Cambi announced it would publish its Q3 report on Thursday, Nov 7, but it popped out already on Wednesday, Nov 6, at around 6 PM Finnish time. The same phenomenon occurred in Q2 as well. A curious habit for the company. Apparently, many in the market didn’t notice this, as only 12 trades were made after six, with a total of 812 shares changing hands.

The investor call is tomorrow at 11 AM Finnish time.

Key observations

-

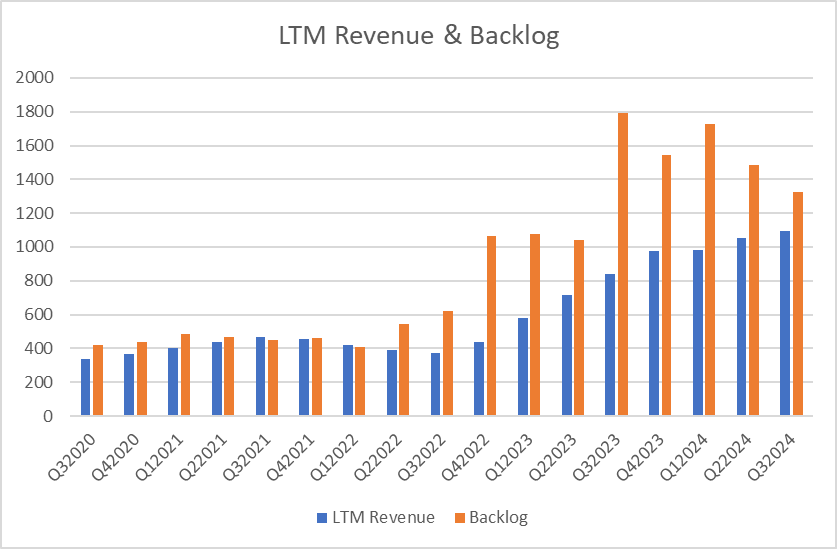

Revenue grew 18% YoY, but declined just under 10% from the previous quarter.

-

No new orders were received, so the order backlog decreased for the second consecutive quarter. Now down by about 10%.

-

Service order intake naturally fluctuates less than the project-based Technology side.

-

Cash reserves had decreased by 85 MNOK, as inventories were increased and apparently some other working capital-related items have accumulated.

-

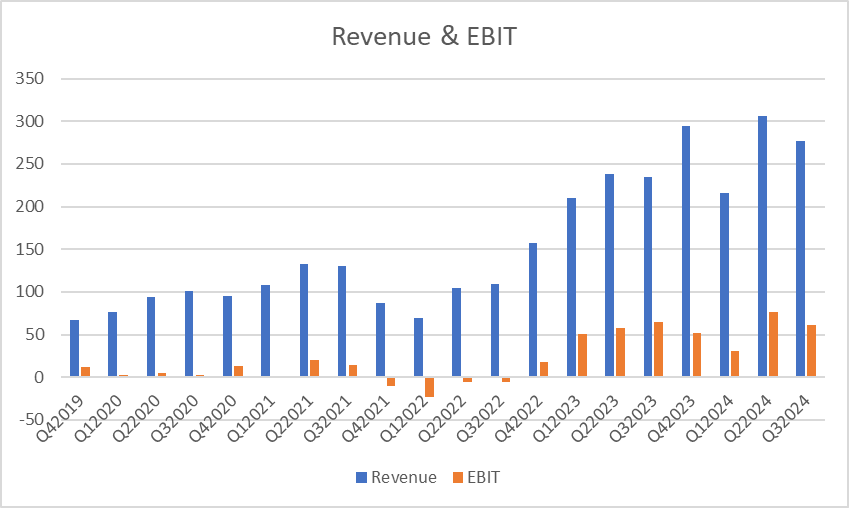

The company has invested in personnel resources, and personnel costs grew by over 40% YoY (41.9 MNOK → 59.3 MNOK). In Technology: 34 → 46.6 and in Solutions: 7.9 → 12.7.

-

Solutions had increased sales of the soil product from 66t to 81t.

-

An interesting observation is that the Lviv project in Ukraine restarted after being on hold for obvious reasons.

-

The CEO left, as I understand it, of his own accord. The founder and main owner (Chairman of the Board) became the CEO, and a representative of the second-largest owner became the new Chairman. It would be nice to know more about these arrangements and plans.

-

Amidst the shake-up, the company’s visual identity changed, including the logo and website.

=>

=>

-

In the UK, a five-year Asset Management Period (AMP8) is beginning, which is expected to bring business to Cambi as well.

Graphs

Speculation

On trailing 12-month figures, EV/EBITDA is around 9.5, while for competitors it hovers around 11–13 for 2025 and 2026 according to DNB. Quite a decent situation, but closing that gap would probably require growth in the order backlog. So far, nothing more has been said about that other than that investments have been made in human resources regarding sales, marketing, and production, plus there was a mention of the UK potential. Otherwise, there was only a vague “there is interest” comment.

So, most likely no rocket-like surge is expected, but there probably is some kind of potential.