Asmodee pöytäpeli imperiumi - Catanista Pokemonkortteihin

[https://corporate.asmodee.com/]

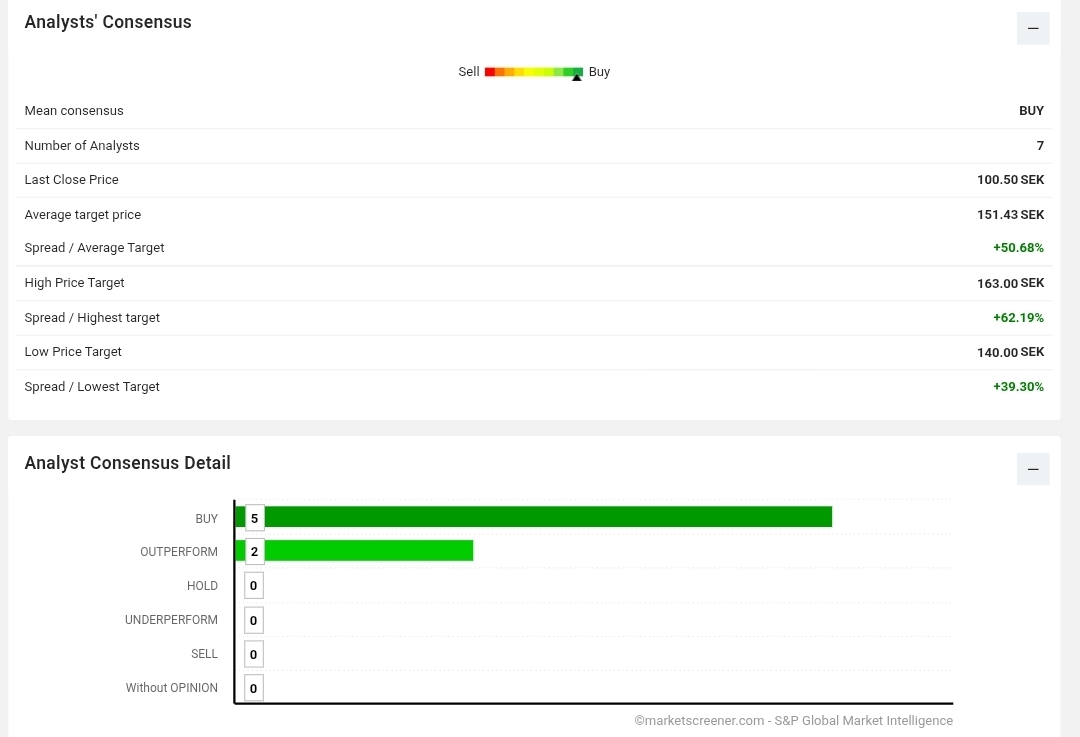

Tukholman Nasdaqin pörssissä tikkerillä ASMDEE-B large cap yhtiöistä.

Pöytä peliyhtiö Asmodee on irronnut emoyhtiöstään Embracerista vihdoin ja viimein.

[Wingefors: De flesta i PE-aktörerna i världen har velat köpa Asmodee | Placera]

Taustaa Embracerin omistuksessa

Ennen Tukholman pörssin listautumista Asmodeella on takanaan 30 vuotinen historia yksityisomistuksissa, joista viimeisin omistaja on ollut Embracer. Embracerin omistuksessa Asmodee on kasvanu ja tuonut kassavirtaa vakaasti. Isomman saneerauksen alla Asmodee oli yksikkö, josta vähennyksiä tai studion sulkemisia ei tehty.

Asmodeen irrottamisen Embracerista suurin päätarkoitusta voi pitää karkeasti siinä, että se vei mennessään Embracerin suuret velat. Tällainen korppikotka tyyli sopisi muuten kuvaan, mutta Asmodeen alkua haluttiin aidosti vahvistaa, kun Embracer sai Easybrain kaupan myötä ylimääräistä kassaa ja antoi irtautumisen yhteydessä rahaa Asmodeelle mukaansa.

Asmodee on noussut yhdeksi maailman suurimmista lautapelien ja korttipelien julkaisijoista ja jakelijoista. Sen pelikirjastoon kuuluu jättihittejä, kuten Catan, Ticket to Ride, Dobble, sekä laaja valikoima kolmansien osapuolien pelejä. Monet eivät kuitenkaan tiedä, että Asmodee on myös yksi suurimmista Pokémon-korttien jakelijoista Euroopassa.

Vaikka yritys listataan Ruotsiin ja pääomistaja on Lars Wingefors, niin Asmodeen juuret löytyy Ranskasta. Tämän lisäksi operatiivinen päämaja tulee olemaan myös siellä.

Johtokunta (2024/2025)

Asmodee toimitusjohtajan Thomas Koeglerin näkemys Asmodeesta on rohkaiseva “Yksityisomistuksessa olleesta Asmodeesta on hoidellu historiassaan isompiakin vipuvarsia (velkalastia) ja kasvanut.”

Lars Wingefors (Chair of the Board)

Kicki Wallje-Lund (Deputy Chair)

Stéphane Carville (former Asmodee CEO)

Marc Nunes (Asmodee founder and former COO)

Jacob Jonmyren (Embracer board member)

Linda Höljö (COO and CFO of Pophouse Entertainment Group)

Velkakirjat ja luottoluokittajien näkemys, sekä kilpailijat

Asmodeen velkakirjat menivät vauhdilla kaupaksi ja nämä on arvioitu Fitchin (B+ positive), Moodyn (B2 positive) ja S&P (B Positive) mukaan highly speculative luokkaan. Näistä avoimena raporttina löytyy Fitchin rating, josta löytyy ongelmat, mitkä erottavat Asmodeen kilpailijoistaan (Mattel, Hasbro). Kilpailijat ovat luottoluokituksensa saaneet investment grade statukselle, joka selittänee niiden arvostustasoja.

[https://www.fitchratings.com/entity/asmodee-group-ab-97674454#ratings]

Raportti sisältää myös hyvän yhtiöesittelyn Fitchin näkökulmasta.

Odotettavissa on Fitchin raporttiin nojaten, että Asmodee suorittaa osan velan maksuistaan ja luottoluokitukset nousevat. Isoin kysymys on, että onnistuuko Asmodee rakentamaan oman portfolionsa tarpeeksi vahvaksi, jolla mahdollinen (pokemon-kortit) riippuvuus vähenisi. Tällöin Asmodee tavoittelisi ainakin Fitchin mukaan kilpailijoiden Investment grade velka luokituksia.

Muuta spekulaatioa…

Alku on hyvä, kun Embracer tosiaan laittaa sitä rahaa mukaan tässä Spin-offissa.

Pöytäpelit ei yleisesti vaihdu niin nopeesti top listoilla, kuin kuumat pc/konsolimarkkinat vaan muutokset on hitaampia. Yksi trendi jota pöytäpeleissä on, että nyt useammissa on mukana yksinpeli, sekä älypuhelimien myötä tuodaan myös digitaalisuutta mukaan.

Lisäksi Asmodeella on merkitystä, ei vain kehittäjänä vaan myös kolmansien osapuolien jakelijana, jossa se on suurin Euroopassa.

Pari linkkiä vielä lisäksi.

[Tabletop Gaming Market will grow at a CAGR of 12.20% from 2024 to 2031.] Pöytäpeliyhtiöiden kasvunäkymistä.

[Browse Board Games | BoardGameGeek] Tuossa hieman ranking listoja pöytäpeleistä.

Kiinnostavia kysymyksiä jää vielä avoimeksi…

- Saako Asmodee Pokemon kortti riippuvuutensa tasapainotettua?

- Pystyykö haastamaan Mattelin ja Hasbron markkinoilla?

- Onko Asmodee kiinnostava osake ja mihin arvo voisi kehittyä?