https://avtech.aero/pressrelease/avtech-publishes-key-figures-for-the-third-quarter-2025/

The preliminary Q3 figures came out from there, very good development still. The stock price already started to rise.

https://avtech.aero/pressrelease/avtech-publishes-key-figures-for-the-third-quarter-2025/

The preliminary Q3 figures came out from there, very good development still. The stock price already started to rise.

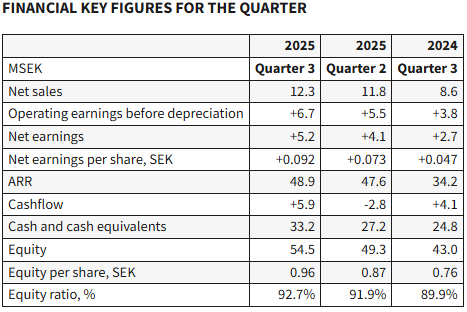

Epic 40% growth compared to the same period last year, “only” 5% relative to the previous quarter. ARR grew 30% to 51 million crowns. Earnings weakened due to recruitment.

“2025 was our strongest year to date, with approximately 2,200 connected aircraft and record levels in both net sales and earnings. During the year, Aventus and ClearPath were deployed with new customers, and we took important steps in product development, including the ClearPath app, new features for On-Time performance, and improved collaboration between the cockpit and ground operations. For the first time, we are seeing that the market is ready for expanded collaboration between airlines and air traffic control. During the autumn, we initiated the sharing of real-time data with air traffic controllers, and the initial results are very promising and further strengthen customer value. With strengthened organization, solid profitability, and a pipeline of customers in testing phases, we enter 2026 with strong conditions for continued growth. At the same time, we note longer decisionmaking processes among some customers in today’s more uncertain global environment. During 2026, we also expect new and expanded strategic partnerships that will enable new products and higher value for AVTECHs customers,” said David Rytter, CEO. “Full-year 2025 represents our strongest performance to date, and we are also experiencing growing interest in AVTECHs products. A Rule of 40 of 67.6 precent reflects a healthy balance between strong growth and profitability. The strengthened earnings development provides room for further broadening of the product portfolio.”, said Ingvar Zöögling, Chairman of the Board

According to preliminary figures, Avtech’s revenue decreased compared to the previous quarter in Q1’26.

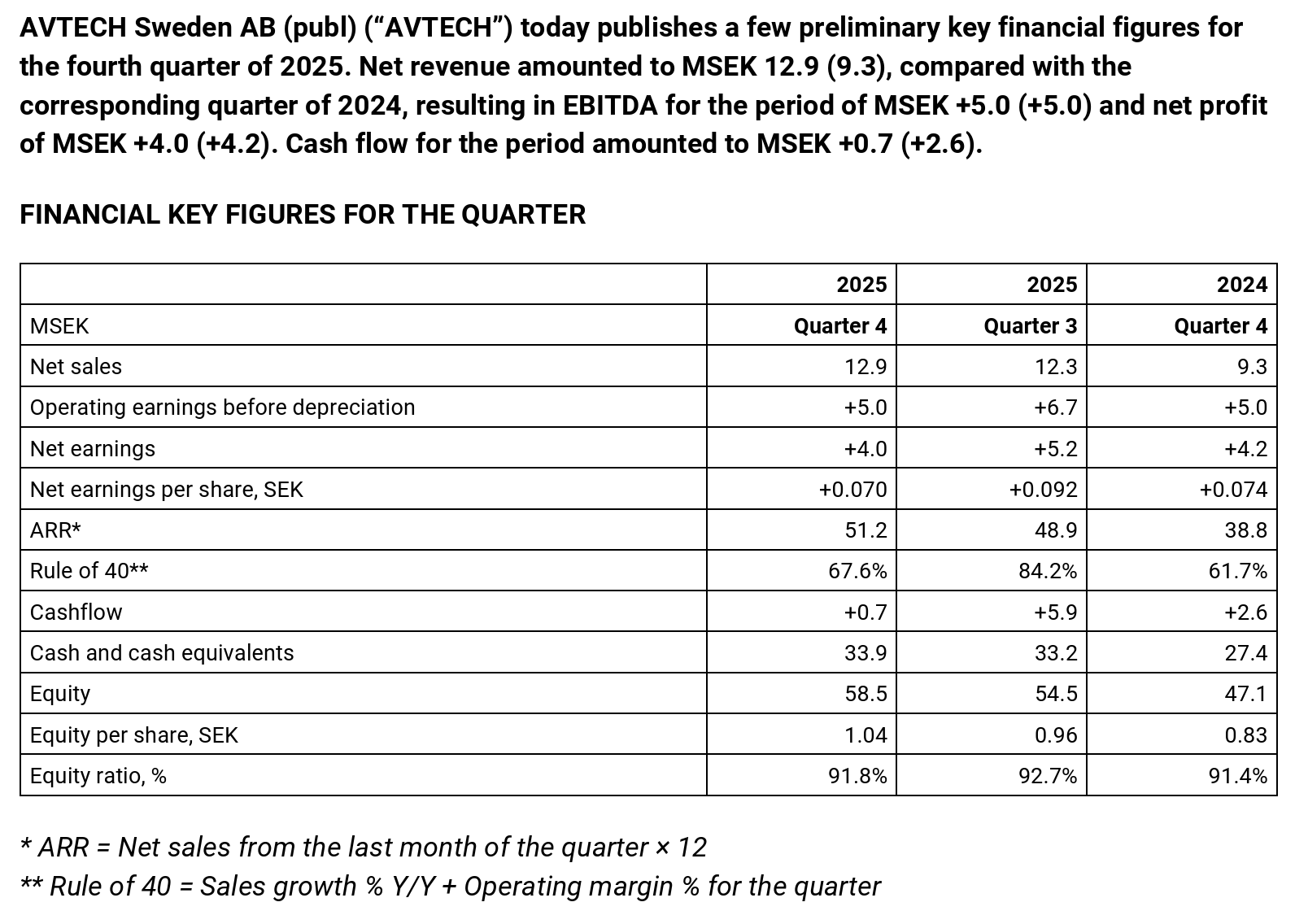

AVTECH Sweden AB (“AVTECH”) today publishes a few preliminary key financial figures for the first quarter of 2026. Net revenue amounted to MSEK 11.7 (10.5), compared with the corresponding quarter of 2025, resulting in EBITDA for the period of MSEK +4.7 (+5.1) and net profit of MSEK +3.8 (+3.7). Cashflow for the period amounted to MSEK +3.2 (+2.6).

FINANCIAL KEY FIGURES FOR THE QUARTER

| 2026 | 2025 | 2025 | |

|---|---|---|---|

| MSEK | Quarter 1 | Quarter 4 | Quarter 1 |

| Net sales | 11.7 | 12.9 | 10.5 |

| Operating earnings before depreciation | +4.7 | +5.0 | +5.1 |

| Net earnings | +3.8 | +4.0 | +3.7 |

| Net earnings per share, SEK | +0.068 | +0.070 | +0.065 |

| ARR* | 49.4 | 51.2 | 47.2 |

| Rule of 40** | 43.3% | 67.6% | 68.1% |

| Cashflow | +3.2 | +0.7 | +2.6 |

| Cash and cash equivalents | 37.1 | 33.9 | 30.1 |

| Equity | 62.3 | 58.5 | 50.8 |

| Equity per share, SEK | 1.10 | 1.04 | 0.90 |

| Equity ratio, % | 92.5% | 91.8% | 92.8% |

Reason for the decrease:

Quarterly revenue was impacted by negative currency effects and by Latam pausing the Aventus service for an in‑depth re‑evaluation, which resulted in slightly lower revenue during the period compared with our underlying run rate and the previous quarter. This pause should be seen as part of a customer‑driven evaluation process in which we work together with the customer to ensure the right conditions for continued operational value. This does not affect the more extensive delivery of ClearPath to Latam. At the same time, Wizz Air increased the number of aircraft using Aventus, which had a positive impact on revenue. Wizz Air is a clear validation of the operational value of the Aventus solution and of our ability to scale within existing customer contracts.

Redeye published a quick comment on the Q1 results and an interview with CEO Rytter (22 min) on Friday, as well as an updated analysis today (all available for free but require login):

In the interview, analyst Rasmus Jacobsson asks about, among other things, the LATAM Aventus re-evaluation.

In Redeye’s view, the market is potentially overreacting and pricing in the loss of the entire LATAM Aventus contract. The current share price is close to the analyst’s no-growth case.

Redeye estimates a full Aventus loss at ~SEK2 per share in fair value. The share has fallen ~SEK2.3 since the key figures release, implying current pricing already assumes the worst. With LATAM unresolved rather than lost, Redeye views risk/reward as skewed to the upside.

Redeye reduces its base case to SEK9 (SEK10), with a bull case of SEK13 (SEK15) and bear case of SEK5.5 (SEK6). EV/EBIT NTM of 13.5x sits below the five-year average of 16.5x. The no-growth implied price — based on Q1 ARR and a 34% EBIT margin — is SEK5.6, approximately 15% below current levels. Net sales estimates are reduced 8% for 2026–2029, with an H2 recovery assumed.

AVTECH has secured its first new customer in a long time and its first-ever Boeing customer. However, it is a relatively small airline and deal in question.

AVTECH has signed Compass Cargo Airlines for its Aventus Flight Optimisation services covering its Boeing 747F fleet, marking the first customer deployment on the Boeing 747 platform. The contract value is immaterial at SEK0.1m–0.2m. According to Planespotters data, Compass Cargo operates two Boeing 747s and three Boeing 737s, suggesting modest upsell potential through fleet expansion and broader adoption of AVTECH’s product portfolio. Following a year-long hiatus in new sales, Redeye views this as a positive indication that the refreshed sales organisation is beginning to secure contracts.