Thanks a lot, now I really understood that in broad terms. A press release just came out stating that the arrangements have been completed. This was a bit of a bigger deal than I first thought.

Not all acquisitions are successful. Assa also made a 2.2b SEK write-off on some Citizen ID business.

Assa Abloy has been increasing shareholder value for years through numerous relatively small acquisitions. The locking business, based on local “monopolies,” has grown profitably. This has been my largest single investment, and I have been a satisfied shareholder. The strong management has also enjoyed my confidence.

Now, the size (and risk) of acquisitions has increased. Furthermore, I feel the focus is less sharp than it was previously. I suspect that managing numerous acquired businesses may become difficult, potentially leading to surprises for shareholders. I am no longer as confident in the company’s success as I was over the past 20 years. Consequently, I have reduced my holding over the last two years. It remains to be seen what the future holds.

They have indeed managed to grow for decades with this strategy. I agree that the scale is now larger than usual and more complex. I still trust that the solid execution will continue; very good management and smart owners. Latour and Melker Schörling are the kind of owners you can trust. I am a very long-term owner and added a small slice over the past year.

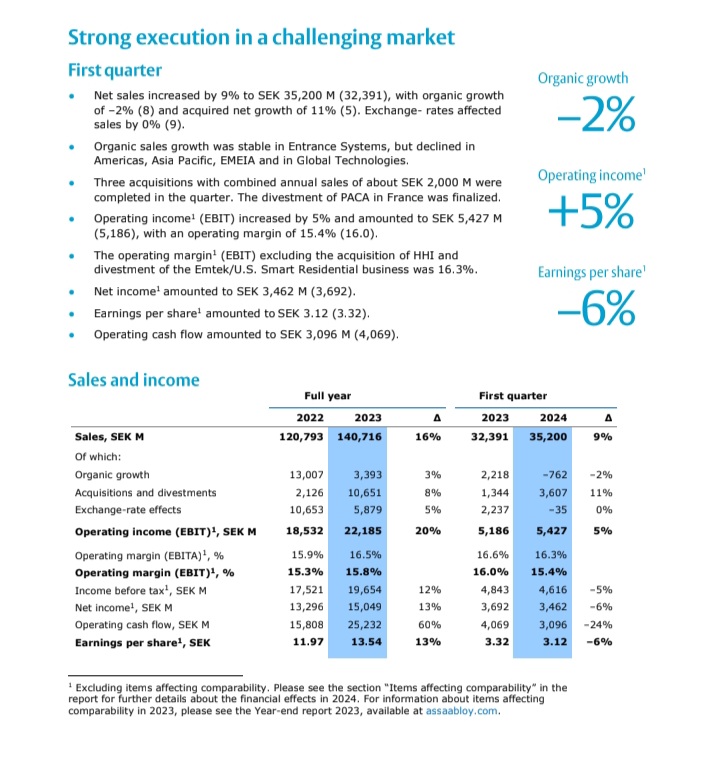

Net sales increased by 17% to SEK 34,474 M (29,466), with organic growth of 3% (13) and acquired net growth of 6% (0). Exchange-rates affected sales by 8% (12).

Very strong organic sales growth in Global Technologies, good growth in the Americas, stable in Entrance Systems, while organic sales declined in Asia Pacific and EMEIA.

The acquisition of Spectrum Brands’ Hardware and Home improvement division (HHI) was completed in June.

The divestment of Emtek and Smart Residential business in the U.S. and Canada to Fortune Brands was completed in June. The divestment gain, including exit costs, totaled SEK 3,661 M for the quarter.

Impairment of goodwill and other intangible assets in Global Technologies led to one-off costs of SEK 2,268 M before taxes.

Operating income1 (EBIT) increased by 25% and amounted to SEK 5,500 M (4,406), with an operating margin of 16.0% (15.0).

The operating margin1 (EBIT) excluding the acquisition of HHI and divestment of the Emtek/U.S. Smart Residential was 16.7%.

Net income1 amounted to SEK 3,731 M (3,156).

Earnings per share1 amounted to SEK 3.36 (2.84).

Operating cash flow amounted to SEK 6,671 M (3,787).

Don’t know what consensus expected, but it seems to be chugging along nicely…

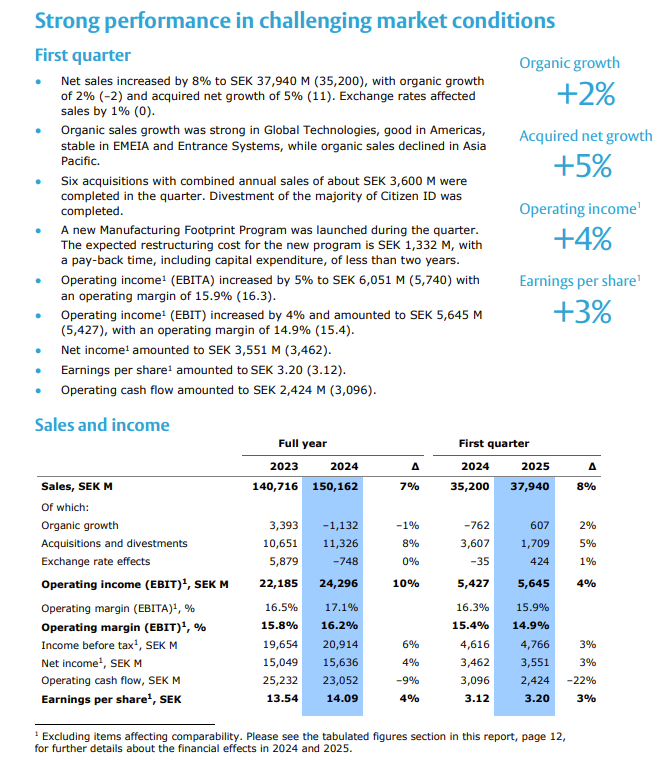

• Sales increased by 16% to MSEK 36,881 (31,820), of which 1% (14) was organic growth and 11% (3) net acquired growth. Exchange rate effects affected sales by 4% (16).

• Good organic sales growth was achieved by Global Technologies and Americas, stable organic sales for Entrance Systems, while organic sales decreased for Asia Pacific and EMEIA.

• Ten acquisitions were signed during the quarter with a total annual turnover of approximately MSEK 2,000.

• The EBITA margin was 16.7% (16.2).

• Operating income1 (EBIT) increased by 16% and amounted to MSEK 5,777 (4,973), with an operating margin of 15.7% (15.6).

• The operating margin1 (EBIT) excluding the acquisition of HHI and the divestment of Emtek/U.S. Smart Residential reached a record high of 17.4%.

• Net income1 amounted to MSEK 3,656 (3,552).

• Earnings per share1 amounted to SEK 3.31 (3.20).

• Operating cash flow reached a record high of MSEK 7,177 (4,520).

Edit. I don’t know what the market expected, but the numbers were apparently quite alright.

-Sales increased by 12% to SEK 36,970 M (32,915), of which 0% (9) was positive organic growth and 11% (5) net acquired growth. Exchange rate effects impacted sales by 1% (14).

-Strong organic sales growth was demonstrated by Americas and good growth for Entrance Systems, while organic sales decreased for Asia Pacific, EMEIA and Global Technologies.

-Six acquisitions were signed with a total annual turnover of approximately SEK 900 M.

-Operating income1 (EBIT) increased by 11% and amounted to SEK 5,722 M (5,152), with an operating margin of 15.5% (15.7).

-The operating margin1 (EBIT) excluding the acquisition of HHI and the divestment of Emtek/U.S. Smart Residential amounted to 16.8%.

-Net income1 amounted to SEK 3,969 M (3,729).

-Earnings per share1 amounted to SEK 3.56 (3.36).

-Operating cash flow reached a record high of SEK 7,315 M (6,588).

-The Board of Directors proposes a dividend for 2023 of SEK 5.40 (4.80) per share, distributed equally over two separate payment dates.

Organic growth really fizzled out in Q4. Q4’22 organic growth was at least 9%. I don’t know what the markets were expecting.

Q1 results out, first time organic growth since Q3 -23. Aftermarket (maintenance, repair) apparently in an important position, when the markets are otherwise lagging. Acquisitions (and sales?) slightly lowered the margin, reportedly temporary

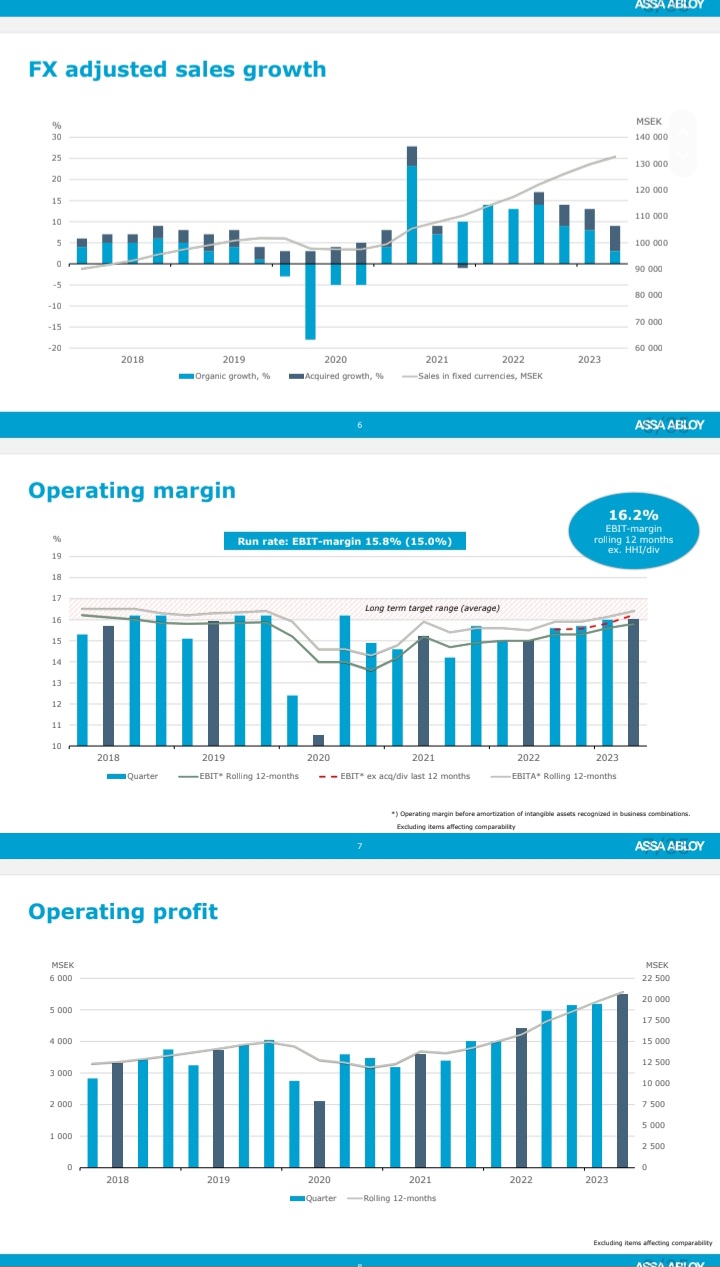

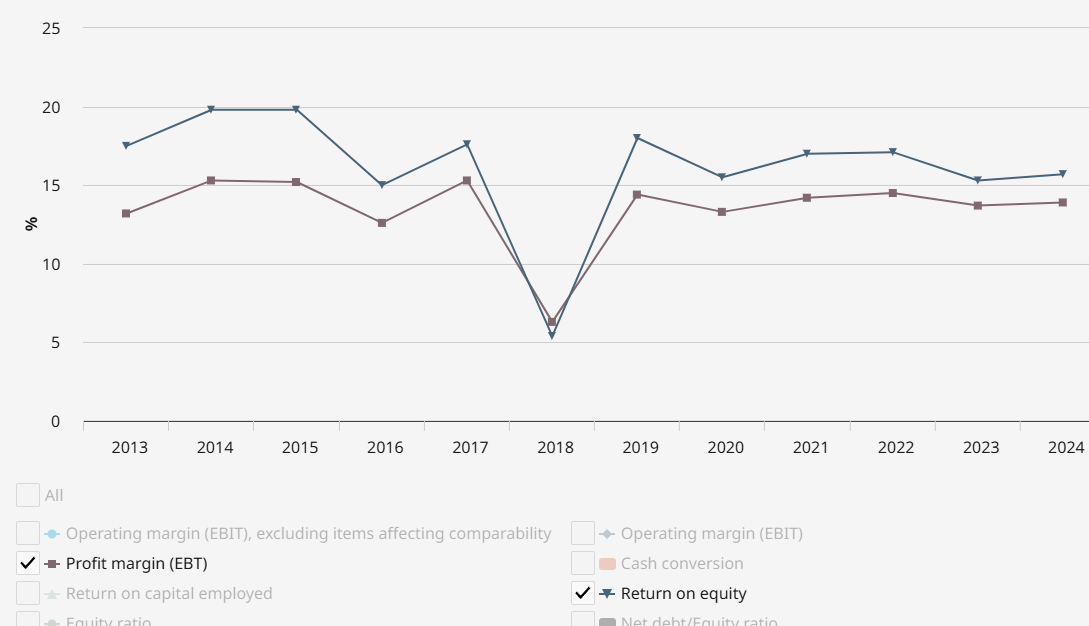

I looked at the long-term figures, and profitability has indeed been at a good level in terms of both revenue and capital. (There’s some one-off dip in 2018; does anyone remember what it was?).

I quickly looked at recent figures (2013-2024), and profitability is at a good level, indebtedness is perhaps slightly elevated, the company has grown slowly, investment in product development is ongoing, and the dividend has been sustainable. Acquisitions are then a risk, depending on how successful they are.

I couldn’t quickly get clarity on the competition, what the role of traditional competitors is, and whether there are new players that could disrupt the situation.

I can’t really say anything smart about the valuation, as it’s not my strength. Recent key figures: P/E 23.5 (total), dividend yield 1.7%, and EV/MCap = 118%.

It seems quite OK at a quick glance; I’ll have to look into this more closely.

Just for fun, I downloaded all of ASSA ABLOY’s financial data from 2013-2024 to do a “reality check” on what the company has been able to achieve in the long run. It gives some guidelines for the realism of the targets; of course, the past is no guarantee of the future, but it does tell something. I also included the company’s targets so you can compare. Realized growth figures for 2013-2024, annualized:

Revenue +9.9% p.a. - target 10%

Earnings +10.5% p.a.

Share price +9.3% p.a.

Dividend +9.9% p.a.

So, a company growing by approx. +10% by all metrics.

Additionally, let’s look at the operating margin, which has averaged 15.7% with a target of 16-17%. The operating margin has been very stable over the years, with little variation.

So, very “down-to-earth” targets relative to the company’s history.

P.S. Credit must be given for sharing such financial data; all key figures and ratios can be nicely downloaded as an Excel spreadsheet. Since the figures are available, there’s no need to be stingy with them.

ASSA ABLOY has acquired Kentix GmbH (“Kentix”), a German designer and manufacturer of monitoring and access control products for datacenters

ASSA ABLOY has acquired Kentix GmbH (“Kentix”), a German designer and manufacturer of monitoring and access control products for datacenters.

“I am very pleased to welcome Kentix to ASSA ABLOY. This acquisition delivers on our strategy to add complementary products and solutions to our core business,” says Nico Delvaux, President and CEO of ASSA ABLOY.

“I am delighted that Kentix will join the EMEIA Division. Their strong expertise in access control products for data centers aligns well to our Digital & Access Solutions segment vision. Kentix will expand our capability in the fast-growing data center segment delivering an integrated, future-proof security solution that complements our portfolio and positions us well in this critical vertical. We welcome the team at Kentix to the ASSA ABLOY family,” says Neil Vann, Executive Vice President of ASSA ABLOY and Head of EMEIA Division.

**Kentix was established in 2008 and has some 40 employees. The main office and factory are located in Idar-Oberstein, Germany. **

Sales for 2024 amounted to about MEUR 8 (approx. MSEK 90) with a good EBIT margin. The acquisition will be accretive to EPS from the start.

ASSA ABLOY has acquired NSP Security (“NSP”) in the UK, a company providing design, manufacturing and installation of access control solutions primarily within the student accommodation segment.

This is news too, and it’s nice if we can get some discussion going here!

The scale of the acquisition is quite small: NSP’s revenue was just over €9m in 2024.

It is in line with the strategy, however; ASSA’s goal is to grow 5% annually through M&A + organic growth.

2025 results the day after tomorrow on Thursday, are any surprises expected?