1.4M annual value contract with a U.S. healthcare organization – client size is comparable to European national health systems

24.2: A large insurance company implements an AI agent provided by Digital Workforce for personal injury claims processing; no hallucinations in the production pilot

The question then is, why is the stock still reacting so negatively?