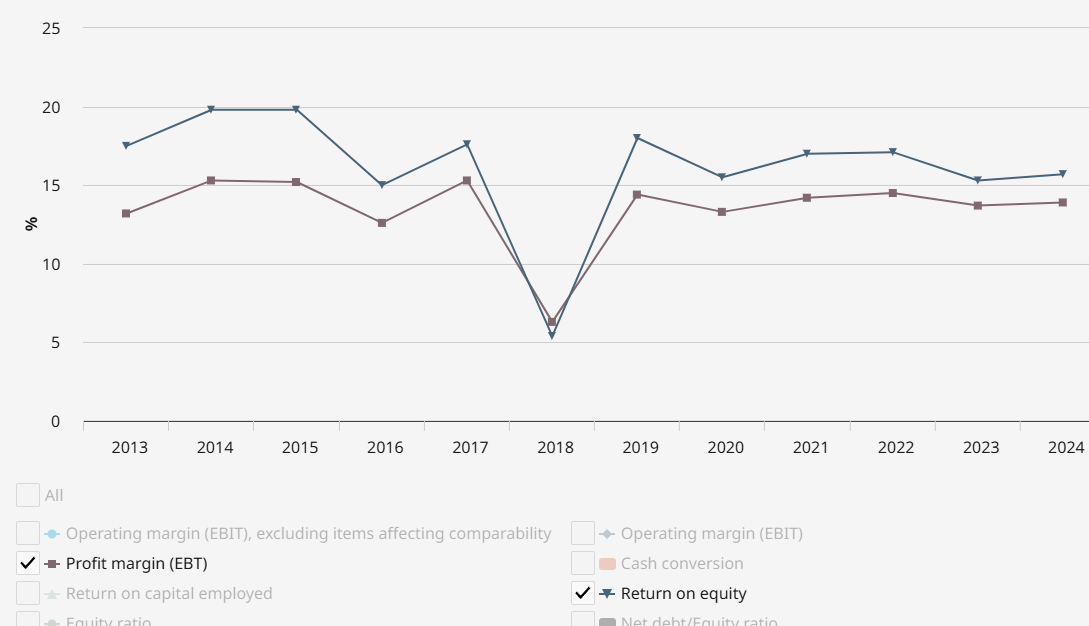

I looked at the long-term figures, and profitability has indeed been at a good level in terms of both revenue and capital. (There’s some one-off dip in 2018; does anyone remember what it was?).

I quickly looked at recent figures (2013-2024), and profitability is at a good level, indebtedness is perhaps slightly elevated, the company has grown slowly, investment in product development is ongoing, and the dividend has been sustainable. Acquisitions are then a risk, depending on how successful they are.

I couldn’t quickly get clarity on the competition, what the role of traditional competitors is, and whether there are new players that could disrupt the situation.

I can’t really say anything smart about the valuation, as it’s not my strength. Recent key figures: P/E 23.5 (total), dividend yield 1.7%, and EV/MCap = 118%.

It seems quite OK at a quick glance; I’ll have to look into this more closely.