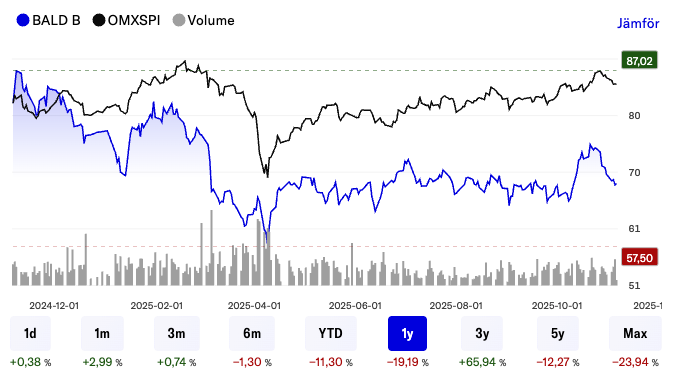

Hey! I’m curious about your general thoughts on the real estate sector, but especially on a Swedish listed company called Balder. Briefly, my thoughts: The real estate sector has undergone a significant transformation in recent years. After several years of record-low interest rates, rising property values, and high leverage, conditions changed rapidly when central banks began raising interest rates in 2022 and 2023. But now, in 2024 and 2025, the market has started to stabilize somewhat. Inflation has fallen back, and is it a good time for real estate stocks?

Balder was founded in 2005 and has since grown into a significant Nordic real estate group. The company operates as a long-term owner with local roots in residential, commercial properties, and new production in larger towns. Since its listing on Nasdaq Stockholm in 2005, Balder has transitioned from a smaller player to owning nearly 2,000 properties with a property value of over SEK 220 billion. The company’s strategy has been to combine its own management, local presence, and growth through acquisitions and development.

The CEO of Balder is Erik Selin, who has been with the company since its early days and is also a significant owner and a person many investors in Sweden are familiar with. It’s worth noting that Selin, through his large ownership and influence, has a strong commitment, which can be both a strength and an aspect to monitor from an ownership perspective.

A brief summary of Balder’s Q3 report:

-

Rental income: SEK 10,269 million (compared to SEK 9,543 million the previous year)

-

Profit from property management: SEK 5,176 million (previous year SEK 4,838 million), corresponding to SEK 4.03 per share (compared to SEK 3.84) for the parent company’s shareholders.

-

Profit after tax attributable to the parent company’s shareholders: SEK 5,851 million (SEK -117 million the year before) corresponding to SEK 4.92 per share.

However, there’s still a bit to prove after the report. For example, the solidity was below the company’s own target (38.2% vs target 40%) and Net Debt/EBITDA was also slightly above the target (11.9x vs target maximum 11x), which indicates some leverage risk.

And it’s a sensitive industry where the differences between companies are significant: players with high leverage or exposure to office properties in major cities have had a tougher time, while companies focusing on residential and community properties, like Balder, have fared better.

I’ve invested in the company this year as I think it’s an interesting position for the industry as a whole. Is there anyone here on the forum who has looked at Balder or any other competing company? ![]()