Time for a review.

A few scattered observations:

-

Listed around 2007 via a ‘reverse merger’ through some not-so-lucky mining company

-

The original branding as a health drink failed, but it looked so successful initially that Coca-Cola, together with Nestle, developed their own ‘negative-calorie’ drink to compete with Celsius. Around 2010, there was a wave of lawsuits against these beverage manufacturers’ claims; CC & Nestle lost theirs and pulled the drink from the market, while Celsius won its trial—there was nothing fishy about the research results.

However, the lawsuit took a toll on the business, which is at the mercy of distributors.

-

Rebranding sometime in 2012 while delisted; the lead investor bought out the founders and brought in star-class executives who rebranded Celsius from a health drink to an energy drink (well, a health-energy drink).

-

Apparently the only company that has gone down and back up every step of the ladder from the list (Nasdaq) to being delisted, and from delisted back up again; I don’t remember the exact ladder (‘penny-stock etc’), but the CEO goes through them in the interview.

-

Unlike more traditional energy drinks, Celsius is a ‘health-energy drink’ rather than a hyper-masculine brand where the drinker jumps out of planes or does triple-ollies (I haven’t skated, as you can tell from the terminology) from one rooftop to another. Thus, there is no gender preference.

History:

2008

Distribution in Chicago, Detroit, Boston, Los Angeles, etc. Revenue 2.5M, loss just over 5M.

2009

Raising capital by shuffling Series B, raising the stakes. Testing demand through Costco and other big chains; full gas if it’s there. A loss of nearly 8M on revenue of just under 6M. (2M increase in accounts receivable)

2010

Revenue just over 8M, loss ~20M. Loss due to national marketing stunts including TV, apparently implemented because experiences with ‘penetration’ in big chains were good.

2011

Hit the ground, deregistered.

2016

Back in the game, 15M in equity, revenue about 23M and loss of 3M (the re-registration shows a few years back, some millions in losses made there too)

2017

Revenue 36M (+59%), loss 16k. 20M in equity.

2018

Revenue 57M (+45%), loss 11M (Large international marketing campaigns). 12M in equity.

2019

Revenue 75M (+43%) Profit generated 10M. 25M in equity. China distribution deals made (expensive). Shares sold for 26M (I guess an offering or something, can’t be bothered to check).

2020

Revenue 131M (+74%). Volume starts to significantly improve gross margin. Some ‘note’ thing related to China distribution deals dropped the profit by over 10M, profit just under a mil. Just under 70M in equity.

Cash flow looks strange due to China stuff. 4M acquired by using ‘stock options’ (cash flow statement). Possibly related to compensations, which were 6M. Dilution anyway.

2021

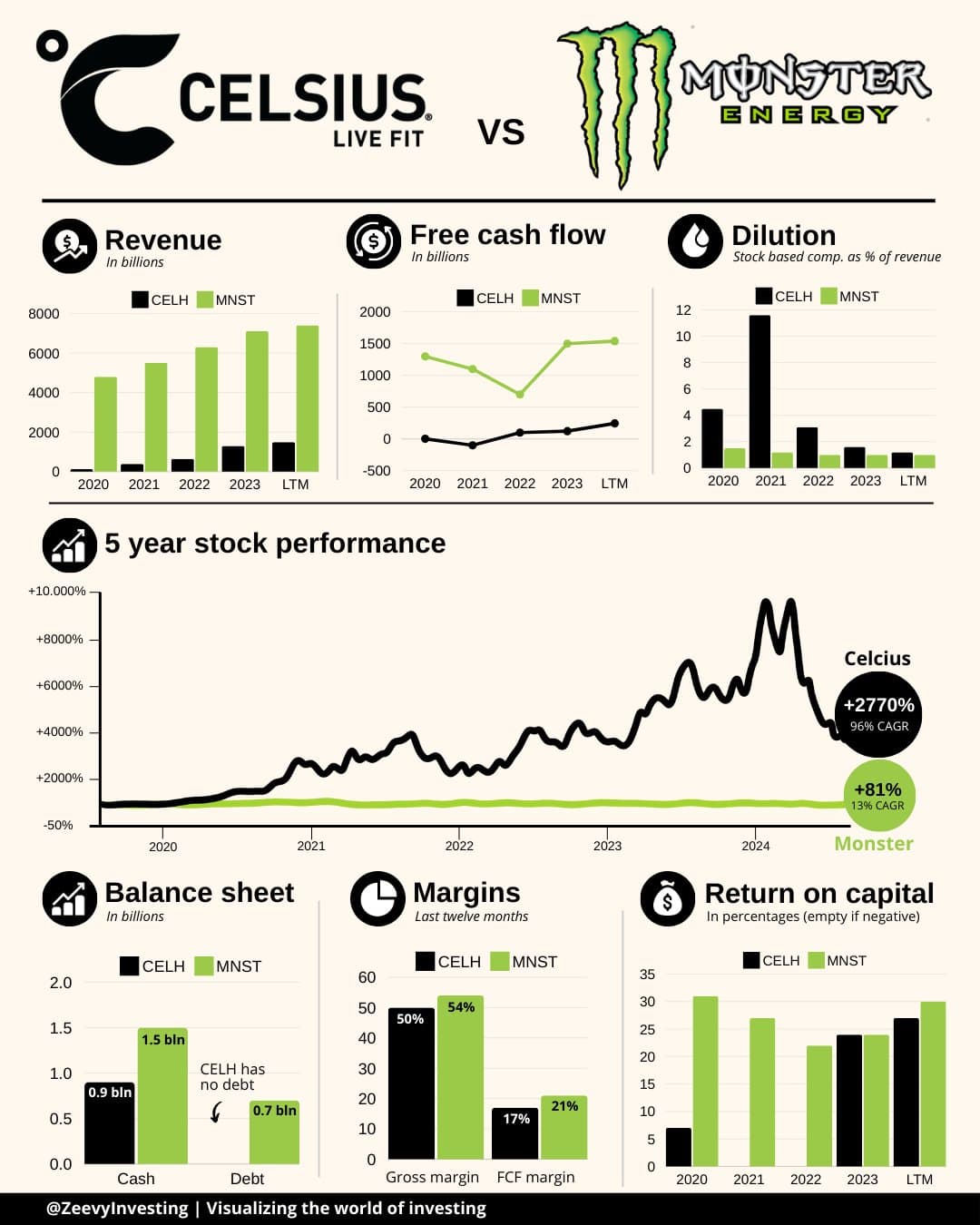

Revenue 314M (+140%), growth almost entirely from the US (97%). Gross margin decreased ~6 percentage points because cans (aluminum) became more expensive. Marketing +110% YoY (year over year), i.e., 75M. Stock options (compensation) tripled YoY. Profit ~4M. Balance sheet positive by 165M.

2022

Revenue 654M (+108%), growth from the US and marginally from Asia, decline in Europe. Loss of 200M. Marketing budget 353M (+372% YoY). Balance sheet 860M in the black (over half a billion from the Pepsi distribution deal). Cash flow 100M.

In the cash flow statement, over half a billion in share capital dilution to Pepsi. Pepsi deal entered the picture from August.

2023

Revenue 1.3B (+102%). US +105%, Europe +41%, Asia +30%, and others more than quadrupled. But everything else is tiny compared to the US. Gross margin jumped close to 50% due to ‘efficiencies in raw material sourcing, and product waste reduction’. Profit just under 200M. Balance sheet over 900M in the black.

Cash flow 100M - if you adjust for the growth in receivables (the assumption being that all the money will be received that was pushed on credit in 2023 + another assumption that it doesn’t stay rotting on the retailer’s shelf, which would burden the following year’s sales accordingly), you get over 200M.

2024

Q2 New distribution agreements here and there around the world. Balance sheet: approx. 900M in the black. H1 2024 758M (+30% vs. H1 2023). Pepsi apparently has some issues with distribution stuff. Profit H1 132M (+80% vs. H1 2023).

H1 cash flow is a ballpark figure around a quarter billion.

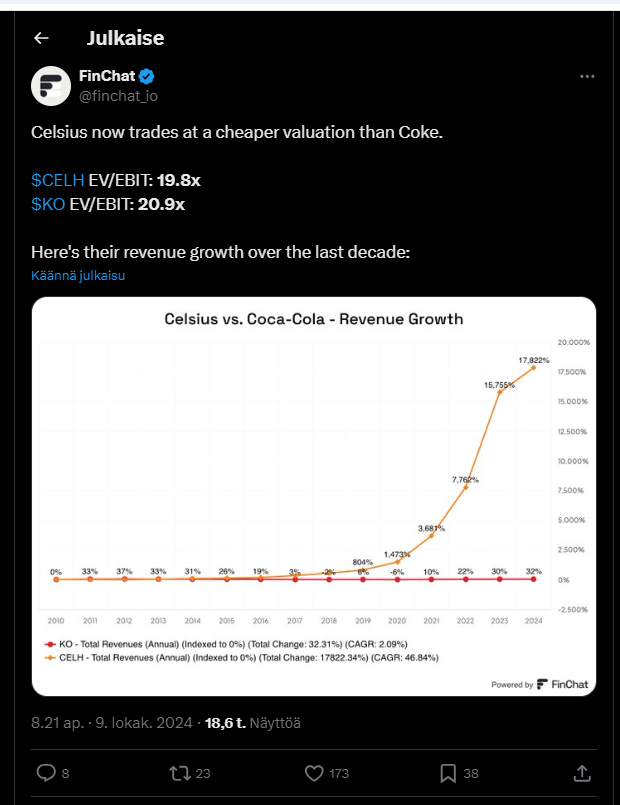

Taking into account errors in assumptions and calculations I might have made, I could ballpark the current valuation at ~15-20 * annual cash generation.

My own experience with the product is that it smells and tastes like acidic fruits (good!), there’s none of that weird mix of axle grease, gear oil, and butt crack in the scent that I’ve sometimes smelled when someone opens a more traditional energy drink nearby.

(a very subjective evaluation  )

)

I don’t know if this is useful to anyone else, but I wanted to do a small review myself because I find the company interesting

A few informative links:

Excellent review of the rebranding:

(73) The Strategy That Broke Celsius’ 10-Year Slump - YouTube

Interview with the CEO; he knows the history well even though he wasn’t there from the start:

Celsius CEO: From Near Bankruptcy to $10B Company (youtube.com)

[FULL PODCAST]")