I was waiting for a dip in the share price with this one too, but after Midsummer, this will also be in my portfolio thanks to the Nasdaq 100.

1 Like

Definitely a good basic solution for exposure to Arm. And Arm certainly belongs in that portfolio. I’ve been trying to dig a bit into how Arm is doing. It looks like Arm possesses quite a bit of software expertise and creates/supports developer networks. Here’s one example below:

Add sentiment analysis on Graviton using Hugging Face - Infrastructure Solutions blog - Arm Community blogs - Arm Community

The example was sentiment analysis from text, and perhaps even from multimodal data. These examples are relaxing to explore because your brain sometimes starts to get exhausted if you only study these chip companies at a high level. In other words, the linked article discusses how new architectural solutions can get more out of the silicon with less power. And architecture is more software than HW. And Arm is, of course, very much involved in how the line is drawn between SW and HW.

@Roope_K shared an interesting VTT article in the Nvidia thread. Flow Computing is once again a new interesting addition to the whole computing network.

Returning to Arm. I can’t understand what the market is doing with it right now. Is it a short squeeze because Softbank is holding onto the shares and the so-called float, i.e., the number of shares on the market, is small? Are hedge funds playing their familiar short-term game with the stock? But why would they play at such a high valuation? Because in the short term, the price would be expected to slide back towards a hundred.

On the other hand, NVIDIA is sticking tightly to its ARM CPU strategy and integrating Arm into its new solutions. Very purposefully, so the CPU isn’t dying off anywhere. Then the “Arm-backed Raspberry Pi” was listed with much fanfare on the London Stock Exchange. Broadcom and Qualcomm are in some kind of AI upturn, they use Arm, AI PCs are coming soon, and Qualcomm has Arm-based chips.

It’s really hard to grasp Arm from an investor’s perspective. It feels like there are many Arm-related angles in the air right now. But is it so that nothing will provide a massive boost to the fairly stable license and royalty stream? In other words, is this just another hype bubble, and after the earnings on August 7th, the excitement will deflate when Arm gives conservative guidance contrary to the current price?

As you can see, I’m quite confused about Arm. But since it was a company Jensen wanted badly, I think Jensen already saw 10 years ahead in 2020 what Arm’s value is in IoT, edge, mobile, and he saw the server-side benefits of CPUs.

And then we already know that Softbank is making Arm produce, i.e., manufacture AI chips. And Arm has its own GPU too.

Summa summarum. It’s quite impossible to say anything other than that Arm apparently continues to be at the hot core of the AI world and is also striving to grow its own revenue and earnings.

Against what I’ve said above, that Nasdaq 100 exposure feels like a good basic solution. But I will continue with direct stock exposure because the future looks very interesting and will bring surprises anyway.

9 Likes

I am sharing this same “video summary” to both the Arm and Nvidia threads. This is about a person named Masayoshi Son. The visions he presents in his video, even if only partially realized, define the new paths that will catapult the significance of AI to a whole new level. This summary is based on a video found on YouTube of SoftBank’s annual general meeting on June 21, 2024 (SoftBank Group Corp. The 44th Annual General Meeting of Shareholders - June 21, 2024). The most interesting parts start from the 26-minute mark.

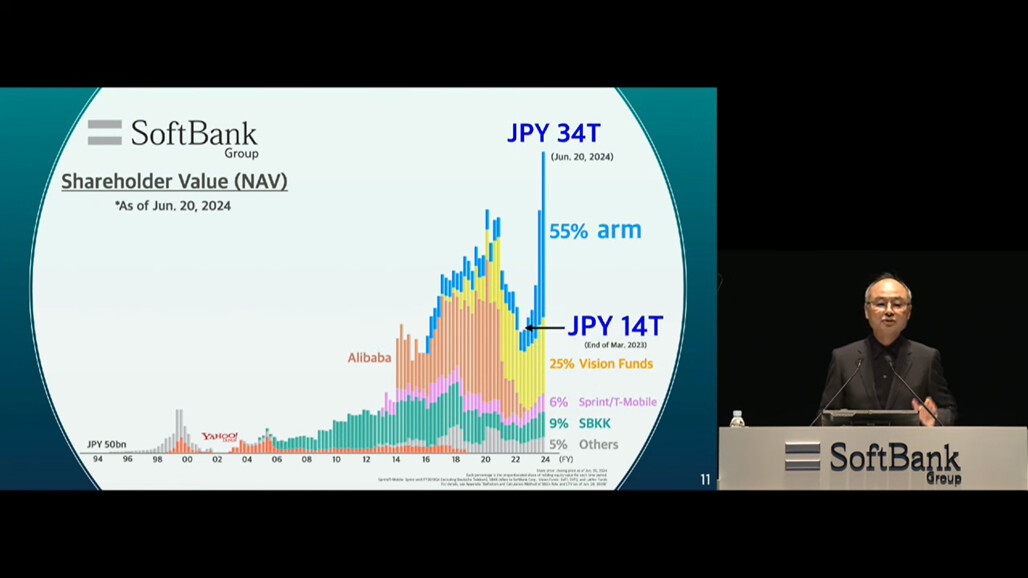

Masayoshi Son founded the Japanese company SoftBank in 1981. Masa is therefore an entrepreneur and one of Japan’s wealthiest individuals. The following image gives a broad overview of Masa’s and SoftBank’s history. SoftBank is behind the likes of Yahoo and Alibaba. Masa is known for suffering the world’s largest losses with his company during the dot-com bubble (1999-2002). From the image, one can infer that SoftBank survived in 2002 mainly due to the goodwill of banks.

In the video, Masa talks about how a couple of years ago he was desperate because he hadn’t achieved anything significant.

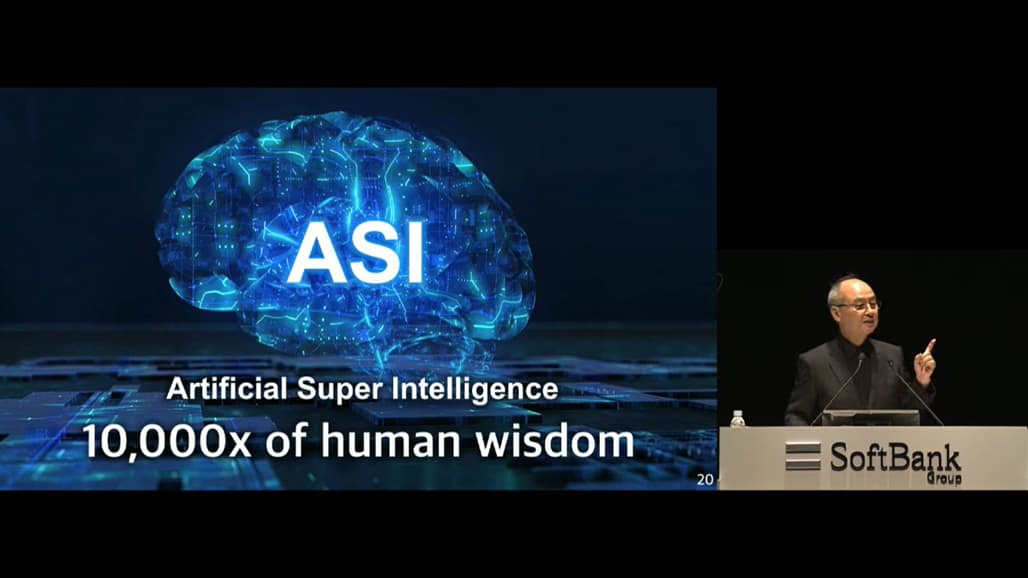

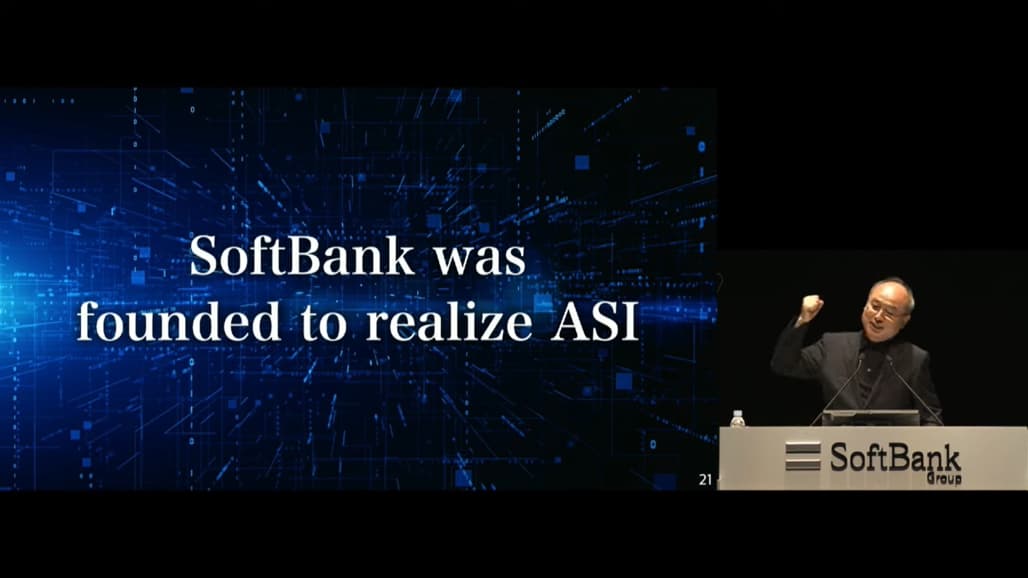

Now, on June 21, 2024, he revealed that a year ago on June 11, 2023, he realized that ASI, Artificial Super Intelligence, is the purpose for which he founded his company. Everything up until now has been a warm-up for this actual purpose.

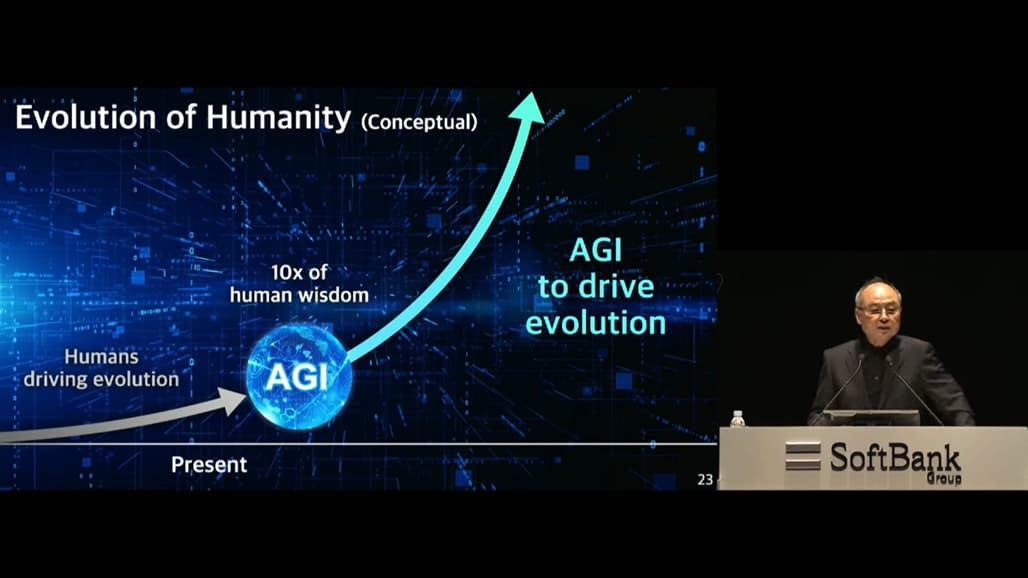

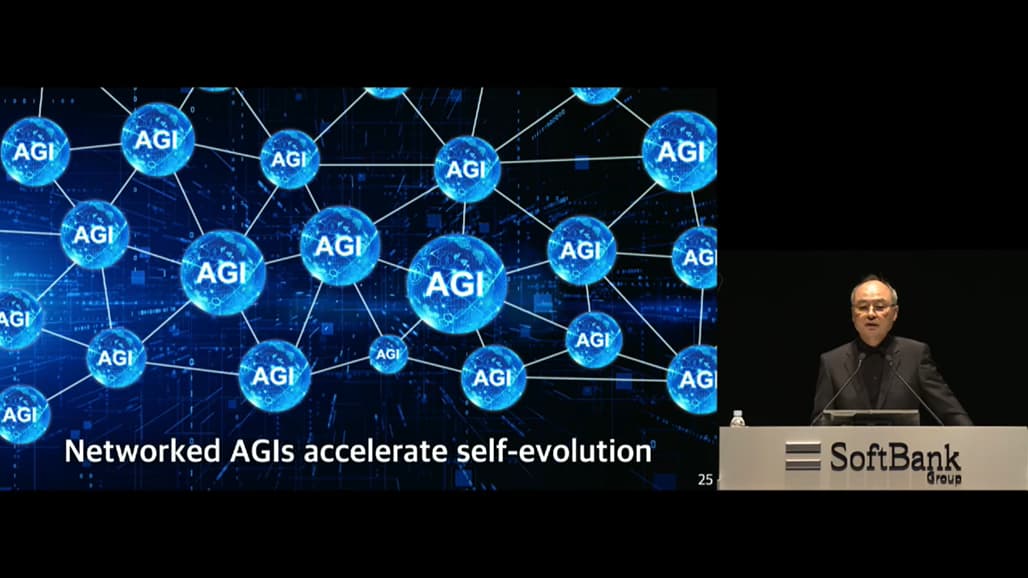

In the video, Masa goes through his own thinking regarding ASI. AGI (Artificial General Intelligence) is the stage where AI’s thinking is equivalent to wise men and women. It will be achieved within a few years.

AGIs will network, giving birth to ASI (Artificial Super Intelligence). It will help people; it will be beneficial.

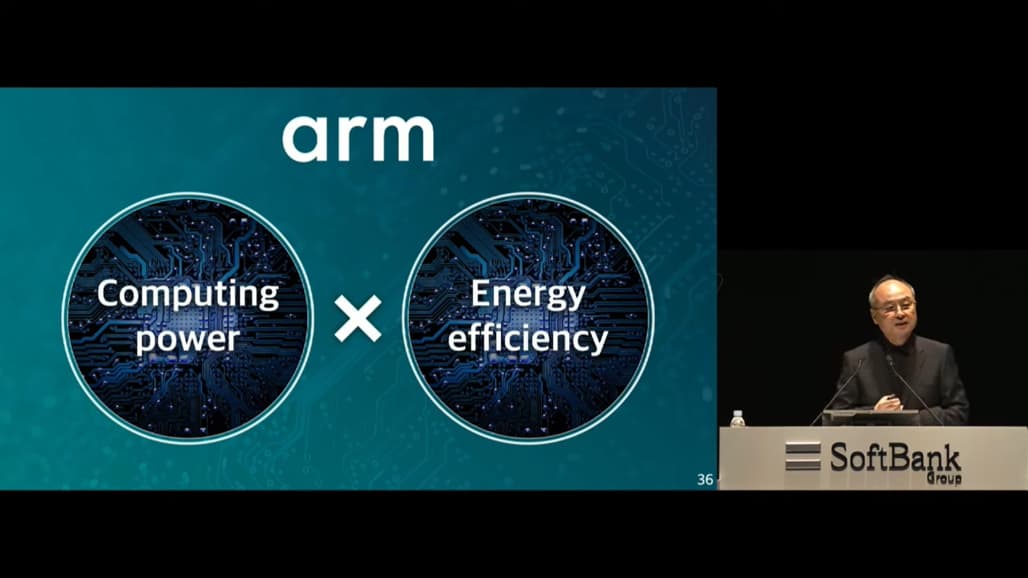

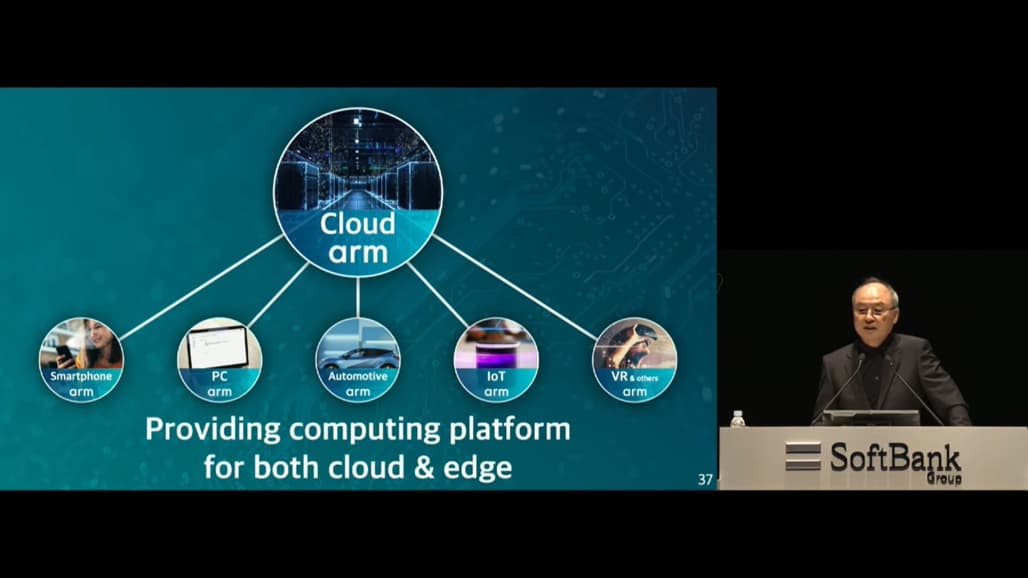

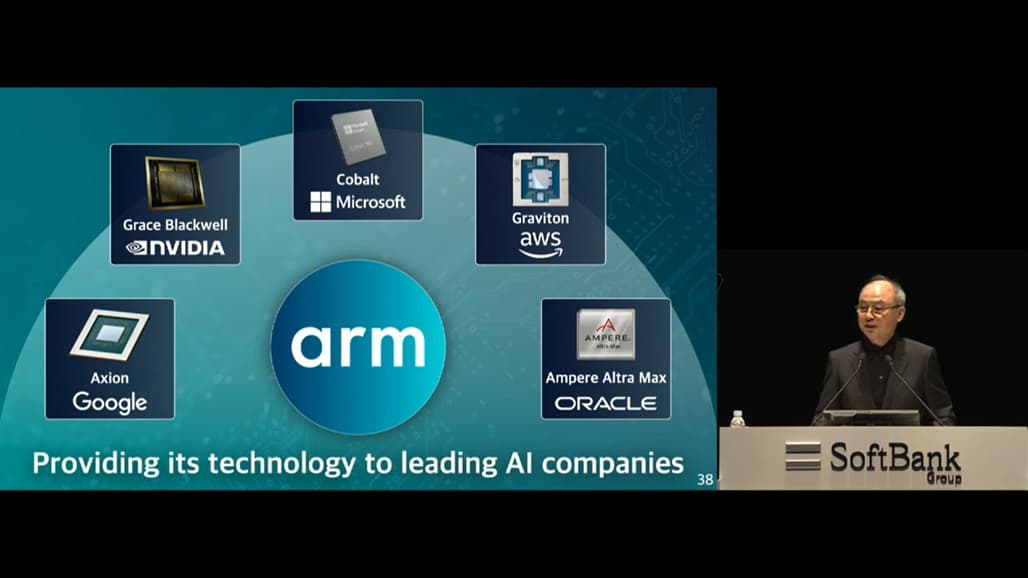

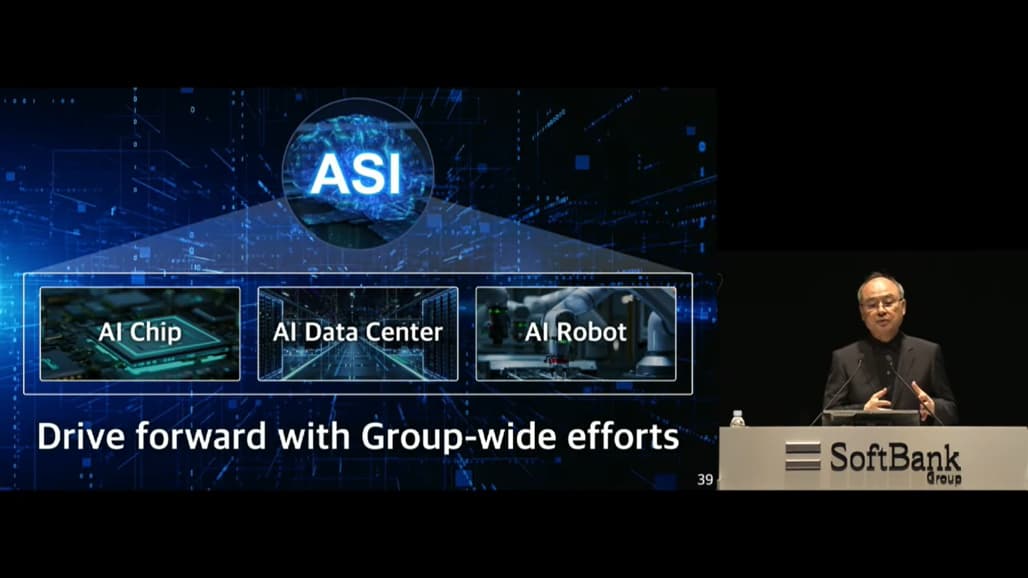

The image below is a ten out of ten in terms of overall architecture. The image shows how Super Intelligence is put to work, i.e., producing concrete things.

And it’s not very far off, 10 years at most.

SoftBank states that it is a key player in the ASI evolution through Arm.

Because the Arm architecture is precisely suited for AGI and ASI.

In light of the above, I am no longer surprised why SoftBank has been talking about Arm starting to manufacture chips itself. Because they will be needed, and in large quantities, when AGI is taken to the edge.

Partners have already been found.

The next slide is important – according to Masa, all players are needed for cooperation.

The video shows how confident Masayoshi Son is in his vision. Notice Masa’s determination in the image below. It shows that he’s going all in, no half-measures! SoftBank and Masayoshi Son exist to produce Super Intelligence, together with their partners. Everything SoftBank has done so far has been a warm-up for this next phase.

6 Likes

A bit of nostalgia - Nokia was a jackpot for Arm, allowing them to showcase their capabilities in energy-efficient processing. And the snake game was one of the first mobile games. And for those of us who used Nokia phones around the turn of the millennium, their batteries were famously long-lasting ![]()

Arm’s IP lent itself perfectly to the smaller form factor and more consumer-friendly designs of the new GSM-powered mobile phones. In the mid-90s, Nokia was advised to use Arm-based designs by Texas Instruments, a significant Arm silicon partner at the time, for the company’s new GSM mobile phone. This led to the first Arm-powered GSM phone, the Nokia 6110, which was a big commercial success. The 6110 paved the way for the iconic Nokia phones of the late 90s and early 00s, such as the 3210 and 3310. These adopted a similar but smaller brick-style form factor. It was on these phones that mobile gaming was first introduced to the world through 'snake, the original game for mobile. This era signaled the start of the mass-market ‘mobile revolution.

You can read more here:

History of the Mobile Form Factor - Architectures and Processors blog - Arm Community blogs - Arm Community

4 Likes

Arm’s earnings and guidance will be released at the end of July. It is still difficult to get a complete picture of the company from this point forward. Or, on second thought regarding what I just said, I’m taking a new stance on Arm. The fact is that right now, no one in the world knows Arm’s order backlog for 2026 and beyond, because the AI market is constantly evolving and taking shape. Having read various sources, it is my personal opinion that Arm is now everyone’s friend; everyone wants to partner with Arm, and Arm is vital to every AI company, including AMD and Intel. And while Qualcomm and Arm are currently in court, smart companies usually seek rational resolutions to disputes behind the scenes.

Arm is the Visa of the AI world. Both are dominant players in their respective industries that don’t build the basic infrastructure itself but provide significant value-add to the value chain; therefore, they can command massive gross margins—97% for Visa and nearly 96% for Arm.

I want to share one analysis of Arm here, as I feel it does a good job of explaining the AI landscape opening up for the company. I haven’t come across comprehensive overviews like this before. The link is a “gift link,” so it should be accessible to everyone without a paywall.

https://seekingalpha.com/article/4699519?gt=5bf3556fc2309861

6 Likes

Does anyone have a clearer understanding of what factors are behind the stock’s rise during the summer months?

1 Like

A small boost likely came from being included in the Nasdaq 100 index. But I actually elaborated on this earlier. Arm is involved on the server side, at the edge, in AI PCs, in IoT—practically everywhere where there is AI. The market is now anticipating the results to be released on July 31. Mainly, the focus will be on the forecast for the rest of the year, and the market assumes that license sales and royalties have shifted into accelerating growth.

In addition, the Semiconductor Industry Association (SIA) published a forecast on June 6 (link below) regarding the growth of the semiconductor market; the key point is that the semiconductor market dipped in 2023 and has now turned toward clear growth. Some analysts have indicated that Arm’s royalties will start growing at a steeper rate than the overall semiconductor market.

Global Semiconductor Sales Increase 15.8% Year-to-Year in April; New Industry Forecast Projects Market Growth of 16.0% in 2024 - Semiconductor Industry Association

6 Likes

Now that Arm has reached broader headlines through the Nasdaq 100 index, fresh analysis and market forecasts are also becoming available. I am sharing here another Seeking Alpha analysis, which should again be available to all readers without paywalls. It seems that analysts have bought into the analysis forecasts of The Information Network research firm, and based on that, for example, Bank of America sees significant growth for Arm in the coming years.

It is worth looking at at least those tables from The Information Network inside the Seeking Alpha article via the link below. Those tables are unlikely to be available anywhere else (except by purchasing).

Additionally, I picked the following text from the linked article, which describes well that Arm is everywhere:

"As noted above Qualcomm with its Snapdragon series, Samsung with its Exynos chips, and MediaTek with its Dimensity processors all use ARM’s advanced cores.

Investors and readers of this article should not consider an investment in ARM as an alternative to NVDA, as they are not direct competitors and instead, their business models are complementary as noted above with the Nvidia Grace CPU built on ARM’s Neoverse architecture. Nvidia has also used ARM architecture in its Tegra processors.

Indeed, ARM’s architecture has been centered on its use in mobile devices, but is increasingly found in data centers. However, the synergy in collaborative ventures between the two companies, manifested in the Nvidia Grace CPU serves as a trend in the industry between the two companies."

So, check out at least the tables here to get an indication of why the market likes Arm right now:

https://seekingalpha.com/article/4702993?gt=aa2775b75c0bd419

6 Likes

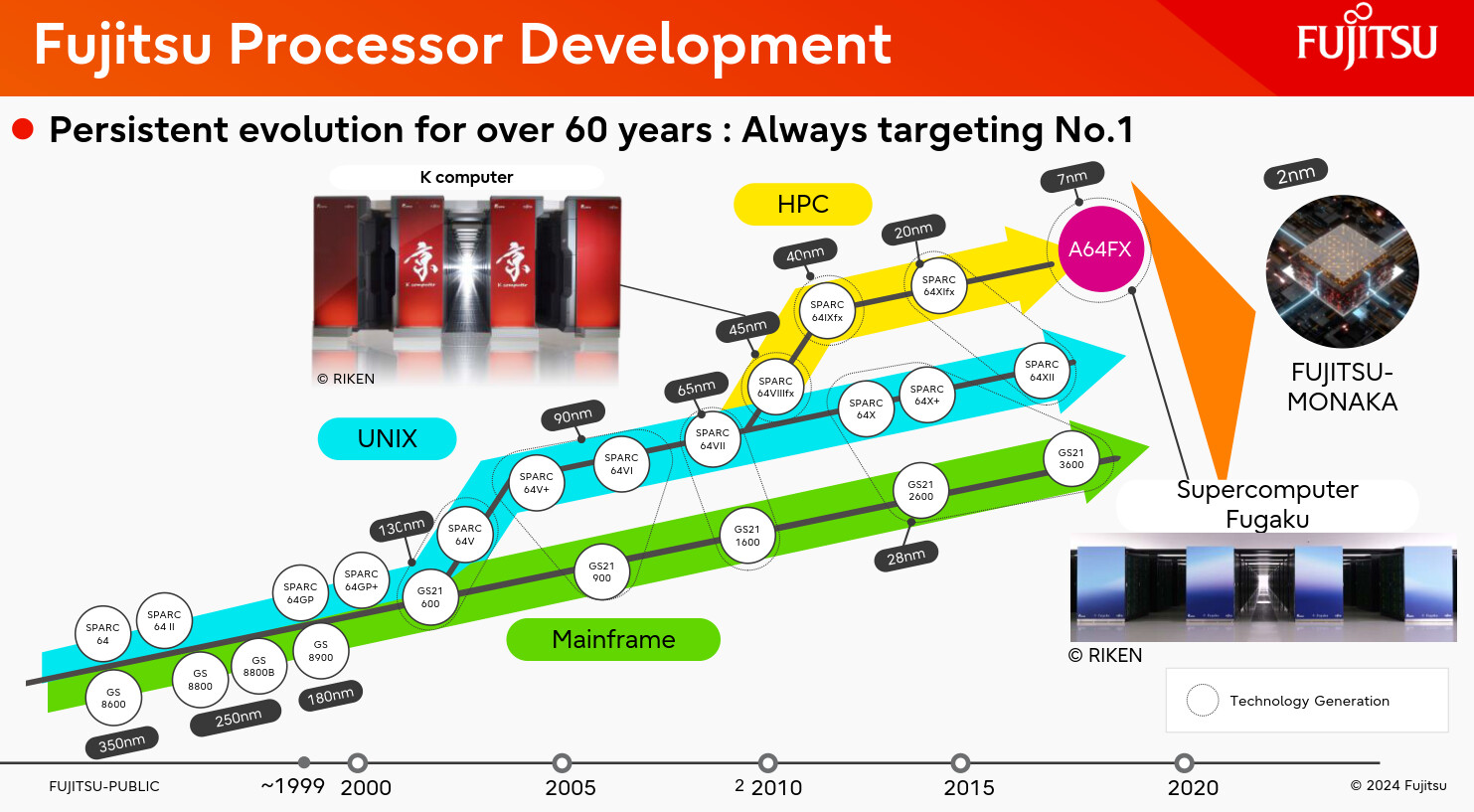

Below is a link to a news article published by Fujitsu regarding the collaboration between Fujitsu and Arm. In a nutshell, Fujitsu is building world-class supercomputers/datacenters in Japan. Below is a roadmap image; FUJITSU-MONAKA is an Arm-based AI CPU that powers Supercomputer Fugaku:

This is a big deal. TSMC has announced it will set up a factory in Japan. I have a feeling that SoftBank is currently plotting something that we’ll hear about at some point. It could be significant for Arm. It’s a very good thing for the overall development of AI that Japan is now also investing in AI. And Arm is in a fantastic position right now because it’s involved in practically all new datacenter CPU/chip announcements (Google, Amazon, Microsoft, Fujitsu, Nvidia…).

In pursuit of energy efficiency: How Fujitsu and Arm are shaping AI’s tomorrow : Fujitsu Global

5 Likes

There’s a lot of interesting content in Fujitsu’s FUJITSU-MONAKA slides; you can find the slides here:

Next Arm Processor FUJITSU-MONAKA and Its Technologies

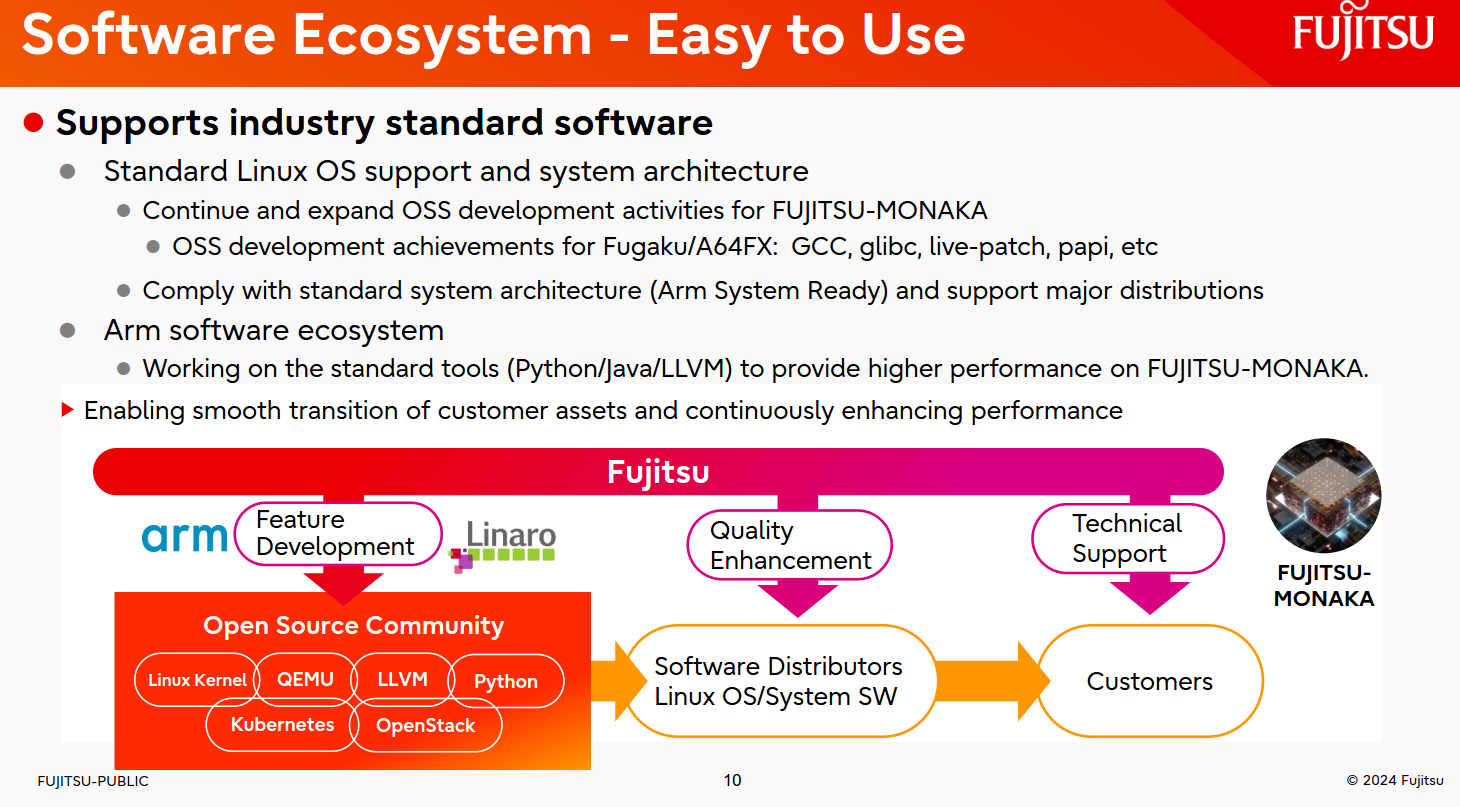

I’ll highlight a couple of slides here. This first slide shows that Arm has become a so-called standard, so new systems are being built around it, which Fujitsu also justifies in this slide - Arm software ecosystem.

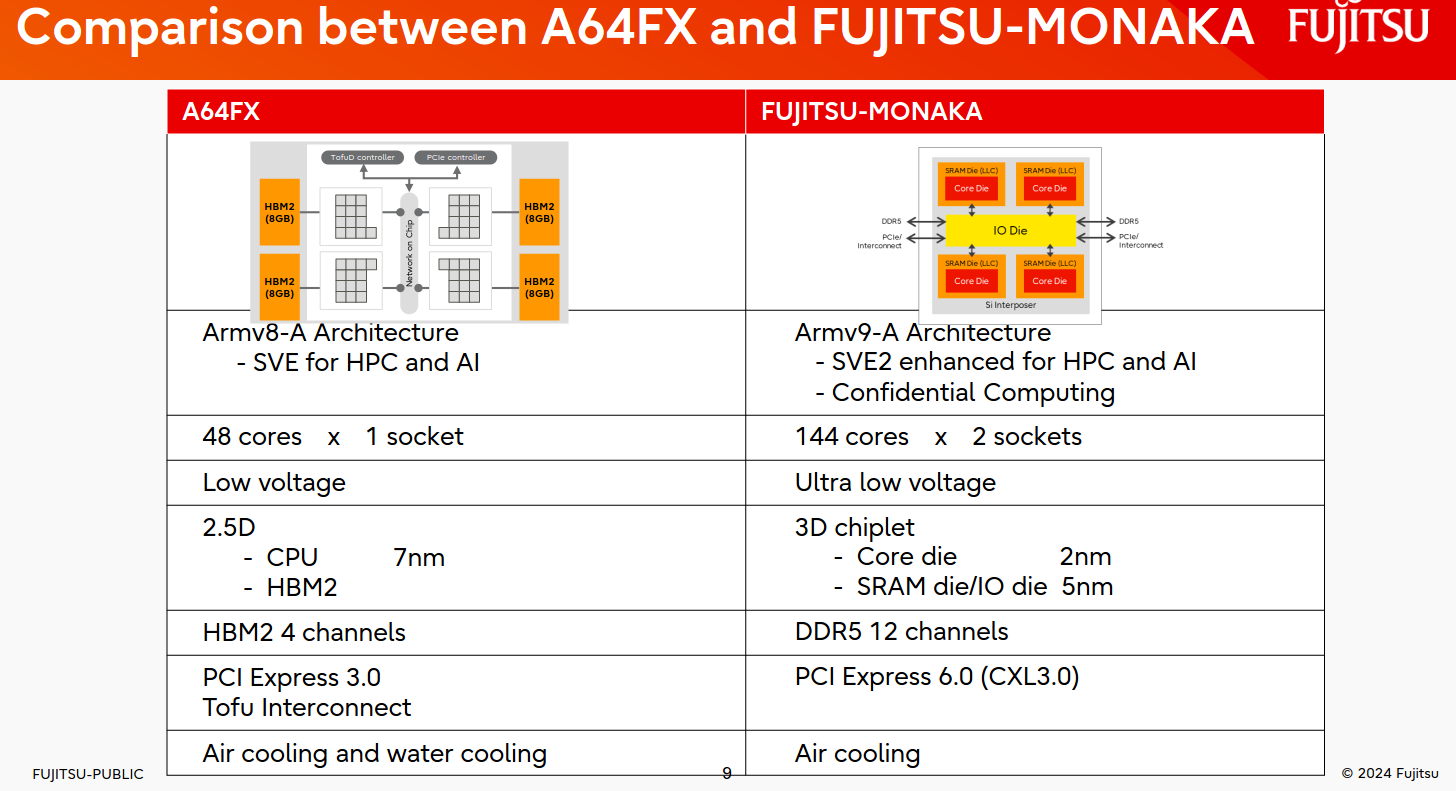

The next slide contains an interesting technical specification → air cooling is sufficient for MONAKA! This is how Arm disrupts Supermicro ![]()

6 Likes

ARM released its earnings report:

Revenue grew by 39% and the EPS (non-GAAP) figure was $0.40. EPS growth was 67% compared to the previous year.

https://investors.arm.com/static-files/559eabc5-4dce-4cfe-bfaf-bb19735eeb40

10 Likes

Arm’s Q1 was released Wednesday evening. The numbers provide something for everyone, i.e., bears and bulls can emphasize their own figures. The so-called official numbers include 39% year-on-year revenue growth, negative cash flow for the period, clearly positive GAAP net income, 2% annual share dilution, and a solid debt-free cash position of over 2 billion.

What do I think myself, then? Here, I’ll highlight points I mostly picked up from the earnings call. For the next/current quarter, the company forecasts a dip in revenue and earnings, and then the fiscal year ending March 31, 2025, will have its best performance in Q4. The company did not change its forecasts for the current fiscal year 2025 after the fiscal year that ended on March 31, 2024.

For the bears, I’ve picked two things from the results. Q2 (ending September 30) will see a dip in revenue and earnings. And the company lowered its royalty growth percentage forecast for Q2 from the mid-20s (approx. 25%) to the low-20s (perhaps 21–22%). For the bulls, the CFO’s words in the earnings call stand out: “However, we also expect Q2 to be one of our highest bookings quarters of the years.” Meaning, deals are being made.

What spoke to me most in the results was how the 39% annual revenue growth was split between license sales and royalties. License sales grew 72% year-on-year, and royalties 17%. It emerged in the earnings call that the time frame from license sales to royalty growth can be as long as 3–5 years. Analysts and investors have plenty to chew on regarding how the company is valued. Therefore, the company will certainly provide investors with significant volatility.

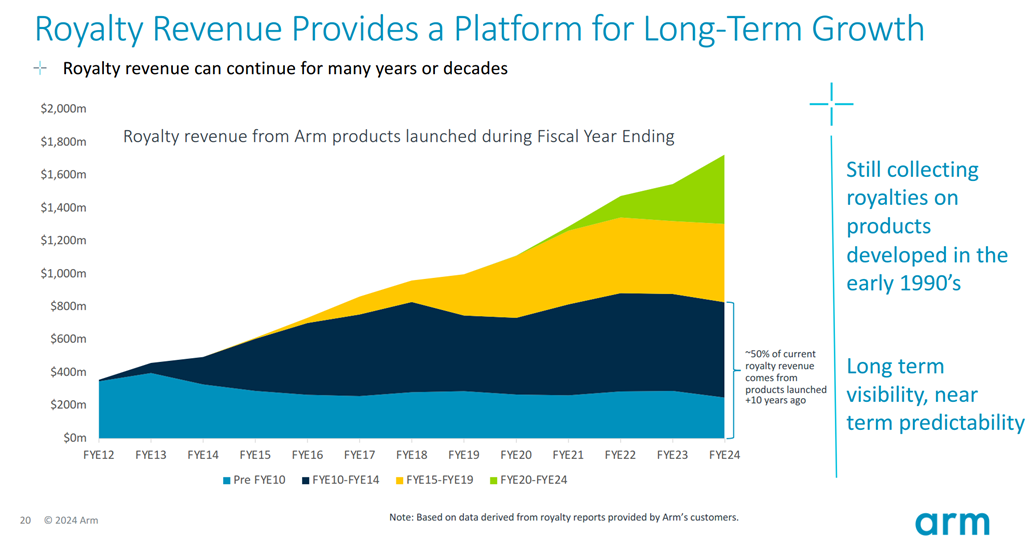

If I summarize why I’m in this company with one image, it’s this:

My own thought is that, over time, the royalties from the licenses currently being sold will make the company the Visa of the chip market. This means Arm will receive steadily growing royalties over a 5–10 year horizon from expanding license sales in a chip world that is growing much larger than it is today. This will ultimately justify an even higher valuation for the company, which even now is considered outrageous by the general investing public (at least the Seeking Alpha investor forum slams the valuation).

Arm’s slides can be found here:

9 Likes

Google has launched the Pixel 9 series, featuring the new Tensor G4 chip, Titan M2 security, more RAM, and enhanced AI features.

Eli tuo Tensor G4 chip on Arm pohjainen ja Titan M2 security processori on RISC-V tyyppinen. Eli ns. “kilpailevat” ratkaisut voivat pyöriä sulassa sovussa päätelaitteissa.

Onhan tämä ihan merkittävä Google ja AI uutinen:

The Pixel 9 series boasts a faster chip, brighter screens, new AI tricks, and a foldable | Android Central

5 Likes

Arm may be developing a new GPU in bid to challenge Nvidia | TechSpot

There are rumors that Arm’s Israeli unit is designing a new GPU for either gaming or AI needs. There is probably nothing more to say about this rumor for now; Arm will make an official announcement when the time comes.

3 Likes

Or maybe not. According to this, the G4 chip is pretty much the same as the G3. Google had messed up the schedule for the new chip or something.

2 Likes

I came across a video that offers a slightly deeper technical perspective on ARM architecture. I’m not involved with processor architectures in any way, so my interpretations are quite basic. Correct me if I’m wrong, but here are my observations from an investment case perspective:

- ARM’s biggest(?) advantage compared to x86/64 architectures is likely its “lightness,” meaning, for example, very minimal backward compatibility. Based on a hunch, this sounds like a significant factor when considering expanding use cases.

- Related to this lightness, ARM lacks many features that are practically mandatory to implement if ARM wants to compete in the same markets as, for example, x86/64 → Would it still be possible to maintain the competitive advantages?

I hasn’t put a penny into ARM, even though I’ve been tempted. However, it somewhat feels like unless its future success is largely based on carefully crafted brand images, there’s a major risk of the technical side fizzling out into the same category as the others, or otherwise staying in its “own waters.” On the other hand, if ARM is already something completely different in practice than the perceptions built on the first ARM-based chips, how far could that reputation carry it ![]() ? Of course, I’d prefer competitive advantages based on things other than just reputation.

? Of course, I’d prefer competitive advantages based on things other than just reputation.

3 Likes

Yep, there are much easier chip plays than Arm. For example, a generally solid, reputable combo would be Nvidia+TSMC. It’s hard for a layman to evaluate competitive advantages. I have some skin in the game because Nvidia was all-in on Arm and wanted to buy the company for 40 billion in 2020. Another reason is that Apple, as a top player, relies on Arm for its architecture, as do many others: Nvidia (Nvidia’s Grace-Blackwell Superchip, or GB200 for short, combines a 72 Arm core CPU), Amazon, etc.

Arm isn’t the same kind of winning machine as Nvidia, because Arm’s growth consists of small streams from here and there. To me, it’s the Visa of the chip world—right in the middle of everything, with thin but long-term contracts. Perhaps because of that wide entrenchment, it might be hard to displace.

And through Arm, you can follow the spread of AI at the edge, where trained systems make those AI decisions. My understanding is that the architecture is energy-efficient, the solutions are cyber-secure, the company has a long track record (which is a plus in the chip world), and it builds IoT solutions and various types of automation (inferencing at the edge) as part of ecosystems.

On investor forums like Seeking Alpha, out of ten writers, 6 give a hold, 2 a strong sell, 1 a sell, and 1 a buy. It might turn out that this is a good company but a bad investment. But as they say, hobbies cost money ![]() .

.

4 Likes

The dispute between Arm and Qualcomm that was lingering in the background has now reached a point where Arm canceled Qualcomm’s license. The notice period is 60 days. So, there will be plenty of action for at least the next couple of months. I can’t fully assess the situation – Arm obviously has plans that triggered the escalation of the dispute now. I’ll be watching from the sidelines to see how things develop. In the big picture, I think the expansion of RISC-V is market dynamics and not necessarily a bad thing for the development of the mobile AI market.

1 Like

This is just a tactical move to pressure Qualcomm into settling before the trial. And this mess will most likely still be settled out of court. They are arm-wrestling over money.

4 Likes

Well, of course, drama and negotiation at the same time. Good points raised on this!