MarketScreener on julkaissut tänään aamulla iltapäivällä Suomen aikaa (06:49 am EDT) tällaisen, joka näyttäisi aidolta Cadelerin Q1-rapsalta, päivää etuajassa vain. ![]() Yhtiön omilla sivuilla ei toki tätä ole. Liittyykö tämän päivän iso droppi (-8%) tähän?

Yhtiön omilla sivuilla ei toki tätä ole. Liittyykö tämän päivän iso droppi (-8%) tähän?

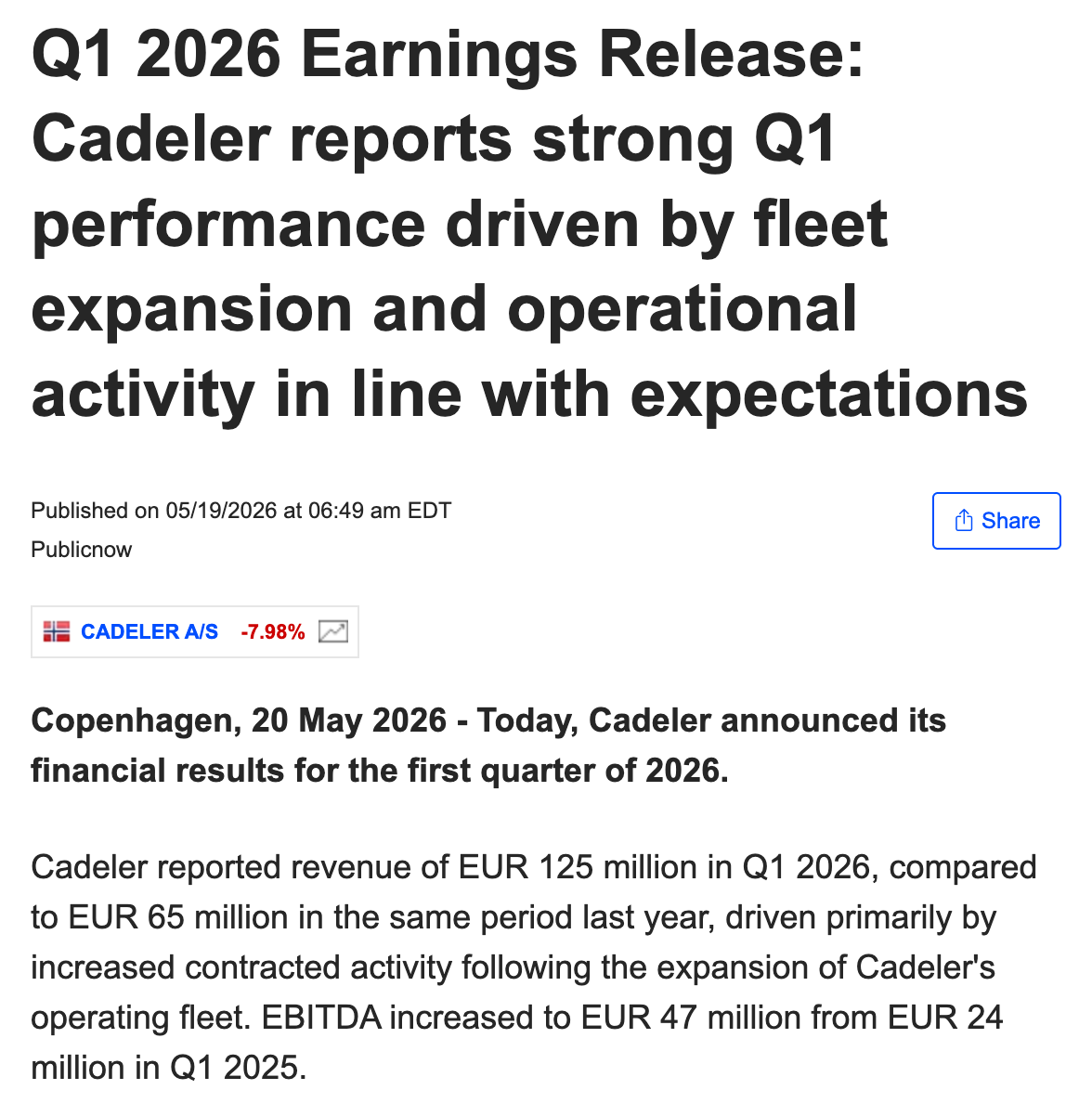

Edit: oletan että raportti on aito (vahingossa julkaistu etuajassa) ja markkina on tänään reagoinut siihen.

Käyttöaste laski vuodentakaisesta (55,3% → 47,6%) liittyen mm. Wind Allyn ja Wind Moverin siirtoon Aasiasta Eurooppaan sekä Wind Orcan huoltotelakointiin. Seurauksena esim. käyttökatemarginaali on “vain” 37,6%. Muuten näyttää omaan silmään hyvältä. Odotukset taisivat vähän lähteä lapasesta viimeisen parin viikon kurssinousussa.

Mikkel Gleerup, CEO of Cadeler, comments: “The first quarter of 2026 reflects the continued scaling of our business following the expansion of our operating fleet over the past year. While the integration of new capacity naturally impacts utilisation in the short term, we are seeing strong underlying operational activity across the fleet. At the same time, we continue to strengthen our financial platform and invest in the next phase of Cadeler’s growth - positioning Cadeler to support the increasing global demand for offshore wind installation capacity.”

Nopea katsaus (Google AI)

- Revenue at €125M: While nearly doubling year-on-year from €65M, it actually represents a near-term miss against analyst expectations of around €150M. Since the fleet doubled from 5 to 10 vessels, the top-line growth is driven by sheer capacity expansion rather than higher revenue per ship, reflecting significant transit periods.

- EBITDA at €47M: This lands at a 37.6% margin, which is the clear soft spot of the report when compared to the ~52% guided full-year average. It proves that having assets in transit or maintenance heavily penalizes near-term profitability, as fixed costs keep running while day-rates are paused.

- Utilization at 47.6%: This explains the margin drag. Less than half of the fleet was actively billing clients, heavily impacted by the transit times for Wind Ally and Wind Mover, alongside scheduled maintenance for Wind Orca.

- The Backlog and Guidance Safety Net: The €2.7B backlog remains the rock-solid anchor, with 82% locked into Final Investment Decisions (FIDs). Crucially, management reiterated the full-year EBITDA guidance of €420M–€510M.