This is a truly interesting case, for a couple of reasons.

From Berkshire’s perspective, it shows a certain weakness in seeing trends and bigger changes in consumer habits. Ready meals, especially Kraft Heinz’s awful jarred foods and packet soups, have clearly gone out of fashion as consumers have moved towards healthier and organic options. This trend has been discernible for quite some time! So, is there a weakness in Buffett’s methodology? Could this also be reflected as a risk in Berkshire’s Apple strategy?

From Kraft Heinz’s perspective, it will be interesting to see if these companies can renew themselves and reposition. In practice, they would need to renew their image and product portfolio. Large companies have resources, but on the other hand, large organizations can be difficult to change.

McDonald’s succeeded incredibly well in this, a truly brilliant performance. McDonald’s renovated its restaurants from awful plastic messes to much more pleasant wood paneling, etc… They brought in a bit of design and healthier options, and renewed their brand and marketing strategies. But they didn’t really have to touch the core products. Big Macs, double cheeseburgers, and Happy Meals are still being churned out, even if the commercials rave about snack carrots.

From Kraft Heinz’s perspective, it will be interesting to see if a successful image renewal can be done without having to retool production lines with large capital expenditure. I don’t know if producing a healthy jar meal is very different from some packet soup or jar noodles…

Certainly a closely watched company due to Berkshire. From what I saw during the previous earnings release, Buffett was squirming uncomfortably when answering the journalist’s questions. What will correct this stock price drop? The earnings report seems to be on October 28th.

Good point. The McDonald’s analogy would probably work well for KH too. I’d guess that making a healthier version of the current product is both technically easy and cheap. But then there are a couple of bigger problems: firstly, they would have to invest heavily in product development, which costs money, and secondly, inform consumers about the change (i.e., market it). Altogether, we’re talking about a significant investment, making it clear that the company should focus only on its strongest brands and sell off the smaller ones. A few major brands can be rebranded, but updating KH’s entire brand collection would be an impossible task.

Buffett’s mistake at the time was expanding Heinz’s higher-quality portfolio with Kraft’s lower-quality product portfolio. And at that time, the change in retail, where only the best brands get on shelves and mediocre brands are replaced by private labels, wasn’t perhaps fully visible. Heinz ketchup is even available at Lidl, but many other smaller brands are not seen much on the shelves. Consumer brand loyalty has weakened (I myself buy private label alternatives for many products).

Buffett has often said that it’s better to avoid difficult problems than to try to solve them. At KH, Buffett now has to solve those big problems; we’ll see what he (and 3G) come up with. In any case, ownership stakes of 26.7% + 20.1% are a big motivator to find solutions.

The funny thing is that ketchup, for example, has been studied, and its lycopene has been found to be healthy and to lower harmful LDL cholesterol. Some claim that it and crushed tomatoes are healthier than fresh tomatoes. So, HeinzK would only need a few product changes and, for the most part, storytelling = fact-telling. Here’s one hit:

Is tomato ketchup good for your heart?

Dipping your chips in red sauce, or catsup if you are feeling fancy, may have unexpected health benefits.

By Susan Blackmore

Whether it’s as good as the real thing is another matter, since fresh tomatoes also contain many other healthy ingredients.

Asked by: Clare Matthews, Canterbury

Tomatoes and tomato juice are known to reduce blood levels of low-density lipoprotein – or ‘bad cholesterol’ – and so reduce the risk of heart disease. But can a thick dollop of ketchup have any such positive effect? Apparently it can.

The pigment that provides the red colouring in tomatoes is lycopene, an anti-oxidant that helps prevent cell damage and inhibits heart disease. Ketchup contains lycopene, with organic and dark red varieties containing the most. In some experiments people’s levels of LDL fell in just a few weeks of eating extra ketchup.

Whether it’s as good as the real thing is another matter, since fresh tomatoes also contain many other healthy ingredients.

I’m not really thrilled about these brand houses, especially in the food sector. Globally, stores are bringing their generic versions to consumers at an affordable price, and more and more people are opting for them. This is also clearly visible in the results and sales figures of these companies, which have been relatively anemic for some time, considering the favorable economic situation.

Yeah, with a product potpourri like this, it’s certainly not easy to freshen up the image

They’re pretty strange. Except for ketchup, HP sauce, Philadelphia, mayo, and Jell-O. Even those aren’t regular items in my shopping cart. They seem to be focused on the American market.

For some reason (I don’t know why) it feels like many food brands are local things. For example, Fazer’s Blue is an iconic chocolate brand in Finland, and even after decades, big international brands haven’t been able to overthrow it. I think (I don’t know) that many of the brands mentioned above are local celebrities that have less of a foothold elsewhere in the world. Ketchup is an exception to the rule in this case.

Then there’s the whole other spiritual matter of why brand loyalty is really strong in some product categories, and in others, stores’ own private labels are eating into the share of traditional brands at an accelerating pace. The strongest brands, such as Coca-Cola and Heinz ketchup, are “Buffett-like” brands that have enough power in relation to retail chains.

And these iconic products are also such that the recipes don’t change - the same production process grinds on year after year. The productization is quite top-notch, but Coca Cola will have to give up plastic quickly.

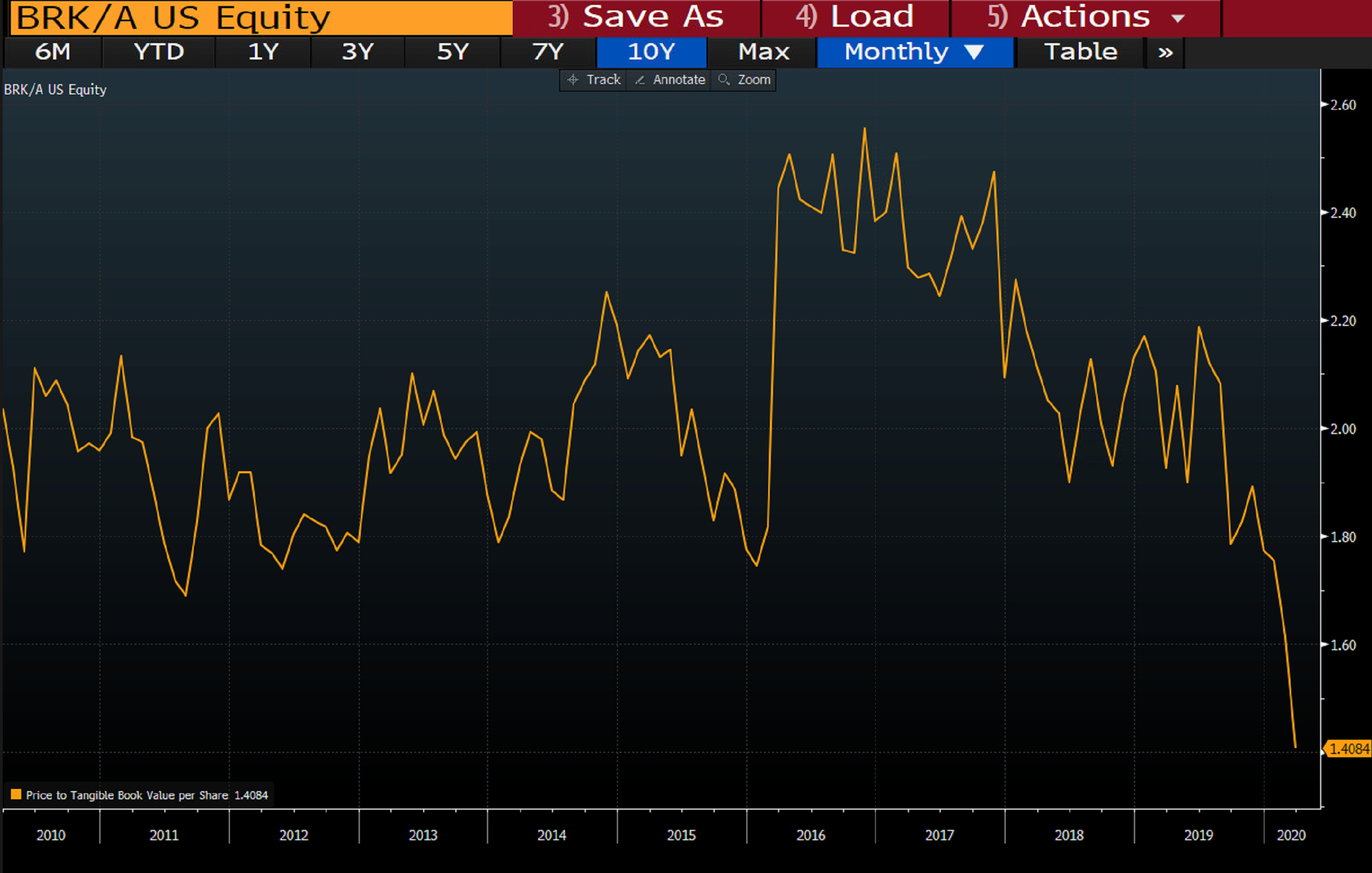

Wedgewood Capital’s patience with Berkshire ran out. I don’t agree with everything below; it’s written in a rather harsh tone, but on the other hand, Buffett is criticized so rarely that I’ll put it here to provide a critical angle on BKR:

Ten years of underperformance is probably the longest in Berkshire Hathaway’s history. Is patience wearing thin even for long-term owners?

Berkshire Hathaway would be at its best in a sideways market, as its stable parts still generate earnings. With a large cash pile and slow-growing companies, a bull market is like skiing with poorly gliding skis.

Berkshire Hathaway’s ten-year underperformance is largely explained by its oversized cash position and, in part, by its industry allocation – Buffett has invested heavily in the financial sector and railroads, which have different risks and returns compared to the high-performing technology sector. This, in turn, considerably reduces risk; Berkshire is currently somewhat like a balanced fund.

During the time I’ve followed this topic, every few years, there are critical statements like these, criticizing or advising Buffett. The first instance I remember was an “open letter” in 1997, and then during the dot-com bubble, there was also criticism about underperformance.

Criticism and challenging are good, but hindsight is not. The above text advises how Buffett should have invested in winning stocks. Anyone can retroactively pick the stocks that Buffett or anyone else should have invested in. Furthermore, anyone who has followed Buffett at all knows very well the reason why Buffett never has and never will invest in Microsoft – I find it hard to believe that these writers wouldn’t know this.

Berkshire and Buffett’s investment style are transparent and thoroughly analyzed – if one had known in 2009 that a long, technology-driven bull market was beginning, one would not have invested in Berkshire but gone all in on the technology sector. Everyone knew then what Berkshire was, where it invested, and that Buffett only operates within his area of expertise.

More than underperformance relative to the index, investors are surely concerned about the future – Buffett is 89 years old and Munger is 95. It’s clear that during the next decade, the “portfolio managers” will change, and Berkshire will pass into new hands, and through that, things will change.

And to clarify, in my opinion, criticism and challenging are excellent things, but being wise after the event, and especially advising with hindsight (about how Buffett should have invested) is not smart. But this is just my opinion, not some absolute truth

Agreed, hindsight is useless. Now it even made it to Arvopaperi (did it originate from here?)

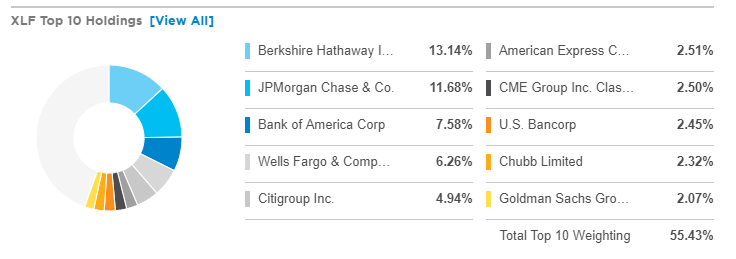

Instead, one can well question Berkshire’s overall investment track record, because the period of underperformance has now stretched so long (in the IT bubble, it was about a few years of massive underperformance, from which Buffett emerged relatively unscathed. If Berkshire had been a traditional Hedge Fund, it would have been closed then, along with many other value investors, now for 10 years. In addition, large investments have unluckily hit dinosaurs (IBM, Kraft Heinz) although there have also been huge successes on a large scale (Bank of America, Apple). That large size is just becoming a big burden, and several industries where Berkshire is active are undergoing disruption and change. Is a decentralized conglomerate, where capital allocation is tightly centralized in one pair of hands, a working model in a world of faster change?

Despite these weaknesses, as I already noted above, Berkshire would get to show its teeth in a sideways/bear market. Waiting for that. I used to own B-shares and I still keep an eye on them sometimes.

I don’t think the structure of BH is the problem as much as the lack of suitable alternatives and, of course, the company’s large size. Buffett wanted to make big acquisitions, but prices have continuously gotten out of hand. In the Private Equity sector, cheap money has driven prices high. Buffett just doesn’t want to overpay. On the stock side, the large size means that stock investments can only be made in large caps, and even then, only in the largest ones. Of course, one can do as with Precision Castparts: first buy a large number of shares and then take the entire company private. But even then, you have to pay a premium. Overall, with Berkshire, it’s important to remember that a larger portion of its market value now comes from sources other than BH’s publicly traded stocks.

At some point, the price level in the Private Equity sector will likely “normalize,” and then BH’s company structure will work well again, with more companies being bought into the conglomerate and funds distributed among them. I don’t see that the world has fundamentally changed; rather, it’s a problem caused by high prices. If the price level never normalizes, then it’s certainly better to distribute dividends and/or buy back more of its own shares.

And, of course, a big factor is what Buffett’s successors will be like and what their areas of expertise are. If they follow the same logic as Buffett, the company portfolio will change regardless, because their areas of expertise are different from Buffett’s. (Some indications of this have already been seen, for example, when one of the “portfolio managers” bought Amazon or DaVita.)

Buffett was recently asked about the amount of cash he holds in an interview. One point Buffett made was that Berkshire Hathaway is managed as if it were a shareholder’s only stock (which is true for many older investors). The company does not take risks that could lead to large, irreversible damage. He also emphasized that big opportunities don’t come very often, which means cash sometimes has to be held for longer periods. He compared the situation to one where, if cash reserves had been invested in, for example, an S&P500 index fund in 2007, the deals made a couple of years later would not have been possible.

Currently, Berkshire could be compared more to a hybrid fund than an index fund when considering the company’s risk profile.

Good joke, but no big outlines on how to get BRK back to the right 20% per annum level.

In my opinion, BRK needs to fundamentally reform in order to create shareholder value above the indices… Charlie & Warren are no longer capable of that.

Salvation could come from a bigger market crash where BRK could put its cash into play.

")