Absolutely. Finally got the business in reasonable shape, and with this shock, demand for products is likely to be strong. HK apparently also supplies more to restaurants, etc., but Atria probably doesn’t have such a large part of the production chain?

Of course, the valuation multiples will now be wiped out, but I will follow the situation with interest and will add it back to my portfolio when the time is right.

1 Like

Maybe domestic demand won’t plummet as much, as people need food even during this epidemic? At least for now, ground meat seems to be in demand, as store shelves are empty. Unless stores and shopping centers start to close down.

How do you see the situation in Sweden, Estonia, Denmark, and Russia? Do they have their own production, or how much is exported from Finland?

1 Like

https://www.aamulehti.fi/a/656100df-d700-4b9d-bc32-43e0abbabc9e?c=1522737894164

Food companies have not suffered from the coronavirus.

Atria, a food processor, is working at a normal pace. In recent days, the food company has even increased the production of those products that have been most in demand.

“We have seen high sales in ready-made meals, which is due to the increase in remote work and thus the shift of lunch to homes,” says Merja Leino, Atria’s Director of Sustainability.

At the moment, there is no indication that the production situation will change. The most important thing now is to protect staff from infections and thus keep the factories running, Leino continues.

Another major food processor, HKScan, is also operating normally in terms of production and deliveries.

Both companies have already implemented a travel ban and quarantine period for employees returning from holidays abroad, and office workers have, where possible, switched to remote work.

3 Likes

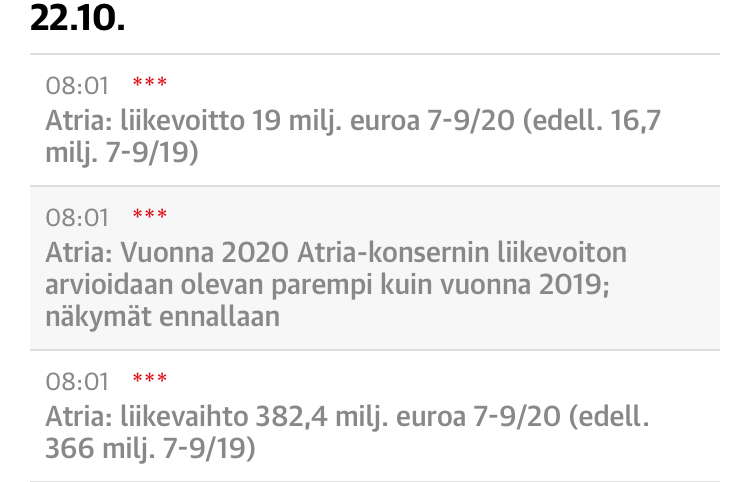

Atria published its Q1 results today.

-Revenue and operating profit grew from last year.

-The full-year operating profit is forecast to be better than last year.

-Pork exports to China have been strong in March and are expected to grow throughout the rest of the year.

-The only clear weakening was the decrease in sales of large kitchen products.

This seems like a pretty good COVID-resistant safe haven.

1 Like

Yes, I’m also quite positive about the report.

If Sweden and Russia become profitable, then it’s fantastic.

Profitability has been eroded by the sudden increase in demand for household products, which has led to overtime and production adjustments – these should even out in the longer term, and for example, allocation decisions to shift the production of institutional kitchen products to household products are probably a matter of organization.

The development of raw material prices is, of course, of interest in this market situation.

Today, Atria is on sale, and I think it’s already my third largest position in my portfolio. I think I’ll have to add a small amount more with dividend money ![]() This stock has allowed me to make a lot of money over the past few years, which at first glance seems quite absurd, considering it’s a meat company

This stock has allowed me to make a lot of money over the past few years, which at first glance seems quite absurd, considering it’s a meat company ![]()

It’s worth considering the Easter period and the fact that JG (not JVG) has often expressed concern that higher-margin products are left in stock. “Steaks are not made at home.”

For Q1, there were no seasons, so everything was, of course, good ground beef hoarding. Many times, it used to be a loss-making quarter.

Sweden grew, but when last year’s one-off gains are adjusted from the comparison period, this year’s Q1 result for Sweden is still terribly bad. This just isn’t turning around.

Boom Boom good friends,

Is anyone else in the meat grinder? The effects of corona are probably not very catastrophic - in the initial stage, there were problems with adapting production, and supply could be strengthened at the expense of margin - overtime had to be done.

Would the situation be different now? However, renewing the product portfolio should be relatively quick, and the volume in lower-margin products could compensate for the decline in volume of more profitable products.

The concern about poor sales of higher-margin products weighed heavily during lockdowns - of course, it may take a while for demand to return to normal. Have the right allocation decisions been made in these cases?

Operational costs will probably be covered by the increased demand for household products, but what does the future look like? The stock price has taken a bit of a setback after the rise of lockdowns - are there any estimates, for example, about the situation in Sweden now in the midst of corona? Will operations outside Finland remain unprofitable? What is the situation with exports to China?

Many questions, many guesses. An interesting case!

1 Like

YT: the end result? ![]()

1 Like

I changed the title that the thread starter put back in the day ![]()

7 Likes

The hosts decided to erect a small annex in Nurmo.

A 155 million euro investment is a rather bold move for a company with a market capitalization of 260 million euros, an operating profit of 30 million euros, and an ROE of 4%. This is probably the healthy growth according to the strategy. But one can lower the bar a bit when shareholder value is created in an abnormal way.

3 Likes

So, to Nurmo…

Now, this is a project of such a scale that we’ll have to see. There will be depreciations for a hell of a long time, or rent payments…

Of course, this world is moving towards white meat, as red meat is unhealthy!!

But is there demand for chicken? Isn’t that dangerous too?

The strategies of the meat companies on our stock exchange are interesting. Even in light of these, I’m willing to lean towards HK – if I have to choose, that is. I followed Atria and the industry for a while, and I really can’t understand this kind of investment in meat. HK’s strategy and time will show whether it will become a proper “food company” that includes more than just meat. It has to be something that creates the aforementioned shareholder value. These two anti-heroes have never succeeded in that.

Atria has a very unfortunate habit of always crashing in some area. Hopefully, it will divest Russia very soon. The timing of that is also completely unbelievably unlucky and shows a complete inability of management. I, on the other hand, see HK having made the right turn in many places – although in my opinion, sharp turns still need to be made. One is the question of meat, or rather, the lack thereof.

Or most likely, these miserable companies will keep playing this dull, follow-the-booze-card (the same business) until the end of time.

1 Like

There’s absolutely nothing to suggest that chicken consumption is decreasing. If there’s demand, it’s best to try and produce as cost-effectively as possible.

From an investment perspective, HK and Atria are not interesting in any way. Kesko and S-Group will continue to pocket the euros from similar productivity improvement projects in the future.

Who will deliver this?

1 Like

EDIT: Found the post I was looking for:

https://twitter.com/zijoittaja/status/1309455153477681153?s=20

1 Like

{“content”:"So, the support came right away, and given my very rough expectations, the result was good. No sign of the so-called file result.

The strategy update, which I also complained about concerning HK’s equivalent, went in the same direction. However, it requires better focus on what it absolutely entails for both.

Even though it now seems that broiler demand is growing, it’s still meat, and I wouldn’t extrapolate anything from meat consumption.

Meat certainly has its place and should have it, but it doesn’t create value or growth. "}

I’m not exactly thrilled about HK/Atria as a company (ownership background), but where’s this dissing of meat coming from?

Did you mean that “artificial meat vs. BYND” and grasshoppers are value creation, or what?

2 Likes

Poor capital return, ties up capital, cyclical from many angles, raw material susceptible to meat prices & feed, poor global synergy benefits.. As I said, some end always leaks, and that is one big reason why owner value has never been created. Quite the opposite. This isn’t even touching on the ownership background or those reasons.

In my opinion, I also didn’t directly write anything about chains etc. Food company is a broad concept and a great step from both of them finally. Objectivity is gold even in bad industries when it comes to investing. Products with higher added margins would be welcome. Both already have these, Atria more than HK.

1 Like