Hei. Onko Aspocompin tiiviitä seuraajia täällä? Mielipiteitä yhtiöstä, hyötyykö 5g-markkinasta? Vaikuttais ainakin kurssikehitys olevan hurjaa.

4 tykkäystä

Tilauskanta on kyllä mielenkiintoisissa lukemissa(4,9miljoonaa). Seuraavan kvartaalin liikevaihto on ollut 2017 jälkeen n. 2,5 kertainen tilauskantaan nähden, mikä antaisi reilu 12 miljoonaa liikevaihdoksi. Aikaisemmin tältä vuodelta on koossa 23 miljoonaa. Yhteensä noi olisi 20% yli viime vuoden, kun ohjeistus on vain noin +10%.

"

TULEVAISUUDEN NÄKYMÄT

Yhtiö säilyttää koko vuoden ohjeistuksen ennallaan. Vuonna 2019 liikevaihdon arvioidaan kasvavan noin 10 prosenttia vuodesta 2018 ja liiketuloksen paranevan vuodesta 2018. Vuoden 2018 liikevaihto oli 29,1 miljoonaa euroa ja liiketulos oli 2,9 miljoonaa euroa.

"

Oli kyllä hidas markkinareaktio negariin. Olisi ehtinyt myymään laitaan moneen kertaan positiot.

Joo, ehdin myymään omat 11 ja 35 sekuntia negarin jälkeen. Mielenkiintoista nähdä millaiseksi tulos muodostuu. Viime vuoden eps oli kuitenkin 0.59, 0.40eps olisi hyvää tasoa sekin nykykurssilla.

Joo katsoinkin, että Nordnet sielä myi nopeasti.

Tervehdys! Aspocompista ei ole paljoa keskustelua vielä, mutta jotain kuitenkin - ajattelin siis lyhyesti kommentoida tulosvaroitusta tännekin ja kantaa oman korkeni kekoon!

Vaikka negatiivinen tulosvaroitus oli toki hyvin mahdollinen heikon alkuvuoden jälkeen, oli tuo ajoitus ja voimakkuus (“jää merkittävästi”) selkeä negatiivinen yllätys. Tuoretta raporttia aiemmin kirjoitin “Heikossa skenaariossa Aspocomp voi joutua antamaan myös negatiivisen tulosvaroituksen loppuvuonna, jolloin vauhtia haettaisiin varmaan alempaa”, mutta Q2:n piti olla vielä vahva kevään kommenttien perusteella autoteollisuuden ulkopuolella. Se arvio meni selkeästi pieleen. Nyt varoituksen ajoitus on sellainen, että Q2-luvut on oletettavasti sisällä ja Q3:lle on ainakin kohtuullinen näkyvyys. Kun tähän yhdistetään yhtiön kommentti kysynnän yleisestä heikentymisestä kesäkauden alussa, taitavat sekä Q2 että Q3 olla vaikeita. Ja alkuvuosihan oli jo heikko, eli vuosi 2020 taitaa olla tuloksellisesti “välivuosi”. Valitettavasti näkyvyyttä ensi vuoteen ei ole, joten tuloksen elpymisnopeutta on käytännössä mahdotonta arvioida ilman lisätietoja.

Osakkeen arvostuksen suhteen ristiriitainen tilanne. Vuoden 2020 kertoimilla osake on suhteellisen kallis, vaikka oma ennusteeni olisikin liian pessimistinen, ja todella kallis jos se toteutuu. Mutta kun katsotaan 12 kk päähän niin 2020 luvuilla ei tietenkään juuri merkitystä ole, jos tulos elpyisi jälleen viime vuosien tasolle ensi vuonna. Aspocompin kohdalla on kuitenkin vaikea katsoa vahvasti eteenpäin, kun 1) näkyvyys on kroonisesti heikko eli tulosta on vaikea ennustaa ja 2) tulostrendi on kääntynyt nyt negatiiviseksi, mikä ei johdu ainakaan yksistäään koronapandemiasta (myös H2’19-tuloskasvu oli negatiivista). Kun huomioidaan vielä osakkeen korkea riskiprofiili, nähtävissä pitäisi olla selkeä nousuvara, jotta suositus kääntyisi positiiviselle puolelle. Nyt potentiaali, mitä varmasti on, on aikalailla sumun peitossa.

Mielenkiintoinen yhtiö kuitenkin on ja jos katsotaan oikeasti isoa kuvaa, niin onhan tuo noin viiden vuoden nousu sekä tuloksessa että osakekurssissa ollut huikea. Lisäksi yhtiön kokoluokassa suuri investointiohjelma loppusuoralla, joten potentiaalia on myös eteenpäin. Katsotaan pääseekö takaisin tuloskasvun tielle, ja millä kulmakertoimella. Q2’20-raportin jälkeen ollaan jo viisaampia, kun tuon tulosvaroituksen vähäisien tietojen ympärille saadaan vähän lihaa.

Ohessa vielä linkki tuoreen päivityksen aamariversioon: Aspocomp: Kysyntä on ilmeisesti sakannut pahasti | Inderes: Osakeanalyysit, mallisalkku, osakevertailu & aamukatsaus (ei tarvitse Premiumia, raporttikin on toki ulkona).

Jäädään seuraamaan, hyviä sijoituksia!

PS. Markkina on tosiaan näissä pienissä todella tehoton, eli nopealla reagoinnilla voi tehdä paljon hyvää.

8 tykkäystä

Aspocomp tänään 5% nousussa, Aspocompilla on ainakin ennen ollut paljon yhteistyötä Nokian kanssa, jonka hyvä vire näkyy varmasti Aspocompissakin. Vai onko tämä muuttunut viime vuosina?

3 tykkäystä

Virallisesti Aspocomp ei tätä kerro, mutta kyllä Nokia on viime vuosina ollut ja on käsitykseni mukaan edelleen yksi Aspocompin suurimmista asiakkaista. Osuus on kuitenkin laskenut merkittävästi, jos katsotaan vähänkin pidempää aikasarjaa - ja se on hyvä juttu, ettei olla ihan niin sidoksissa yksittäiseen asiakkaaseen.

Toisaalta en usko, että Nokia olisi viime aikaisen nousun taustalla. Nousuhan käynnistyi tästä tiedotteesta, minkä jälkeen liikettä Aspocompin osakkeessa on jälleen ollut enemmän. Tuntuu, että välillä sijoittajat innostuu, ja välillä kiinnostus taas laantuu ![]()

3 tykkäystä

Outoa, että yhtiö ennustaa jo puolessa välin vuotta tuloksen jäävän merkittävästi edellisvuodesta. Jos näkyvyys on heikko tulevaisuuteen, niin eikö parhaimmassa tapauksessa jouduta nostamaan ohjeistusta, vai nähdäänkö että mikään ei voi enää H2 aikana parantaa tilannetta. Verrokeilla näkymät ja tulokset ovat olleet paljon parempia, mikä nyt nostanee myös Aspocomppia…Turhaanko?

Onhan tuossa alkuvuonna 2020 tullut aika hurjasti kurottavaa. H1’20 liikevoitto taisi olla -0,2 MEUR, kun H1’19 tässä vaiheessa oli kasassa mukavat 2,3 MEUR. Poikkeama siis noin 2,5 MEUR, mikä on todella iso luku pienelle Aspocompille.

Loppuvuonna voidaan hyvin parantaa vertailukaudesta, mutta kaikkien aikojen paraskaan puolivuotistulos ei riittäisi kuromaan eroa umpeen. Eikä nyt taida markkinatilanne olla tätä ajatellen suotuisa. Tätä vuotta tuskin pystyy tuloksellisesti pelastamaan, mutta ainahan on ensi vuosi.

2 tykkäystä

Mikähän kramppi iski kurssiin perjantaina viimeisellä tunnilla? Jäin vielä ihmettelemään q3 raportin koottuja selityksiä autoteollisuussegmentin kysynnän laskusta, vaikkakin autovalmistajat ovat kauttaaltaan raportoineet euroopassa konsensuksen ylittäviä lukuja sekä erityisesti syyskuussa parantunutta kysyntää.

Viimemetreillä yksi isompi osto, joka sitten nosti epälikvidin osakkeen kurssia voimakkaasti. En ainakaan itse ole huomannut mitään uutisia tai muuta vastaavaa, mikä voisi olla kurssia nostattanut.

Yleisesti piirilevyjen kysyntä tulee oletettavasti viiveellä, varsinkin kun varastotasot olivat edelleen korkealla. Mutta Aspocomp ei pienenä toimijana ole toki kiinni tuossa koko markkinassa, vaan tietyissä asiakkuuksissa. Toisaalta niin kauan kun aasialaisilla jäteillä on ylimääräistä kapasiteettia ja ne pystyvät reagoimaan myös “pienempiin tarpeisiin”, ostot voivat suuntautua sinne, eikä Aspocompille. Tälläkin on varmaan jonkinlainen vaikutus, tai oli ainakin Q3:lla.

2 tykkäystä

Hiljaista on tällä palstalla…Juhan päivitys:

Nostamme Aspocompin tavoitehinnan 4,2 euroon (aik. 3,8 €) ja suosituksemme lisää-tasolle (aik. vähennä). Vuosi 2020 oli yhtiölle todella vaikea ja Q4-tulos voi tuoda vielä uuden pettymyksen, mutta uskomme tuloskunnon elpyvän vuonna 2021. Jos odotettu tuloskäänne toteutuu ja yhtiö pääsee takaisin kannattavaan kasvuun, osakkeen nykyinen arvostustaso on matala (2021e P/E 10,5x). Näkyvyys on Aspocompin kohdalla kroonisesti heikko, mutta mielestämme hieman pidemmälle katsottaessa osakkeen riski/tuotto-suhde on kohtuullisen hyvä.

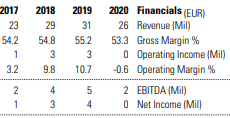

Vuosi 2020 oli surkea, muttei pelkästään paha

Koronapandemia sekoitti koko piirilevymarkkinan vuonna 2020, ja vuodesta muodostui Aspocompille tuloksellisesti surkea. Vaikka Q4-tulos on arviomme mukaan kohtuullinen, ennustamme vuoden 2020 liikevoiton jäävän noin 0,4 MEUR:n tasolle (2019: 3,4 MEUR). Q1-Q3’20 liiketulos jäi tappiolle ja vuosi sisälsi myös ruman negatiivisen tulosvaroituksen. Vaikka tuloksellisesti vuosi oli surkea, lukujen takana tapahtui positiivista kehitystä tulevaisuutta ajatellen. Merkittävä osa heikkoudesta voidaan laittaa tietoliikennesektorin (5G-tuotekehityssykli) ja koronasta sekä toimialan murroksesta kärsineen autoteollisuuden piikkiin, ja yhtiön panostukset puolijohdeteollisuuteen ovat jo tuottaneet tulosta (liikevaihto noussut noin 80 %). Vuoteen 2021 yhtiö lähteekin tasapainoisemmalla asiakaskokonaisuudella, eikä pelkästään esimerkiksi tietoliikennesektorin varassa.

Vuosi 2021 tuonee mukanaan käänteen parempaan

Aspocompin kohdalla näkyvyys on aina sumuinen, joten varmoja ovat vain yllätykset. Silti markkinanäkymä vaikuttaa suhteellisen lupaavalta vuoteen 2021 lähdettäessä, sillä yleisesti tuotekehitys on lähtenyt käyntiin ja teknologinen kehitys vaikuttaa saaneen koronapandemiasta lisävauhtia. Yhtiölle tärkeiden tietoliikenneverkkojen ja sitä kautta pikatoimituksien kysyntä voi piristyä nopeasti, kun 5G-kehitys etenee ja massatoimittajien ylikapasiteettitilanne oikenee yleisen kysynnän piristyessä. Tietoliikennesektorin pikatoimitukset olivat vuonna 2020 paikoin jopa historiallisen heikolla tasolla, joten parantamisen varaa on. Puolijohteissa ja turvallisuuspuolella näkymä on jo aiemmin ollut vahva. Odotamme markkinatilanteen normalisoituvan tänä vuonna ja Aspocompin liikevaihdon elpyvän lähelle vuoden 2019 tasoa, kun Tietoliikenneverkkojen kysyntä elpyy ja Puolijohde- ja Turvallisuus-, puolustus- ja ilmailusegmenttien vahva kehitys jatkuu. Samalla tuloskunnon pitäisi elpyä voimakkaasti, vaikka ennustamme 2021 liikevoiton (2,8 MEUR) jäävän selvästi 2019 tasosta (3,4 MEUR) investointien nostaessa poistotasoja. Emme ole tehneet muutoksia ennusteisiimme, mutta luottamuksemme niihin on parantunut hieman.

Odotusarvo on positiivinen, vaikka tuloskäänne on jo hinnassa

Arviomme mukaan vuoden 2020 heikko tulos on poikkeus eikä sääntö, ja koronakuopan yli katsottaessa yhtiön arvostus on kohtuullinen (2021e oik. P/E 10,5x EV/EBITDA alle 6x). Lievästä noususta huolimatta Aspocompin osake on nyt 10-20 % aliarvostettu suhteessa verrokkiryhmään (sisältäen Scanfilin ja Incapin). Osittain tämä on perusteltua, koska Aspocompille vuosi 2020 oli paljon verrokkeja vaikeampi eikä tuloskunnon elpymisestä ole vielä konkreettisia merkkejä. Silti hieman pidemmälle katsottaessa näemme Aspocompilla kaikki edellytykset palata kannattavaan kasvuun yhtiön investointiohjelman edetessä ja heijastuessa tuloksiin. Kehuttava osakkeen riski/tuotto-suhde ei mielestämme ole, mutta vuoden 2021 näkymän selkeytyessä osake voi olla jo korkeammalla tasolla. Olemmekin valmiita odottamaan vuoden 2020 tilinpäätöstä varovaisella lisää-suosituksella.

3 tykkäystä

No olipa huonoa tekemistä viime vuosi…

1 tykkäys

Kaippa tässä pientä valonpilkahdusta on nähtävissä…

Aspocomp estimates that its net sales will increase and its operating result for 2021 will improve from 2020. In 2020, net sales amounted to EUR 25.6 million and the operating result to EUR -0.1 million.

2 tykkäystä

Mitä mieltä porukka, että sataako tämä yleinen komponentti pula Aspocompin laariin ja mahdollisesti isostikin heidän mittasuhteilla ![]()

4 tykkäystä

Minä päädyin siihen, että jos nyt ei ole hyvät ajat edessä niin koska sitten?

Juhan 11.3 yhtiöpäivityksestä:

Ylikapasiteettitilanteessa suuret massavalmistajat pystyvät poikkeuksellisesti tarjoamaan lyhyitä toimitusaikoja, mikä syö Aspocompin kilpailuedun korkean katteen pikatoimituksista.

Sirupula löi silmille vasta Q1 loppupuolella, eikä siten minusta tuossa tuoreimmassa analyysissä näkynyt. Vai onko @Juha_Kinnunen mitä mieltä sirupulan vaikutuksista?

Kaikki lähteet Yleä myöten tosiaan huutavat nyt alikapasiteetista ja sen ennustetaan jatkuvan ensi vuoden puolellekin, mm. NVIDIA ja Qualcomm juuri osareissaan. Eihän se tietysti välttämättä ole lineaarisesti päinvastoin, että nyt Aspocompilla rokki soi, mutta pitäisi sen ehkä olla (IMO). Jos talous vetää yleisesti, niin silloin niitä pikatoimitustarpeita tulee muutenkin eteen ja sirupulan pitäisi vielä buustata.

Toisaalta ei se sirupula mikään ideaalitilanne ole, jos tilane on niin paha että asiakkaat lyö tehtaita kokonaan säppiin kun tavarat on liian isosti finito.

Ja voihan se pula koskettaa Aspocomppia itsekin, vaikkakin käsitykseni on että sirujen “raaka-aineet” yms. ei ole nyt se ongelma. Firma itsekin kirjaili sivuillensa 25.3. tällaista:

How Aspocomp can help

We have an extensive material stock at our Oulu site and supply network with our European partners. It may be the case for European sourcing even if you are used to Asian supply chain for your products. We have been delivering solutions to PCB designs that are not typicaally produced in a QTA factory under normal circumstances. Get in touch with us and we will help you.

https://aspocomp.com/2021/03/25/lead-times-and-logistics/

Tästä nyt on helppo ylituoton metsästäjän bulleroida tulevaks vuodeks kaksinumeroisia tuottoprosentteja sijoitukselle jos sitä kysyntää on todella pikatoimituksille ollut ja/tai on tulossa loppuvuoden aikana.

Tuota Morningstarin tiivistelmää kun tulkitsee niin, että 2020 oli vain ymmärrettävä kuoppa ja tänä vuonna paukautetaan se historiallinen 2-4 megaeuroa nettoa niin kyllä P/E 15 taas jossain kohtaa sallitaan.

Inderes on muuten samoilla linjoilla tuon tulostason kanssa:

Eteenpäin katsottaessa yhtiön pitäisi mielestämme epäonnistua selvästi, ellei se pystyisi ylittämään vuoden 2019 tulosta seuraavan kolmen vuoden aikana

About tällä kurssitasolla on kuitenkin myös mörnitty nyt negareiden yli, joten en ihan odota mitään mahtirommia vaikka Q1 ei mahtava olisikaan. Enkä mitään isoa määrää lappuja tästä viitsi ottaa kun ei tästä pitemmän aikavälin näkymästä saa mitään tolkkua maallikkona. Epäilen myös kroonisesti ja vahvasti, että en ole sittenkään markkinaa nokkelampi noissa kysyntänäkymätulkinnoissani, vaan mörnimiselle on perusteensa.

Mutta pitäähän sitä yrittää ja katson siis silti mieluusti osarin tai toisenkin yli, että lähteekö homma rullaamaan kohtuudella “skin in the game”.

5 tykkäystä

Pahoittelut @naata, että tähän vastaaminen on viipynyt.

Eri asteista komponenttipulaahan on ollut toimialalla jo pitkään. Aspocomp tietysti Eurooppalaisena toimijana (Oulun tehtaan osalta) voi olla hieman eri tilanteessa, mutta en tuon yhtiön (potentiaalisille) asiakkaille suunnatun viestin perusteella tekisi suurempia johtopäätöksiä. Onhan Aspocomp kuitenkin myös nostanut komponenttipulan lähiajan riskeihin. Alla oleva on otettu tilinpäätöksestä:

COVID-19-pandemian vaikutus elektroniikan toimitusketjuun

COVID-19-pandemia ja sen aiheuttamat rajoitukset vaikuttavat merkittävästi koko elektroniikkateollisuuden toimitusketjuihin. COVID-19-pandemia saattaa vaikuttaa myös elektroniikkakokoonpanijoiden tarvitsemien osien ja komponenttien saatavuuteen, mikä heikentäisi kysyntää.

Kokonaisuutta on hankala hahmottaa, koska kuten itsekin tuossa sanoit, negatiivisessa skenaariossa asiakkaat eivät saa tuotteitaan valmiiksi ollenkaan (tai ne viivästyvät). Silloin kyllä myös Aspocompin kysyntä heikkenee. Positiivisessa skenaariossa tilanne ei ole niin paha, Aspocomp pystyy toimittamaan ja saamaan mahdollisesti uusiakin asiakkaita tilanteen kautta. Tässä voisi tukea antaa myös nuo logistiikkahaasteet, jotka voisivat tukea Euroopan houkuttelevuutta (vs. Aasia). Mutta ei piirilevyt kuitenkaan ole massiivisesti tilaa vievä tuote, joten onkohan konttipula sitten kuitenkaan niin iso tekijä. Lisäksi jos komponenteista tulee enemmän pulaa, yleensä tuppaa olemaan niin, että isommat asiakkaat saavat omansa ensin. Tietysti hyvä jos on osannut ennakoida, mutta tilanteen pitkittyessä tilanne voisi kääntyä myös Aspocompia vastaan.

En rehellisesti sanottuna osaa sanoa kokonaisvaikutusta, mutten olisi yhtään varma siitä, että se kääntyisi positiiviseksi ![]() Kohtapa tästä saadaan lisätietoa Q1:n yhteydessä.

Kohtapa tästä saadaan lisätietoa Q1:n yhteydessä.

Voi tietysti olla, että P/E 15x sallittaisiin myös huipputuloksella - hullumpiakin asioita näkee markkinoilla, nykyään melkein päivittäin. Mutta pidetään nyt kuitenkin mielessä, että Aspocompin mediaani P/E on ollut viimeisen 10-vuoden aikana noin 9-10x. Siitä >50 %:n korotus on paljon, ja erityisesti odottamallasi huipputuloksella se olisi melkoinen harppaus. Aspocomp ei ole kuitenkaan pystynyt kestävää kannattavan kasvun träkkiä vielä esittämään, ja 2020 meni kyllä pahasti pieleen. Ymmärrettävistä syistä toki, mutta kun vertaa vaikkapa Incapiin tai Scanfiliin samalta toimialalta, niin erottuuhan tuo Aspocompin tulos ikävästi.

Se on totta, että Aspocompin osake tuntuisi löytäneen jonkinlaisen pohjatason pandemian aikana. Heikoista uutisista huolimatta luottamus elpymiseen on ollut ilmeisesti vahva, ja ainakin 2020 tulos katsottiin aikalailla läpi sormien. Siinä mielessä “mahtirommi” olisi kyllä suuri yllätys itsellekin, jos isompi kuva pysyy kuitenkin ennallaan.

Ja terve itsensä epäileminen on aina hyvästä, sitä harrastan itsekin jatkuvasti ![]()

Tosiaan tuon arvostustason suhteen olisin hieman varovaisempi. Kyllähän tuo nykyinen arvostus sisältää jo suuria tulosparannusodotuksia, koska eihän 2020-tuloksella tietenkään voi näitä tasoja mitenkään perustella - ei mielestäni myöskään 2021 ennusteella. Mutta toki jos tulos elpyisi lähivuosina odotuksien mukaisesti takaisin aiemmille huipputasoille ja vielä tuloskasvunäkymäkin pysyisi hyvänä, niin kyllähän osakkeen tuotto-odotus olisi hyvä. Niin sen mielestäni pitääkin olla, koska pitäähän korkean riskin vastineeksi saadakin merkittävästi tuottopotentiaalia.

Mutta ollaan varmasti viisaampia Q1-tulosjulkistuksen jälkeen. Omien ennusteiden mukaan Q1-tulos on vielä tappiolla, joten siitä nyt ei ihmeitä odotella. Sen jälkeen odotukset alkaakin nousta ja ovatkin jo varsin kovia.

9 tykkäystä

Nyt tuli Aspocompilta isompi sopimus juuri ennen Q1-raporttia ![]()

Huomenna kuullaan varmasti lisää tästäkin.

10 tykkäystä

Vaikeaa on…Ihmellinen ero on suoritumisessa verrokkeihin.