A growing telehealth company from the Canadian Venture list, founded in 2013. The company operates in an interesting sector; for example, ARK continuously invests in the larger TDOC. Its share price boomed 5x in a short period last autumn but has somewhat receded since. The company constantly makes acquisitions, largely paid for with shares.

+Growing industry

+Teams want to join on a share-based model - Belief in growth exists

+Large North American markets with significant room for development

+100M CAD in cash

±Share price at the mercy of retail investors; there’s also upside if institutions become interested

-Small player

-Small market cap

-Much integration due to acquisitions

I see great potential if things go well; it goes without saying that the stock is risky. It’s in my portfolio; I bought it at 1.77 CAD from Toronto.

Discussion about CloudMD and the telehealth sector in general? Company presentations show that the entire industry is in its infancy in North America. For example, on the CEO.CA forum, it was highlighted that CloudMD allowed prescriptions to be faxed to the patient’s desired pharmacy…

I’ve been eagerly awaiting this to arrive here.

It’s been in my portfolio since last autumn, but I sold it when it started to drop and have now bought back in.

Indeed, they’ve diluted a lot due to acquisitions, but now they’ve started talking about organic growth, which should start materializing.

The CEO seems very focused based on the interviews I’ve watched, and he’s busy. They want to own everything they offer: their own software, services, and staff.

Apparently, it’s the only platform? Where you can input a local Kela card (Finnish social security card - perhaps referring to a Canadian equivalent like a health card) and access both public and private sector services in that part of the world.

Users have praised the app, saying they won’t go back to the old way. Apparently, it’s only in use in a small part of Canada so far. The CEO has said the app is ready and could be opened for wider use immediately, but they apparently need more clinics and staff before expanding, to ensure things run smoothly.

You can apparently choose a man or a woman, someone who speaks the same language, is in the same time zone, etc.

A wide range of services for patients’ different needs.

The last share issue was at CAD 2.70, and the current price is CAD 1.84.

Staff, their families, and close ones have bought/are buying shares, from what I understand, and the CEO has talked a lot about Amazon as a potential buyer someday, which is quite speculative but still worth noting.

Wearables, like Apple Watches, etc., are coming, which can measure some vital functions.

These are just a couple of points that came to mind. Indeed, there are not many institutional investors involved yet, so it’s all in the hands of citizens, but it has been one of the most traded stocks in Canada in recent months, at least on the Venture Exchange.

Some price target was given, but I don’t recall it at the moment.

Here’s a good article about the company. It covers background information, acquisitions, and more. They have written a few articles (links can be found further down in the article). This one is older but more in-depth; newer ones can be found from this year.

Apparently, acquisitions have also established a foothold in China and India, but Covid put that on hold. Expansion into Canada and the USA is prioritized.

They will soon participate in an institutional conference.

"We are planning a TSX up-listing and have already started the process. Our new CFO, Daniel Lee, is streamlining all our financial processes and working on integrating all of the acquisitions we announced/closed/will be closing.

Realistically, it will be middle of 2021"

From their PR team

So, a marketplace change could be coming in Q2-Q3.

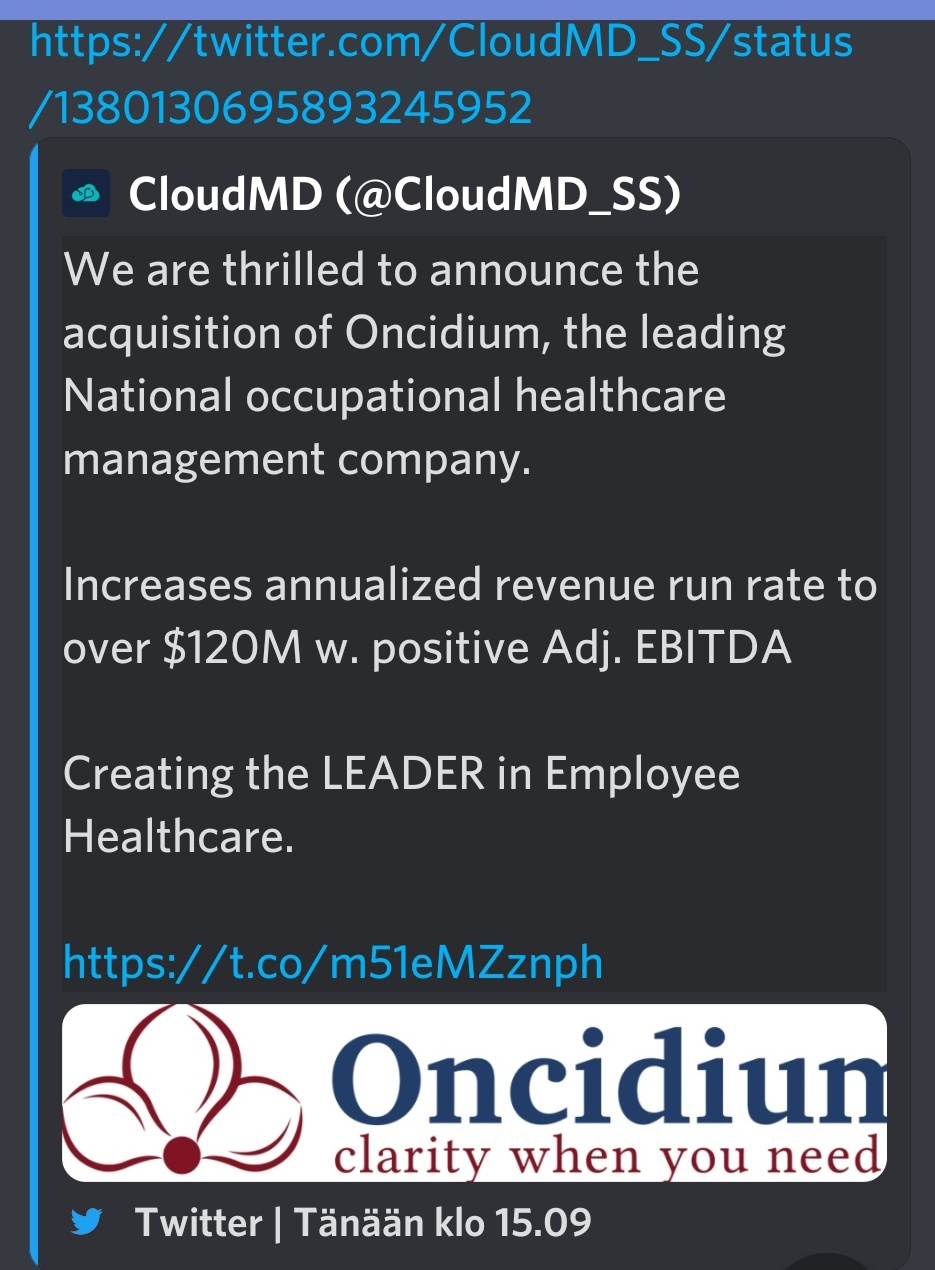

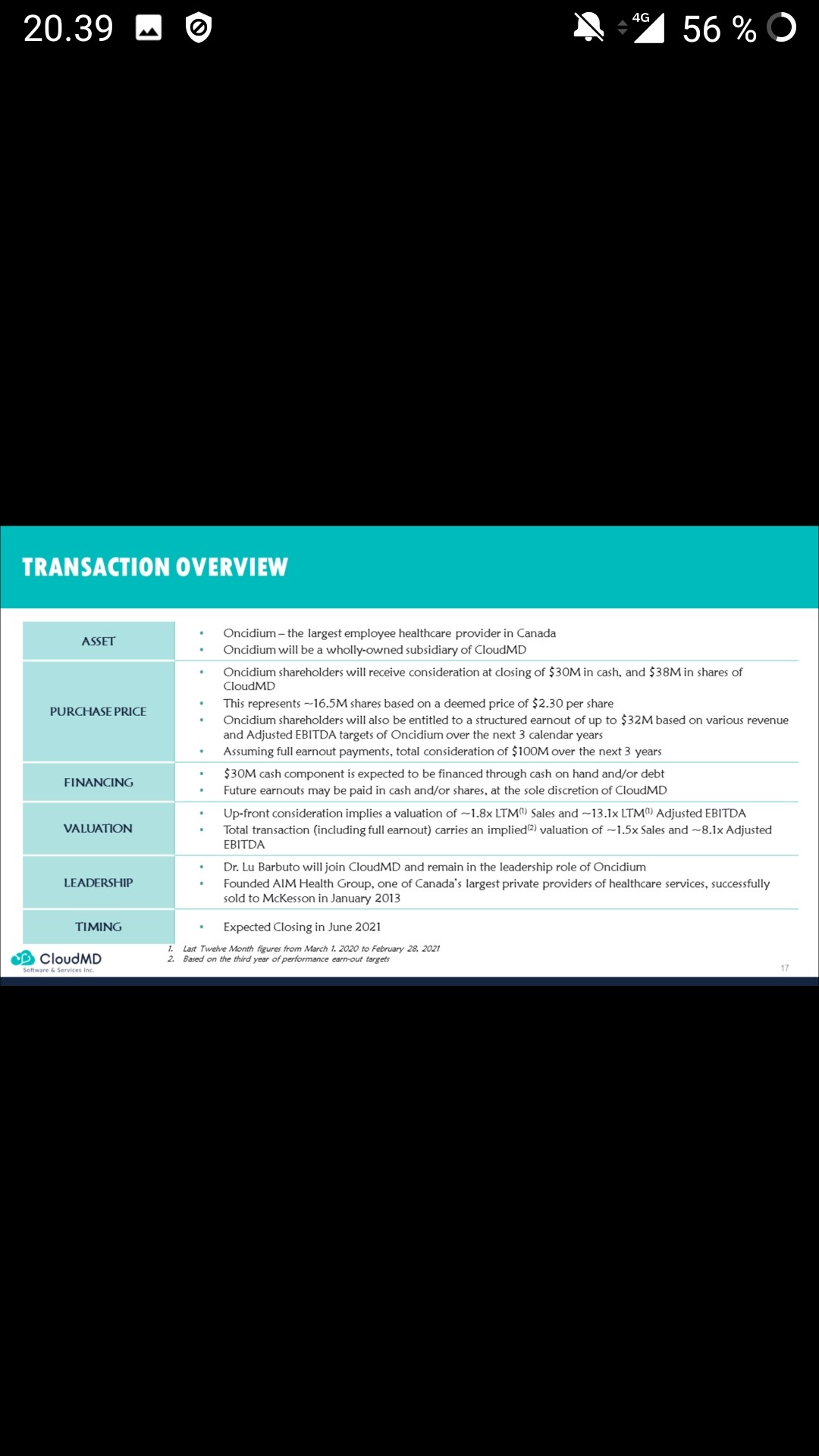

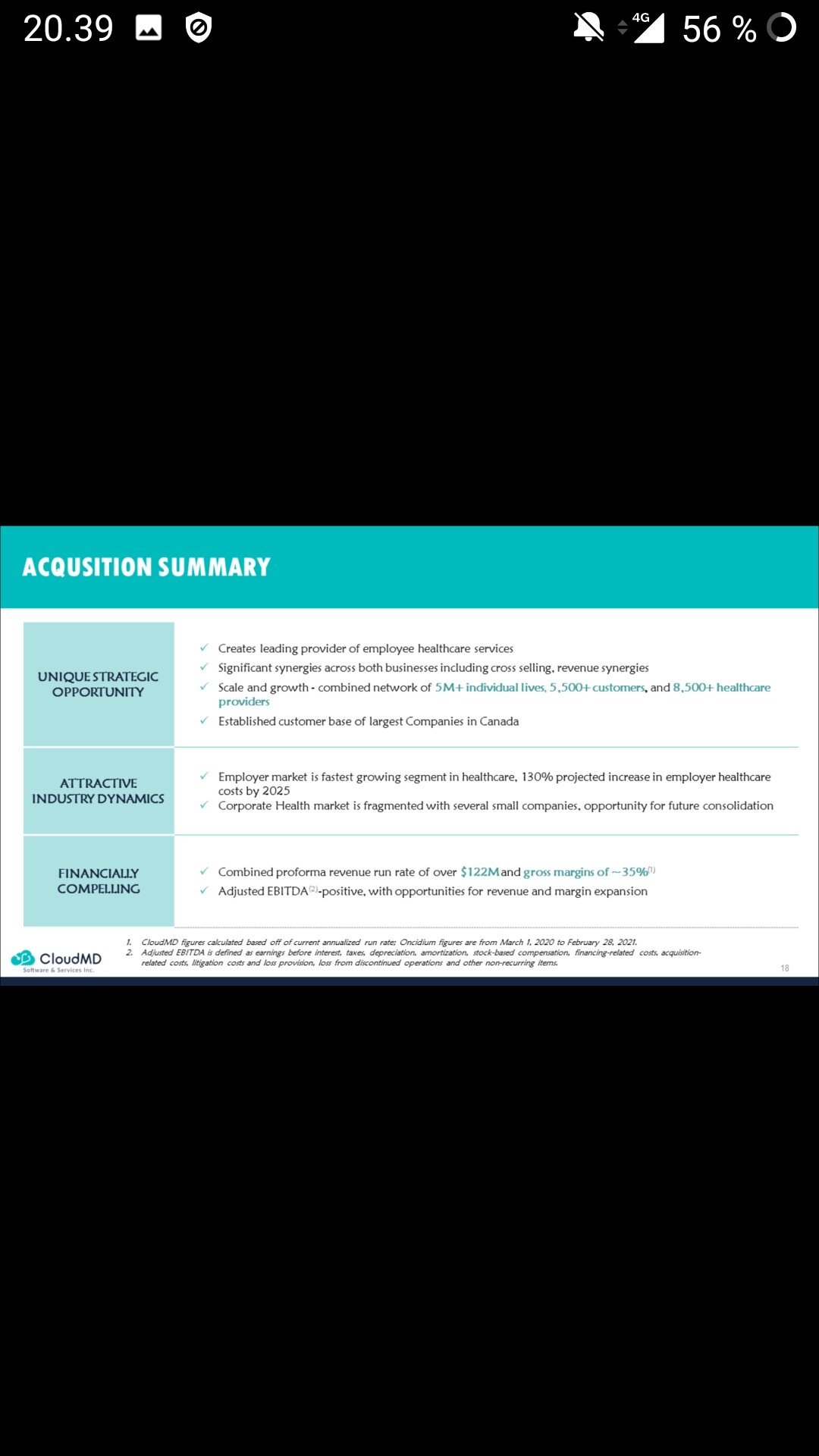

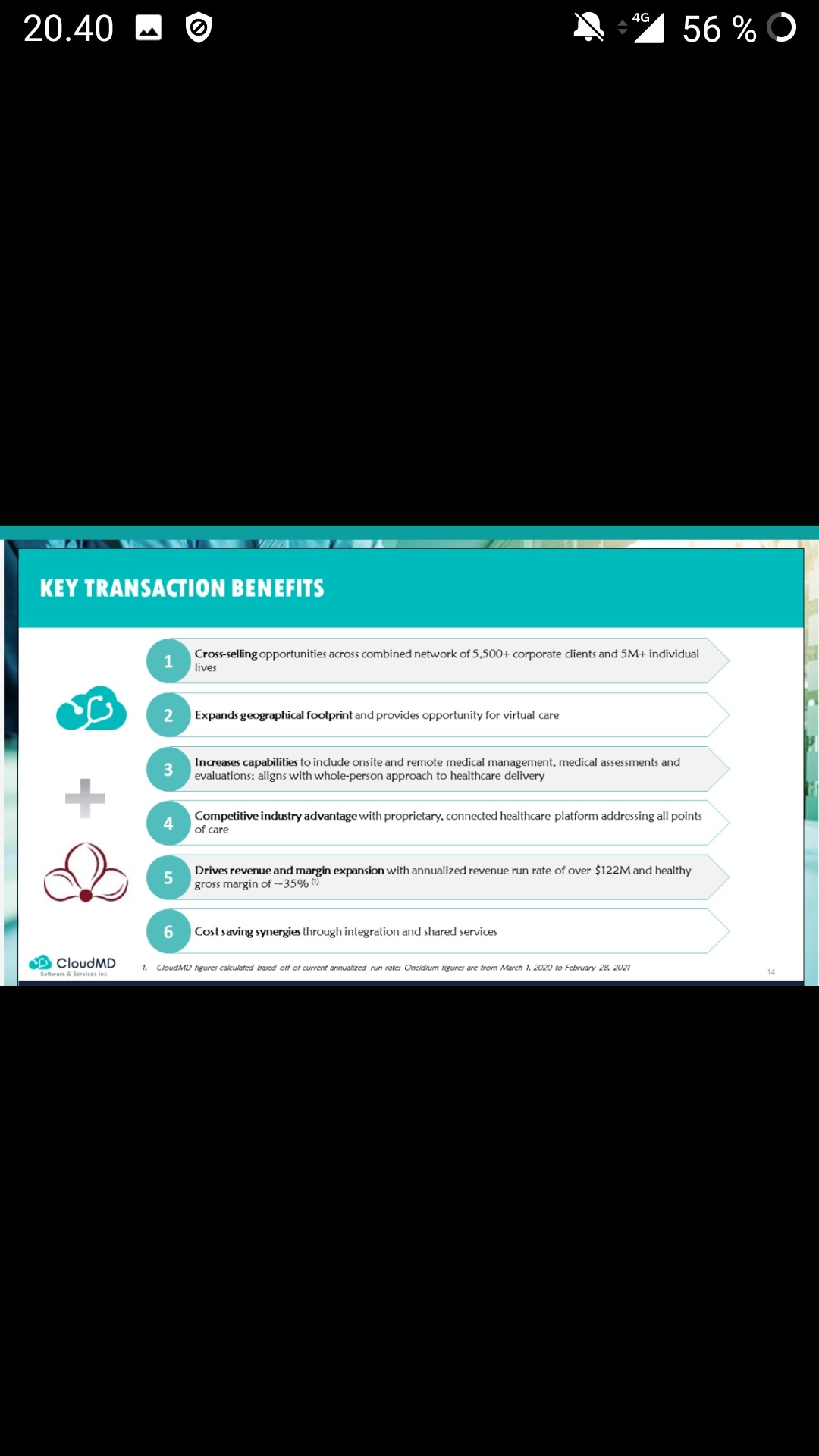

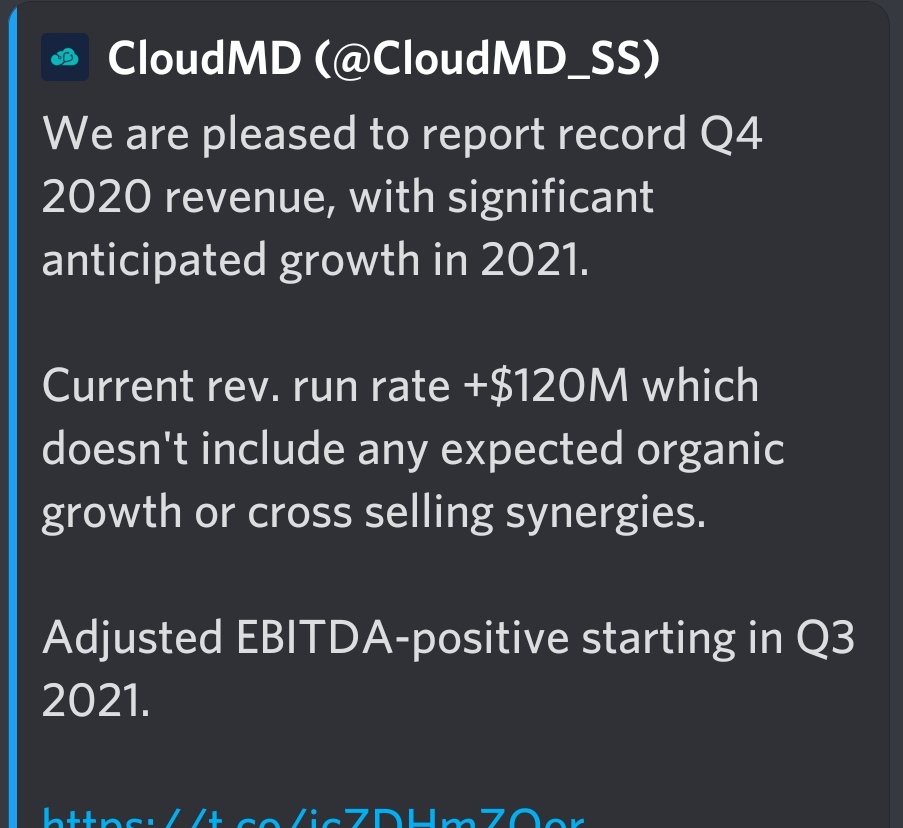

I didn’t get to comment on the results earlier; truly significant growth figures for 2020. It will be interesting to see the Q1 figures soon, especially since the company has been continuously making new acquisitions, and the $120M revenue run rate that the company has communicated is on a completely different level than last year’s figures. The risk in this growth, especially when it largely comes through M&A, is naturally the integration of the acquired businesses. Otherwise, based on Cloud MD twitter, they are constantly working at various conferences.

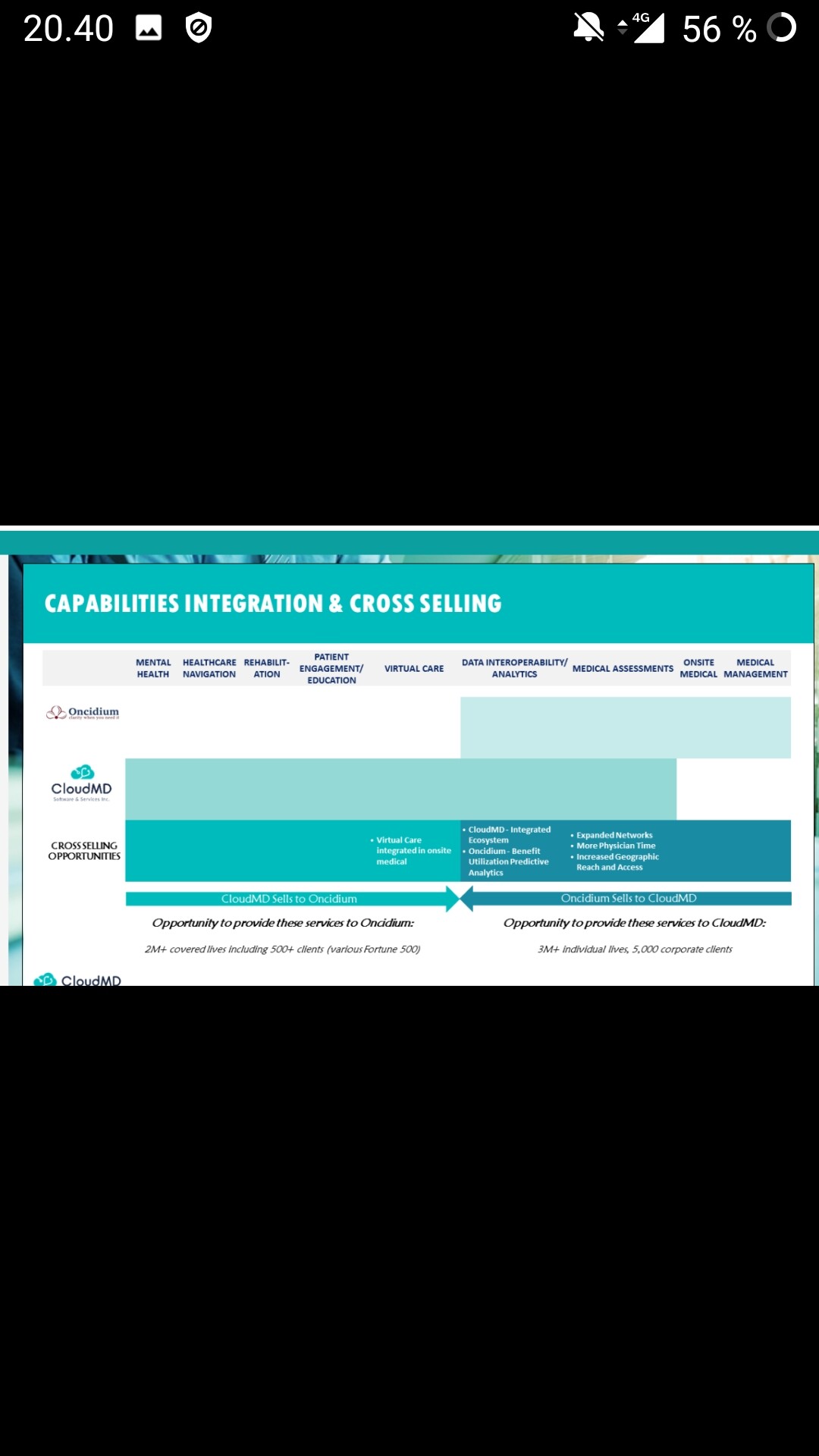

It will be interesting to see how organic growth starts to develop in the background. It seems that the acquisitions have been carefully made to support the “one-stop shop” principle and have already been profitable. I’m sure this will develop into a productive workshop within a few quarters. I don’t remember which ones were closed in this quarter, but some results should start to show from the seven acquired last year .

I have bought slices for the whole family for long-term holding.