A comment like this from Barron’s:

1 Like

It is clear that Qualcomm cannot replace ARM with RISC-V in the short term; such a scenario is at least a 5-10 year project. So the possible scenarios here are, in order of probability:

-

Qualcomm and Arm end up settling their dispute and Qualcomm pays something for the license, which is likely more than before, but less than what Arm is asking for with its hand out.

-

Qualcomm pays Arm what Arm is asking for.

In both cases, in return Qualcomm receives an updated licensing agreement under which they clearly have permission to continue the development and use of Nuvia cores.

- The court provides its view on the alleged breach of contract (the point is that Qualcomm considers that the current license allows it to make these custom cores, the IP for which it acquired by buying the Nuvia startup. Arm considers that this is not OK, at least unless it gets more money, cf. Arm’s new licensing model) and based on that, Qualcomm then pays according to the former deal or more. I am not familiar enough with the exact arguments to evaluate what the court is likely to decide, and I strongly suspect that neither party actually wants to go all the way to a court ruling.

Note that the list does not include the option “Qualcomm stops using Arm IP in 60 days when it no longer has a license,” and the option “Qualcomm stops development of Nuvia cores” is also so far at the bottom of the list that it is not really realistic. So much money has been sunk into their development, and they are such a vital part of Qualcomm’s competitiveness compared to SoCs using “standard” Arm Cortex cores, that it is clear their use will continue.

As one article reporting on the situation summarizes:

“There is a degree of absurdity of Arm suing its second-biggest customer, and Qualcomm being sued by its largest supplier”

The shares of both companies will then swing at some point depending on the final outcome of the settlement. Arm hopes for bigger bags of money, Qualcomm does not want to pay more than now and does not want restrictions on its custom CPU development.

2 Likes

If you’re interested in an expert discussion on the topic of Arm - Qualcomm - RISC-V, I highly recommend this stream:

(it’s running live right now, available as a recording once it’s over; also, the first ten minutes are just general chatter and the real meat starts after that)

Edit: I came across an interesting analysis regarding this lawsuit that speculates a bit on the details and motives:

(no position in Arm or Qualcomm, but I’m following with interest because it affects so many other things in the chip market - since Arm is pretty much everywhere and the outcome of this mess could have far-reaching consequences)

4 Likes

Quarterly results are out. That is, Q2 FY2025. What immediately stands out from the figures is that the company is in R&D mode. R&D headcount has been increased and the operating margin—is that EBITDA then—has dropped. Steady growth in royalties (23% y-y) is a plus in otherwise lackluster numbers. But I need to take a closer look when I have more time to see what the company is actually up to now.

; it’s worth examining the first KPI tab in the Key Financial Data attachment. And the terms are explained at the end of the Shareholder Letter attachment; that’s where I spotted the “leading indicator” point I mentioned. There are other noteworthy things mentioned there too, such as the fact that the company does not include royalties in ACV or RPO figures in any form.

7 Likes

Arm makes steady results behind the biggest spotlights. CPU chips are still needed, even though sometimes it starts to feel like GPUs & software handle everything.

Amazon released its latest Arm-based cloud chip yesterday.

Amazon Unveils Graviton4: A 96-Core ARM CPU with 536.7 GBps Memory Bandwidth

2 Likes

So that’s a year-old thing and has been generally available via AWS since at least last summer. Its price/performance ratio is quite OK, but it naturally requires the program code to be recompiled, so it’s not very popular, as far as I understand.

4 Likes

Well, it was, but apparently, the cooperation continues. We should get new announcements so we can get a newer Graviton for this year too.

https://www.businesswire.com/news/home/20241220310709/en/Qualcomm-Statement-on-Trial-Verdict-Win

But the saga continues…

A week of courtroom arguments and deliberations ended in a mistrial after the jury failed to resolve one of three questions put before it in the trial between the two chip giants. Qualcomm said the result affirmed its right to innovate, but Arm vowed to seek a new trial.

2 Likes

It was a good interim result that Qualcomm can continue its production, for example, for the AI PC markets. As it is not in anyone’s interest if a major player were to be blocked in one of its product lines. But I also understood that the actual problem, the pricing of licenses, remained unresolved.

2 Likes

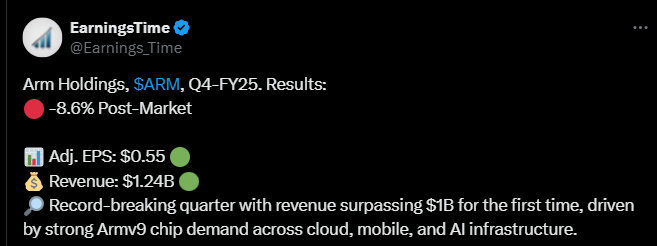

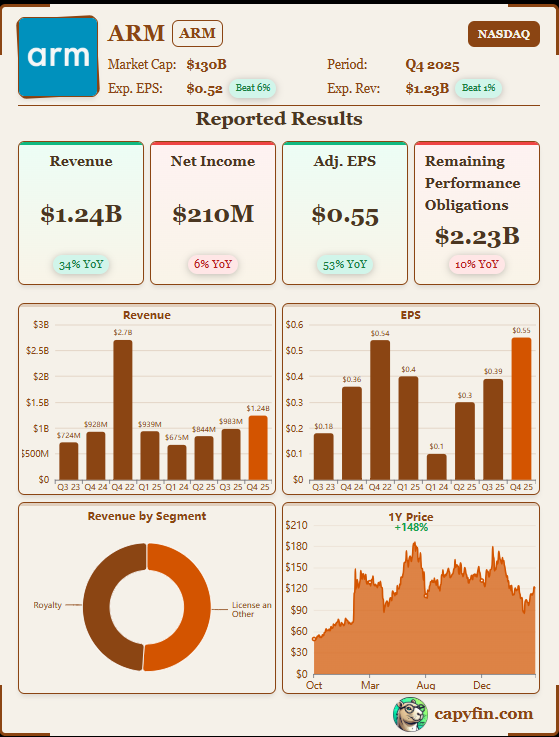

ARM released a new earnings report yesterday, which exceeded expectations in terms of both revenue and EPS. The guidance did not please the markets.

The company’s chip technology is used in almost all smartphones, including chipsets from Apple, Qualcomm, and MediaTek. Growing demand for AI and cloud computing is accelerating the use of ARM-based processors in data centers and AI computing chips. In addition, the company benefits from a scalable business model where licensing and royalty revenues provide stable and profitable cash flow.

China’s share of revenue is significant, but SoftBank’s control over ARM China reportedly brings risks. The stock’s valuation has risen with the AI enthusiasm, but based on what I’ve read, growth outside of mobile chips is crucial for maintaining its value. ![]()

https://x.com/ConsensusGurus/status/1887247150955864400

3 Likes

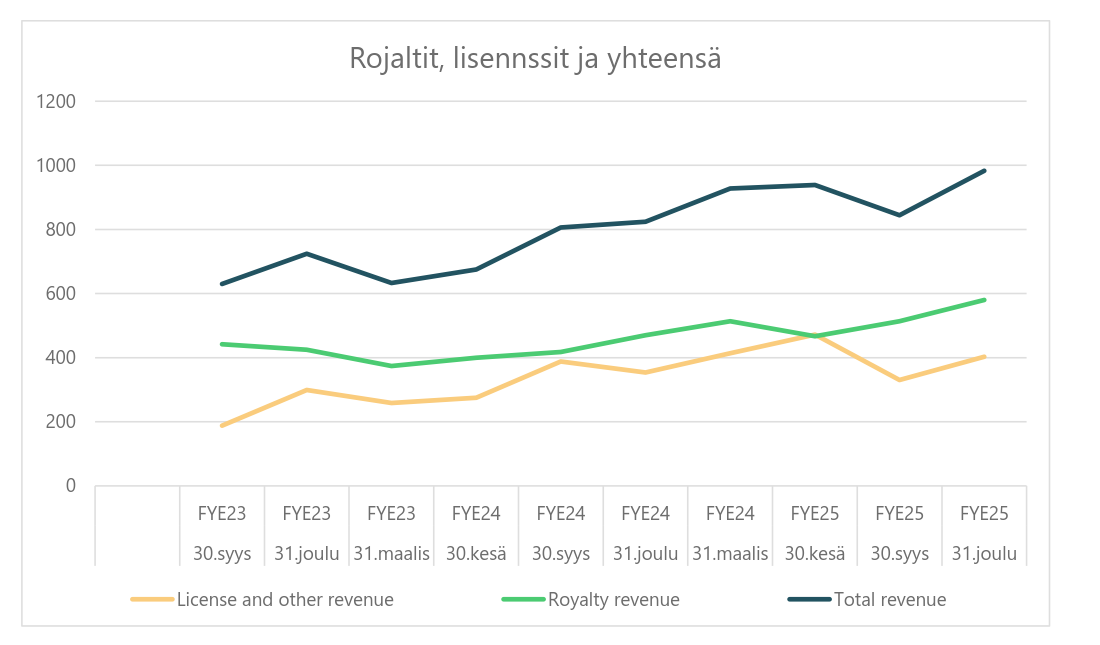

I went through those license and royalty figures with a fine-tooth comb. And I looked at the investor call comments. I know what I’m about to say sounds corny. But I’ll say it, investing in Arm is like putting money in the bank. And this is not an investment recommendation! But in my portfolio, Arm is a piggy bank. The company does meticulous work, meaning it sells licenses to later receive royalties. The company will generate 4 billion in revenue in the fiscal year ending March 2025. The formation of revenues between licenses and royalties is shown in the image below.

Through license sales, Nvidia and cloud mega-firms (Amazon, Microsoft, Google, etc.) get access to efficient CPU solutions, and then when end-user revenue is generated from them, Arm receives royalties. I think this is a good business, especially when we are at the core of AI.

The stock is highly valued, and there could be years when the stock yields nothing. One of the biggest risks for a stock investor, in my opinion, is that Arm’s main owner, Softbank, takes out loans against Arm’s shares for future large American AI projects. Then, if things don’t go as planned, the loans become due, and Softbank dumps Arm’s shares on the market. That’s what I’m trying to anticipate somehow.

7 Likes

Nyt on liikkeellä uutinen, että Arm alkaisi tehdä CPU-sirua Metalle

Arm secures Meta as first customer for ambitious new chip project, FT reports

2 Likes

This is where it all began 40 years ago. The picture shows Arm’s headquarters from 40 years ago, an old turkey shed near Cambridge. There are companies founded to generate maximum profit for their owners, and then there are companies that produce important innovations, like Arm, whose original goals under the name Acorn Computers were to produce a BBC Micro for every British classroom, back in 1978. The ARM1 processor was released in 1985. And back then, an energy-efficient processor had to be made because Acorn Computers couldn’t afford to put the ARM chip in a ceramic chip package, but rather in a plastic one. The plastic would probably have melted if the ARM chip had run hot. And the Nokia 6110 was Arm’s global breakthrough. You can read the story here:

Celebrating 40 Years of the Arm Architecture: From Cambridge to the World - Arm Newsroom

Arm had not released any significant news in the spring. Is there cause for concern, is Arm’s candle fading? Well, I’m not worried, because this is a company whose R&D expenses are 60% of its revenue, 99% of mobile devices use Arm technology, and there are 300 billion Arm-based chips. Someone has to do that R&D. The company focuses on its own game, and that’s the surest way to win the long game. I expect the usual results next Wednesday. Moderate growth and a relatively small net profit, because the company is clearly in R&D mode.

4 Likes

Bringing this here too:

2 Likes

Arm had a pretty decent quarter, as total revenue grew significantly from the previous year and exceeded the one billion dollar mark for the first time. Growth was particularly driven by license and royalty revenues, both of which rose to new records.

Royalty revenues grew as the Armv9 architecture and Arm CSS-based chips became more widespread, and as the use of data center solutions increased. In addition, license revenues grew strongly, due to several large agreements and deliveries from the previous order backlog.

While GAAP-based earnings slightly decreased compared to the previous year, adjusted earnings grew significantly. According to the company, with the spread of AI from cloud services to edge devices, the demand for energy-efficient computing solutions is growing, which Arm aims to widely enable.

https://x.com/Earnings_Time/status/1920209797040758958

Company Materials

3 Likes

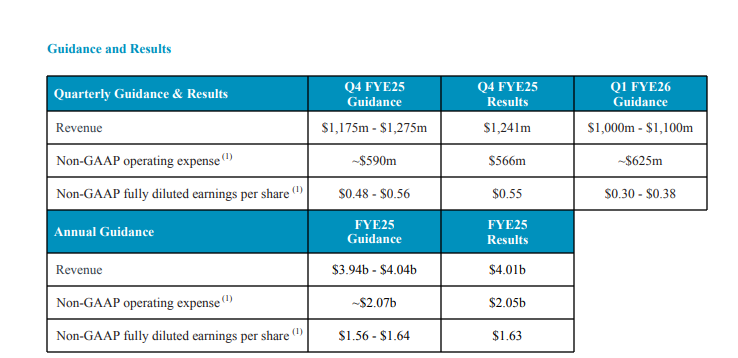

Exactly. The market didn’t like the weak guidance for the current quarter. A Seeking Alpha article had an interesting interpretation of the weak forecast: “CEO Rene Haas stated that the below-expectations guidance is due to a large licensing deal that may not close during Q1 2026.”

You can read more about the interpretation of the results here:

https://seekingalpha.com/article/4783601?gt=09e80a83384432c0

And on to the next earnings in 3 months. Hopefully, that revenue forecast dip will then turn into a bounce. It’s unlikely those deals will be left undone, although this was an Arm investor’s positive guess.

3 Likes

Arm’s quarterly results came out last week:

Exhibit 99.2 FYE26 Q1 (30-Jun-25) Shareholder Letter

The company is on a good fundamental trajectory; royalty growth is steady. The company’s balance sheet is in order, with $2.5 billion remaining after debts. Everything is, in a way, fine. But now we move on to a more interesting area, namely, speculations about the company’s future. In the investor call, CEO Rene Haas said, among other things, the following:

“We are continuing to explore the possibility of moving beyond our current platform into additional compute to subsystems, chiplets and potentially full-end solutions. To ensure these opportunities are executed successfully, we have accelerated the investment into our R&D. These investments include expanding engineering delivery across multiple levels, adding to the already significant product investments we have made to date. Momentum behind the broad CSS adoption and increased demand for AI compute on Arm are driving a powerful growth trajectory for the company.”

The company currently spends over 60% of its revenue on product development. R&D growth is shown below quarterly:

Something is brewing…

6 Likes

Arm officially released new hardware

1 Like

What do you think, @jarnis, previously there was a relatively clear license revenue stream. Now subcontractors are coming in, the gross margin is weakening, and the numbers will probably be rearranged somehow. What kind of near future lies ahead when the pure license/royalty pump transforms into a manufacturer?

1 Like