There wasn’t a thread for Berkshire Hathaway on the forum yet, but undoubtedly the world’s most legendary investment company and investor story deserves one.

Berkshire Hathaway is an investment company steered by one of the world’s most successful investors, Warren Buffett. The company’s roots trace back to the textile industry and the 19th century, but Buffett entered the scene in 1962 and eventually took over the entire company. Ironically, the purchase of Berkshire Hathaway itself was, according to Buffett, one of the worst of his career, but at the same time, from a declining textile company, he built an investment empire that expanded into the insurance business and, with the help of the so-called “float” generated from it, into practically all sectors. Between 1965 and 2018, the share value has risen by an average of 20.5%, while the S&P 500 has risen 9.7% over the same period: $1,000 invested in 1964 would now be worth about $24 million.

We are talking about one of the world’s most unique index-crushing streaks.

Today, Berkshire Hathaway is among the top 10 most valuable companies alongside the likes of Apple, Google, and Amazon, which are perhaps more familiar to Finns; it employs over 300,000 people, and Warren Buffett is one of the world’s richest individuals.

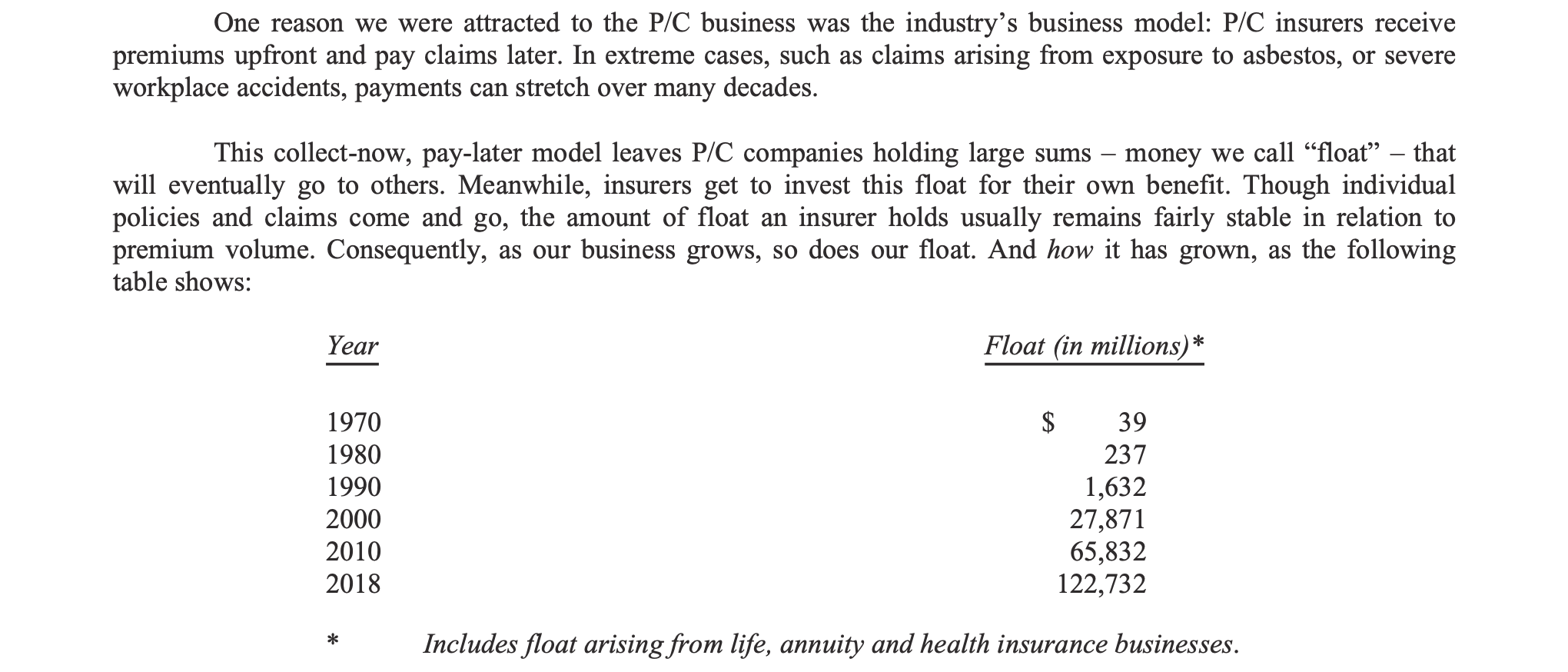

According to a study, Berkshire’s outperformance is explained, in addition to Buffett’s undeniably skillful stock picking, by the use of leverage: the “float” of the insurance companies owned by Berkshire—meaning the insurance premiums paid by customers—is reinvested, and on average, these do not need to be paid back for years, if ever.

“If his Sharpe ratio is very good but not superhuman, then how did Buffett become among the richest in the world? The answer is that he stuck to a good strategy—buying cheap, safe, quality stocks—for a long time period, surviving rough periods where others might have been forced into a fire sale or a career shift, and he boosted his returns by using leverage. We estimated that Buffett applies a leverage of about 1.7 to 1, boosting both his risk and excess return in that proportion. Thus, his many accomplishments include having the conviction, wherewithal, and skill to operate with leverage and significant risk over a number of decades.”

Buffett himself raves about his float in every shareholder letter, and for good reason.

Regarding Berkshire, it’s good to understand—at least in my modest opinion—that the company’s character has changed significantly throughout its history along with Buffett’s investment style and the limits set by the company’s size: while Buffett is perhaps most famous as a value investor, Berkshire’s style shifted decades ago to emphasize quality companies with deep moats when they can be bought at a fair price. Such successful investments in the past have included, for example, Coca-Cola, which remains one of the largest holdings.

As the company’s size grows, acquisitions must be increasingly larger to move the needle. In practice, this means several tens of billions. Despite a stock portfolio of approximately $170 billion and his fame for stock picking, the company increasingly owns 100% of its subsidiaries. Berkshire Hathaway resembles a conglomerate with highly decentralized decision-making, where independently operating subsidiaries pay dividends to the parent company, and capital allocation is almost entirely centralized under Buffett.

It is also worth noting for investors who look at book value: the value of these wholly-owned companies does not appear on the balance sheet in the same way as public holdings, which is why intrinsic value has diverged increasingly from book value:

To conclude this long opening, here are a few concerns regarding the company, even though it has been built into quite a fortress.

-

Due to its massive size, it is also increasingly difficult for Berkshire to outperform the index; in fact, over the last 10 years, it has even lagged behind the S&P 500 total return index.

-

Warren Buffett and his partner Charlie Munger are already 88 and 95 years old. Responsibility has already been shifted at Berkshire, but Buffett’s aura is unique. Whoever the successor in capital allocation may be, they will have big shoes to fill. Buffett has also been forgiven a lot by investors, including fairly minimal external reporting: will a successor be forgiven and understood in the same way?

-

Berkshire Hathaway is no mecca of innovation; it is focused on very “traditional” industries or brand companies. The recent Kraft Heinz price crash shows how disruption and changing trends hit more and more sectors. Are the companies in Berkshire’s portfolio agile enough?

-

Lack of technological expertise: Buffett’s venture into IBM did not go well, and the Apple holding has also been criticized. However, the weight of technology in the index is high, which likely partly explains why Berkshire has lagged behind over the last 10 years.

Quite a long opening—what thoughts does the company evoke in other fellow commenters? ![]()

P.S. Berkshire’s model has also inspired a host of “mini-Berkshires” or copycats. The most successful of these is likely Markel. In the tech world, Google has occasionally floated the idea of being the Berkshire of technology, and in Asia, Tencent has also been compared to a “technology Berkshire Hathaway.”

P.P.S. Buffett’s shareholder letters are very educational; I can only recommend devouring every one of them. ![]() They can be found here http://www.berkshirehathaway.com/letters/letters.html

They can be found here http://www.berkshirehathaway.com/letters/letters.html