Lupailin avata jossain vaiheessa Aspen Aerogelsille ketjua. Arvostuksen viimeaikainen pudotus herätti kiinnostuksen uudestaan, joten tässä olisi kiinnostuneille pakettia avattavaksi:

Yritys

Aspen Aerogels on vuonna 2001 perustettu yhdysvaltalainen yritys, joka erikoistuu aerogeelipohjaisiin eristystuotteisiin. Yrityksen pääkonttori sijaitsee Northboroughissa, Massachusettsissa, ja sen toiminta keskittyy aerogeelien kehitykseen, valmistukseen ja kaupallistamiseen. Aerogeelit ovat erittäin huokoisia ja kevyitä materiaaleja, jotka tarjoavat erinomaisen lämmön- ja palonkestävyyden. Aspen Aerogels tunnetaan erityisesti innovatiivisista, ympäristöystävällisistä ratkaisuistaan, joilla voidaan parantaa energiatehokkuutta monilla eri teollisuudenaloilla.

Tuotteet ja palvelut

Aspen Aerogels tarjoaa erilaisia tuotteita ja palveluja, jotka tukevat energiatehokkuutta, turvallisuutta ja kestävyyttä. Sen keskeisimpiä tuotteita ovat aerogeelipohjaiset eristemateriaalit, kuten Pyrogel® ja Cryogel®, joita käytetään esimerkiksi öljy- ja kaasuteollisuudessa putkistojen ja laitteistojen lämpöeristykseen. Aerogeelit pystyvät eristämään lämpöä erittäin ohuina kerroksina, mikä säästää tilaa ja tarjoaa hyvät palonsuojaominaisuudet.

Yhtiö panostaa myös nopeasti kasvavaan sähköautomarkkinaan. Sen aerogeelipohjaisia ratkaisuja käytetään sähköautojen akkujen lämmönhallintaan, mikä parantaa akkujen turvallisuutta ja kestävyyttä. Näin Aspen Aerogels pystyy vastaamaan autoalan tarpeisiin, sillä sähköautojen valmistajat pyrkivät parantamaan akkuturvallisuutta ja ajomatkaa.

Liiketoimintasegmentit

Aspen Aerogels toimii kolmella pääalueella:

- Energiateollisuus: Yritys tarjoaa teollisuuden putkistoihin, säiliöihin ja prosessilaitteisiin eristemateriaaleja, jotka vähentävät energiankulutusta ja päästöjä.

- Sähköautoala: Sähköajoneuvojen lämpöhallintaratkaisut vastaavat kasvavaan kysyntään, ja yrityksellä on kumppanuuksia useiden merkittävien sähköautovalmistajien kanssa.

- Rakennusala: Aerogeelipohjaisia tuotteita käytetään rakennusten energiatehokkuuden ja paloturvallisuuden parantamiseen, erityisesti silloin, kun tarvitaan ohuita ja kevyitä eristeratkaisuja.

Aerogeelit

Aerogeeli on erittäin kevyt ja huokoinen materiaali, joka koostuu kiinteästä aineesta ja suuresta määrästä ilmaa (yleensä yli 90 % tilavuudesta). Se valmistetaan poistamalla neste geelimäisestä aineesta niin, että jäljelle jää huokoinen kiinteä rakenne, joka säilyttää alkuperäisen muotonsa ja rakenteensa.

Aerogeelin tunnetuin ominaisuus on sen poikkeuksellinen lämmöneristyskyky, minkä vuoksi sitä käytetään monissa lämpöä eristävissä sovelluksissa, kuten rakennuksissa, avaruusteknologiassa ja teollisissa eristeissä. Aerogeeli on myös erittäin kevyt, ja sitä kutsutaan joskus “kiinteäksi savuksi” tai “jäätyneeksi savuksi” sen läpikuultavan ja hauraan ulkonäön vuoksi.

2 grammaa aerogeeliä kannattelemassa 2,5 kg:n painoista tiiltä. (Wikipedian kuva)

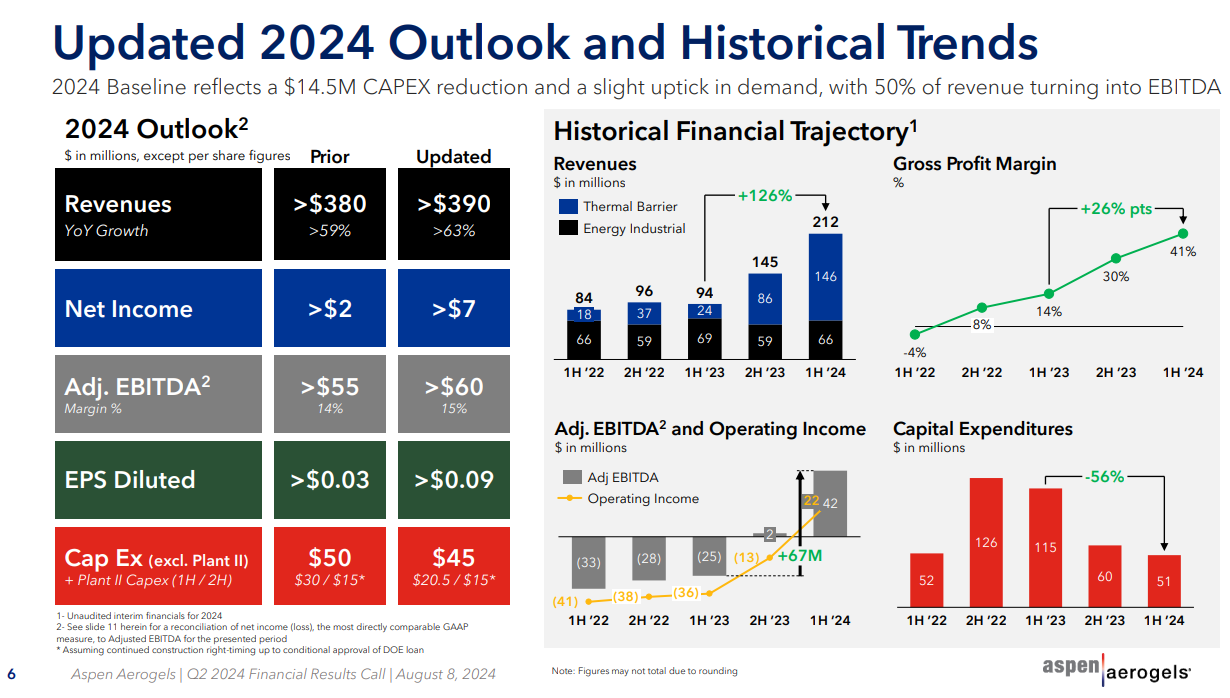

2024 / Q2 raportti ja esitysmateriaalit

Eli toiminta kasvaa ripeästi, kannattavuus kääntymässä plussalle ja kassaa poltettu vielä toistaiseksi

Lähde: Tradingview

Kassanhallintaan yritys keräsi juuri pääomia 85M€ bruttona, 20$ per osake hintaan.

Osakkeen valuaatio on heitellyt todella paljon, nyt menty alamäkeä. Tukitasoa pitäisi löytyä näiltä paikkeilta, mutta hyvin volatiili tapaus kyseessä. Kuva tammi-lokakuu 2024 ajalta.

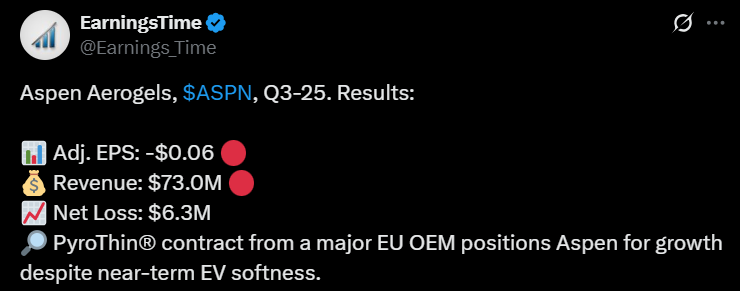

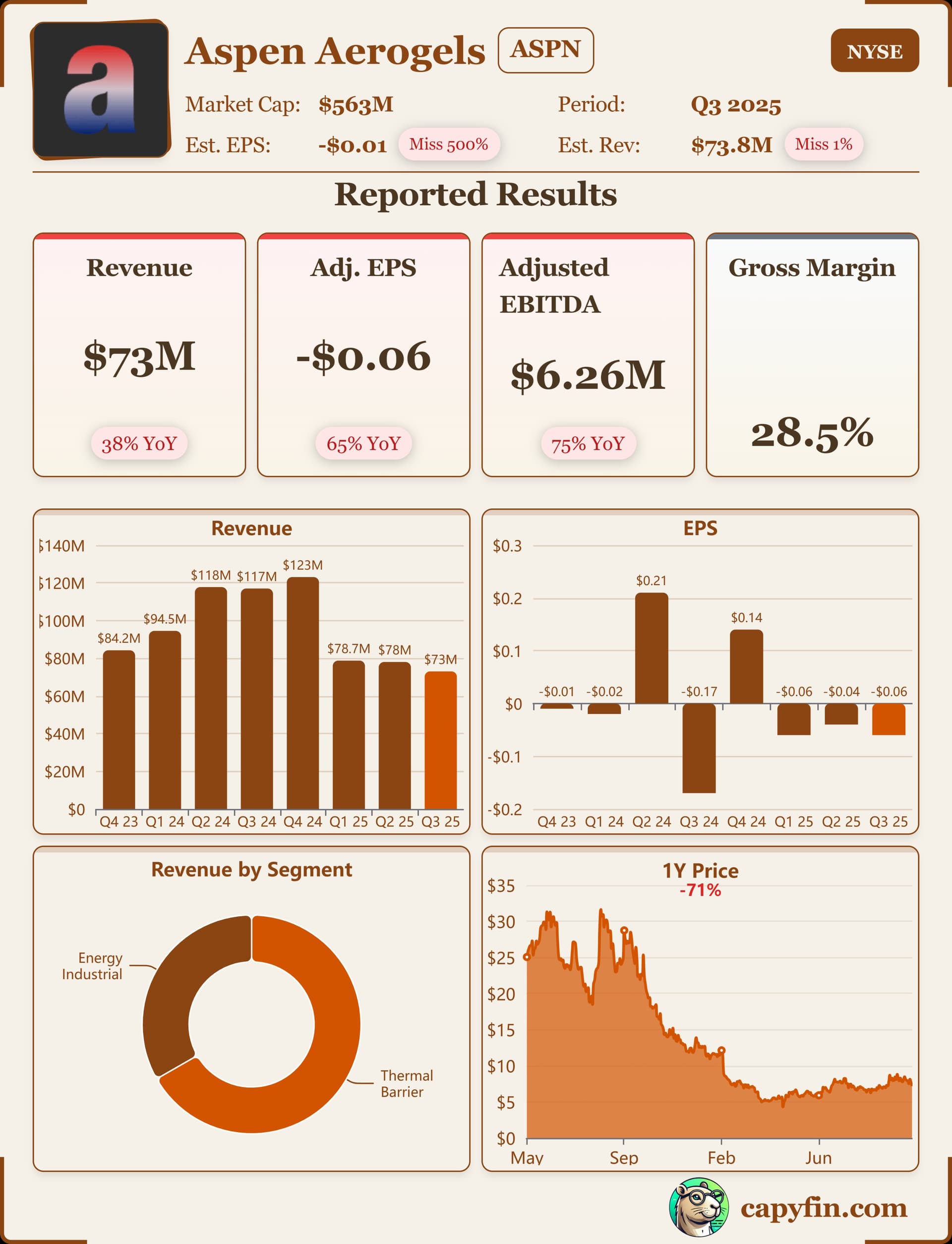

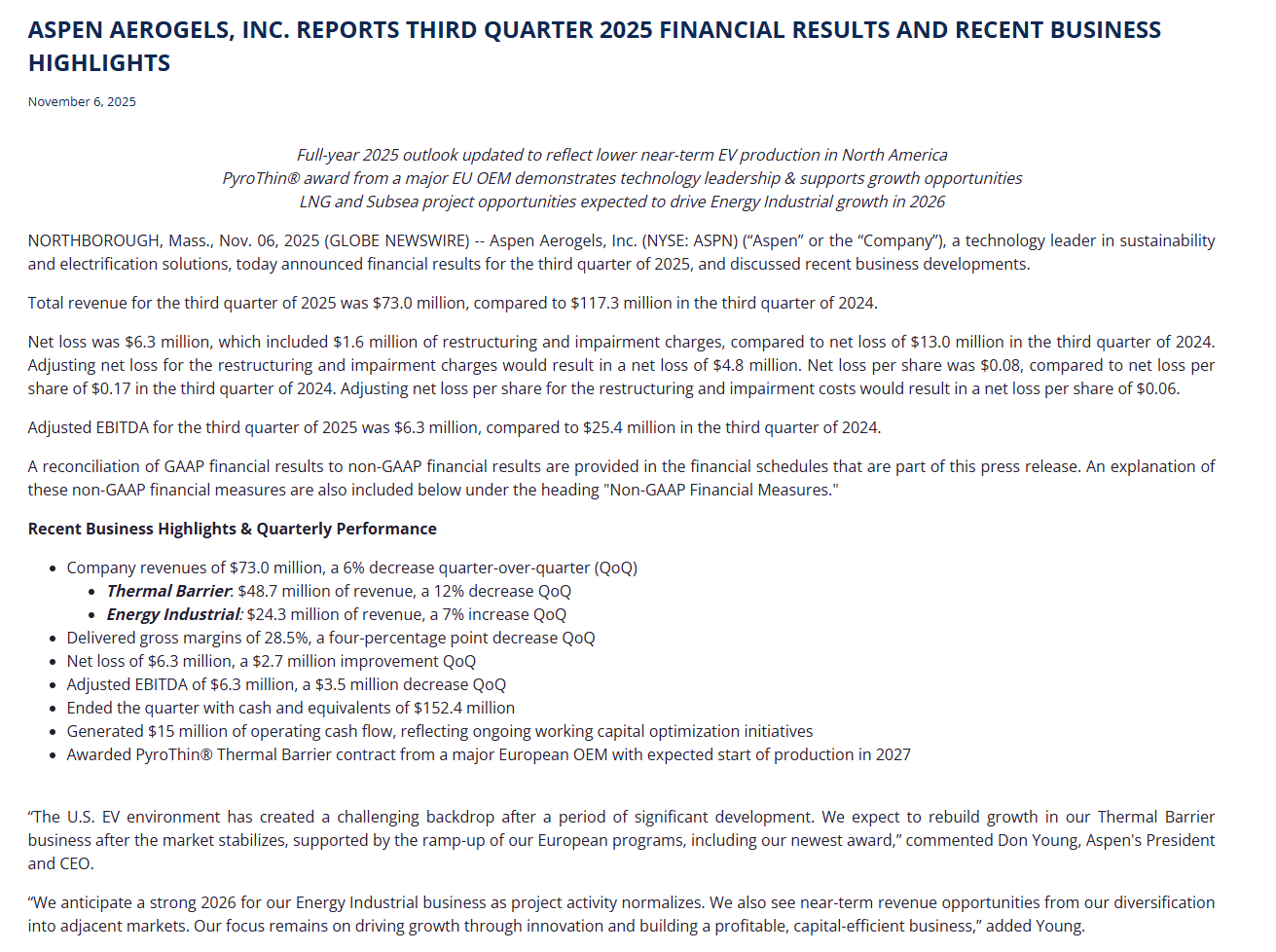

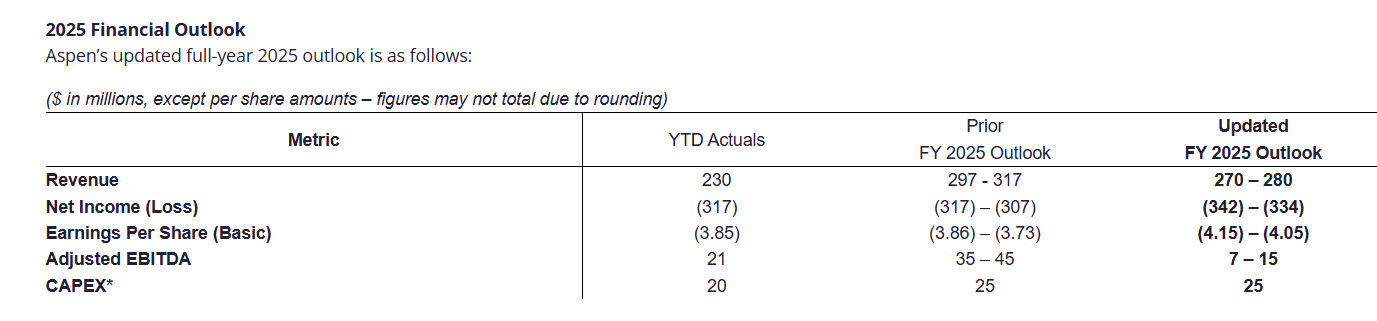

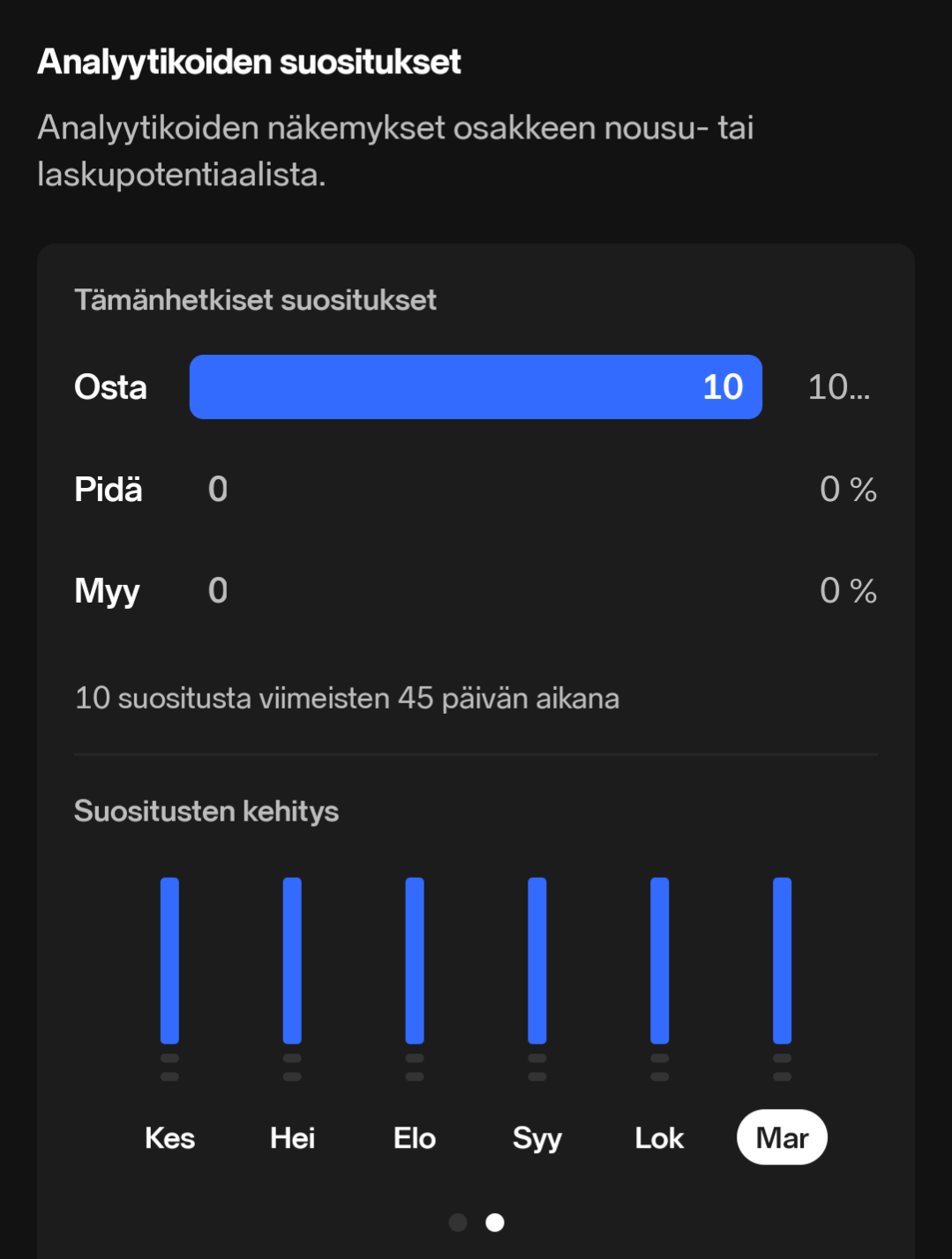

Q3 raportti 6.11. joka määrittää suuntaa vahvasti. Analyytikoilla on isosti luottamusta, nämä Nordnetin näkymästä 1.11.2024

Kilpailijoitakin toki löytyy, ChatGPT nosti muutaman esille

Aspen Aerogelsin suurimpia kilpailijoita aerogeelipohjaisten eristeiden markkinoilla ovat:

- Cabot Corporation – Valmistaa aerogeelipohjaisia eristeitä erityisesti rakennus- ja energiateollisuudelle.

- Armacell – Tunnetaan eristys- ja vaimennusratkaisuistaan teollisuudelle ja rakennusalalle; tarjoaa aerogeelipohjaisia ratkaisuja muun muassa putkistojen eristämiseen.

- BASF SE – Tarjoaa SLENTITE®- ja SLENTEX®-aerogeelituotteita, jotka on suunnattu rakennus- ja infrastruktuurimarkkinoille energiatehokkuuden parantamiseen.

- Aerogel Technologies – Keskittyy aerogeelien kehitykseen ja räätälöityihin ratkaisuihin erilaisiin teollisiin sovelluksiin, mukaan lukien ilmailu ja puolustus.

- Nano Tech Co., Ltd. – Valmistaa aerogeelipohjaisia eristemateriaaleja muun muassa elektroniikan ja rakennusteollisuuden tarpeisiin.