It’s exactly as you say. If I were looking to get in right now, I would enter with 3x 0.5% positions of the portfolio: the first buy tonight, the second in a few weeks, and the third a bit later. Then I’d wait and see if it trends lower. With Arm, the goal is to reach the stage where Arm IP is properly spread far and wide and royalties are rolling in. I’ve been thinking that 500 billion is not a utopian valuation for an IP in a monopoly position. Selling isn’t triggered by the price, but by the current unique position eroding or disappearing.

4 Likes

I wanted to come back to this. If I were only looking at the valuation and Arm, I wouldn’t feel good about it. But Arm is a mandatory part of my so-called AI “full house,” which consists of IonQ, Nvidia, Arm, Palantir, and Supermicro. That’s a sort of AI “super five.” One of them takes their turn going overboard, but I think it’s a good hand for the moment.

7 Likes

Well, I’ll put it this way: you are the only person I follow on the forum. I’m kicking myself for not daring to take any positions.

1 Like

Yeah, I’ve been thinking a lot about this exact moment. Valuations are high, but the US has rate cuts ahead, or if they don’t happen, we’ll get strong economic growth. I wonder if the US economy has been this strong since the '60s. In ten years, people will be wondering why India and China didn’t actually overtake the US economy. Well, they didn’t because US productivity is taking a giant leap now. That “full house” is a key driver of productivity. And there’s also a crisis component to it. If we drift closer to war in Europe, that “super five” includes companies whose solutions will see increased demand from the federal government. The next big conflict will be settled more through IT than we might realize.

2 Likes

Yes, the biggest psychological hurdle is buying into a massive rally. Nvidia’s P/E is falling, and it might actually be the cheapest chipmaker. It’s a mental struggle, even though it already makes up over 6% of my portfolio.

3 Likes

So, HIMS has been a stomach acid balancer for me. Its P/S is reasonable. Ultimately, your portfolio needs to be such that the stocks together form a whole that you can stay put with, rather than constantly overreaching through trading. The portfolio should have the holder’s own strong story. It has to feel like your own. It took me 3 years to get the package together. 3 years ago, I think I was doing 80 trades a year. Now the pieces are in place and trading is at a minimum.

7 Likes

Arm is the only company on the planet that can provide the necessary level of ISA parity from cloud to edge.

That sentence is taken from the article below. Self-driving cars and robots are at the edge, and the embedded systems in cars/robots communicate with the cloud. In its article, Arm explains that the Arm architecture enables such a strong connection between the cloud and the edge (car) in software management that autonomous driving is now breaking through. This cloud-to-edge connection is thus once again one of Arm’s moats. And likely one of those things that Jensen saw several years ago. While NVIDIA’s engines are grinding in the cloud, from time to time the cloud needs to communicate with the edge. The processors in embedded systems at the edge are extremely fast, secure, and energy-efficient. Arm architecture.

Extracting ISA Parity from Cloud to Edge: Why This Matters to the Ecosystem - Arm Newsroom

7 Likes

I revisited Beth Kindig’s previously published article. Beth summarizes the risks for the investor as follows: “The rich valuation combined with lockup expiration is the predominant risk, however, the longer-term risk is RISC-V.” In other words, a luxury valuation level combined with the fact that Softbank will start selling is, according to Beth, an obvious risk for the investor. The situation is strange anyway, because the value of Softbank’s Arm investment (120 billion) is not fully reflected in Softbank’s own valuation (80 billion). At the very least, the market is saying that when Softbank starts selling, 1/3 will be cut from the price. What will Softbank do then, will it listen to the market? The conclusion would be that according to the market, the price will drop by 1/3, and according to Beth’s article, the overvaluation is around 50% when she performs valuation metric comparisons. So Beth will enter after a 50% dip.

According to Beth, the only competitor is RISC-V (open source since 2019).

The main theme of Beth’s article is that she wants to get into the company. Well, I won’t dwell on this valuation matter any further, as I’m no master of timing myself either. Now that those Microsoft OpenAI rumors of 100 billion deals are in the air, AI momentum continues anyway, the quarter has ended, and we’ll soon see good quarterly results across the board from IT companies, it’s a very difficult situation to scout for entry points. Personally, I won’t sell, because I’m either in or I’m out, but I won’t start timing or trading; I’d just end up getting my fingers burned anyway.

6 Likes

I asked the computer which chip and cloud companies rely on Arm and which ones rely on RISC-V. These were the answers:

ARM

| Chip Companies | Cloud Companies |

|---|---|

| Apple | Amazon Web Services (AWS) (Graviton) |

| AppliedMicro (now: Ampere Computing) | Microsoft Azure (Dpsv5) |

| Broadcom | Google Cloud Platform (GCP) (T2A) |

| Cavium (now: Marvell) | Oracle Cloud Infrastructure (OCI) (A1) |

| Digital Equipment Corporation | |

| Intel (for some custom chips) | |

| Nvidia | |

| Qualcomm | |

| Samsung Electronics | |

| Fujitsu | |

| NUVIA Inc. (acquired by Qualcomm in 2021) |

These companies have designed cores that implement ARM architecture, and their chips are widely used in various devices. Additionally, cloud providers like AWS, Microsoft Azure, Google Cloud Platform, and Oracle Cloud Infrastructure offer ARM-based instances for their services12. Google Cloud, for instance, has recently introduced its custom Arm-based CPUs called “Google Axion Processors” for data center use, which deliver industry-leading performance and energy efficiency3. Microsoft has also started offering ARM-based VMs in Azure4.

And similarly, the competing open source solution RISC-V

| Chip Companies | Cloud Companies |

|---|---|

| AdaCore | Scaleway (European cloud provider) |

| SiFive | Alibaba (Chinese tech giant) |

| Antmicro | |

| Microsemi |

Meta’s RISC-V project and the startup Rivos, among others, should be added to the list.

6 Likes

Additionally, RISC-V can be found embedded in, for example, hard drive controllers:

And if you want big names on the list, NVIDIA has been using it embedded in its GPUs for years:

The component goes by the name GSP (GPU System Processor), which acts as an on-chip microcontroller. It doesn’t offer much benefit to outsiders, but every even remotely modern NVIDIA GPU has a small RISC-V core inside that the driver uses for chip startup and management.

Furthermore, there has been movement towards RISC-V in China because it has been realized that if this becomes a bigger thing, it will enable home-grown processors without licensing drama if sanctions continue to tighten.

It should keep ARM in check regarding licensing terms and will surely gain ground in embedded use where every penny counts and paying for ARM cores hurts the product margin too much.

4 Likes

A few highlights from the investor call. Analysts pointed out that in the IPO materials, the company spoke about Arm’s growth being at the 10% level. Now, CEO Haas said that they will exceed the 20% level in the coming years. Well, this explains why Arm, already considered expensive at its IPO, has nonetheless stretched its valuation even higher.

But if we leave the share price aside for now and look at the company’s numbers and services, Arm’s performance is quite exemplary. Operating cash flow over the past year was approximately 1 billion in the black. The cash position is around 2-3 billion, after debt. There didn’t seem to be much debt at all.

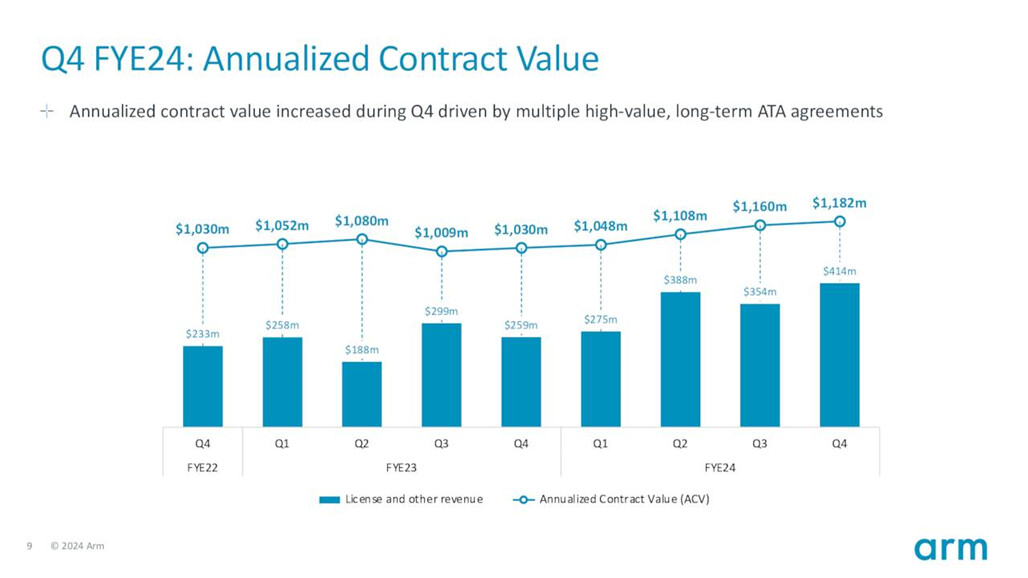

The company receives guaranteed cash flow from long-term contracts:

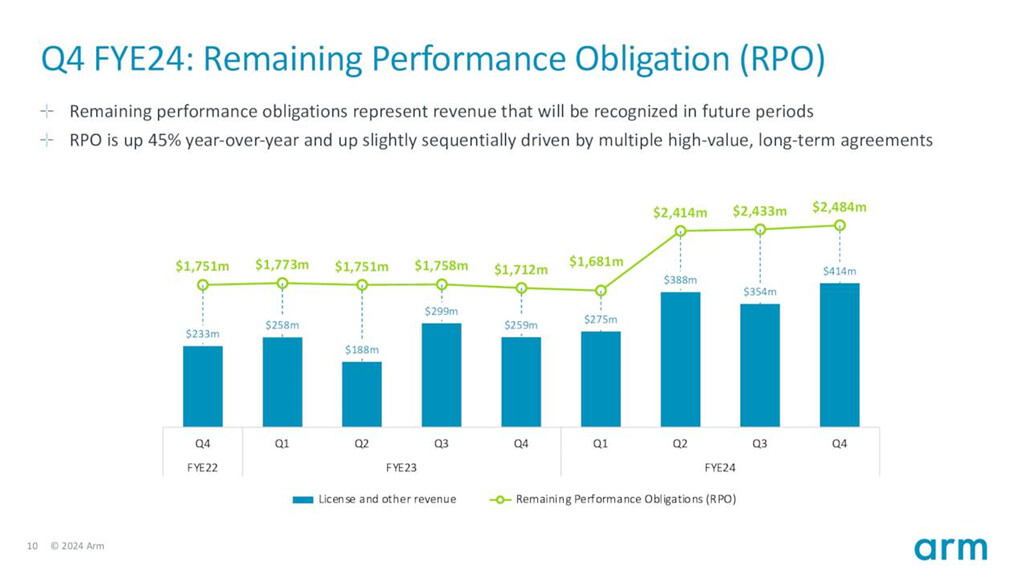

Also, the remaining performance obligations (RPO), which converts into revenue, remains strong throughout:

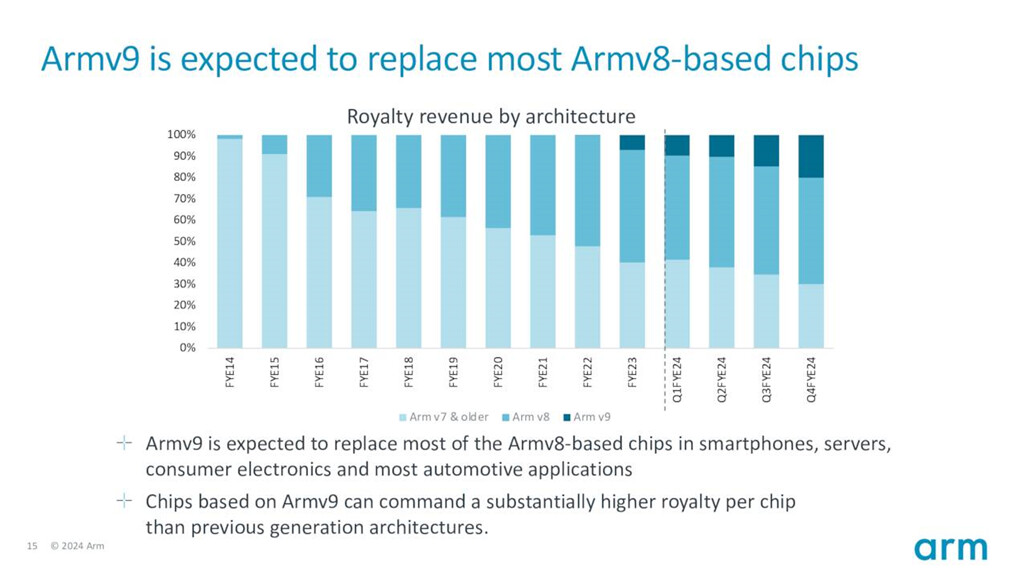

Arm states that Arm9 is built more intelligently from a royalty perspective than previous architectures. That is, Arm9, in my estimation, generates license fees, annual contract value (ACV), and royalties reflecting cash flow from the end-user side.

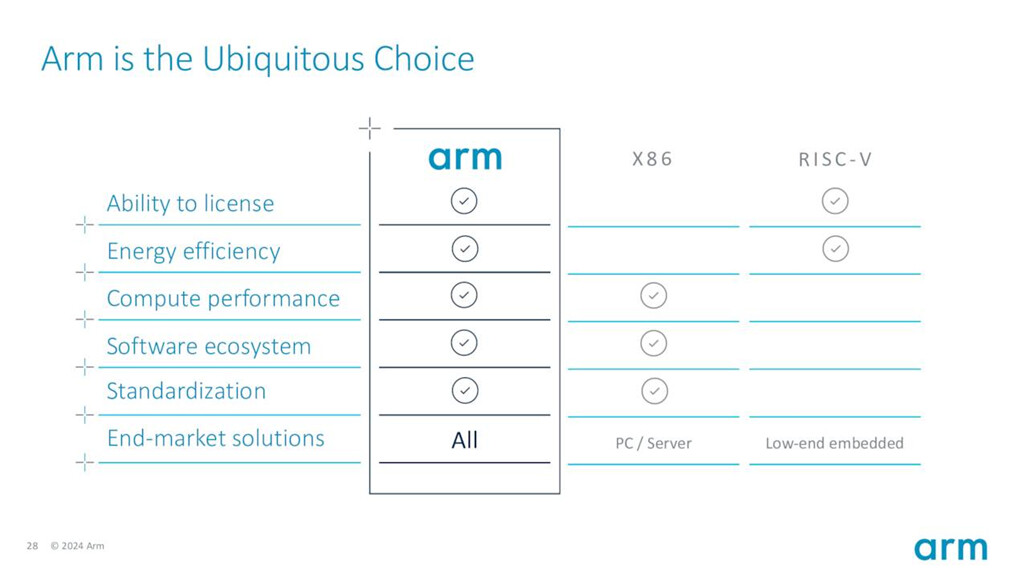

In the design of System-on-Chips (SoC), Arm’s CEO Haas boasts that they are the only player capable of delivering solutions for diverse and demanding CPU GPU AI LLM configurations:

“if you’re trying to develop an SoC that’s going to fit in the server and it needs to run Linux and it needs to run cis on Kubernetes, et cetera, et cetera, there’s really only one choice, ARM.

If you’re trying to build an SoC to run Windows, there’s only 1 choice, it’s ARM. If you’re trying to build an SoC to run Android or Gemini, there’s only 1 choice, it’s ARM. So the confidence we have in terms of licensing happening is extremely high.”

The following comparison made by Arm itself shows that with great confidence, Arm claims to be the solution architecture for all types of needs: evolving edge devices (mobile and PC), embedded systems (automotive and IoT), and AI/LLM data centers.

The company fits my investor profile because I have gradually become accustomed to living with volatile and highly valued companies. Today, too, we are coming down hard. Strong fundamentals come with a price; it is reflected in the stock’s high volatility. If I could only have 1 stock in my portfolio, it would be Arm.

slides here:

4f2fc46b-34a5-4bc5-94af-f13fbc348f0e (arm.com)

11 Likes

Well, now you’ve piqued my interest! Can you say what this means in practice? I read through this Wikipedia article, but I didn’t spot any information about that: ARM9 - Wikipedia

1 Like

Arm itself explains this in the slides I shared above. For example, from the second to last slide shown above:

“Armv9 is expected to replace most of the Armv8-based chips in smartphones, servers,

consumer electronics and most automotive applications”

“Chips based on Armv9 can command a substantially higher royalty per chip

than previous generation architectures”

My bull case is based on the fact that I recently shared a list of companies using the Arm architecture in this thread. It is an impressive list. In practice, almost all cloud companies will start generating steady license fees as Arm spreads to centralized cloud data centers (Amazon, Microsoft, Nvidia, Oracle, Google). The former is already a big deal. But Arm has a good monetization mechanism for when, for example, Qualcomm, as a strong mobile and IoT chip manufacturer, brings its Arm chips to AI phones, cars, and embedded systems. Royalties mean a few pennies per user. But apparently, Arm has designed the Armv9 architecture so that it can extend billing all the way to the end-user. In other words, AI and AI chips are being taken to the edge, i.e., to the user. Autonomous cars or robots cannot communicate with the cloud all the time; they must have a chip inside them that makes AI inferences.

So Arm is already a decent company as all the hyperscalers are building their own data center chips based on Arm. But I personally think that as a bonus, Arm will get exponential royalties later in the 2020s, as the Chinese and many others eagerly use AI in mobile phones and Windows PC devices containing Qualcomm’s Arm-based chips. If/when Arm gets royalties per user, small streams will become a river. And all this is on top of the license fees providing a steady income stream.

It’s worth browsing the slide set I shared earlier. And consider things in light of Arm’s customer base, which includes the world’s best chip and cloud companies.

8 Likes

A bit more detailed news regarding my previous story. There is a rumor circulating that Apple is nearing a deal with OpenAI to bring ChatGPT to Apple’s mobile phones. Below is a link to an article discussing the matter, from which I have highlighted one point:

“Apple will try to power some of its less intensive AI features using on-device processing, choosing to avoid sending data to the cloud wherever possible. There are a couple of good reasons to go that route, not least the fact that handling the processing of data on-device can make for a snappier experience. Performance is just part of the equation here, however, with Apple likely to tout the privacy implications of keeping a user’s data on their iPhone rather than using a cloud server to process it.”

So, Apple will be balancing which use cases are processed on the phone and to what extent the phone communicates with the cloud. That task requires strong chip design, i.e., System-on-a-chip (SoC) expertise. Apple uses the Arm architecture. Apple needs Arm licenses to design its own custom chips for these latest AI requirements. And then sometime in 2025, when Apple launches these “ChatGPT phones,” royalties will start flowing to Arm. I suspect the chips will be at the latest Armv9 level, for which Arm receives higher royalties than for older Arm solutions.

Apple’s nears deal to bring Open AI’s ChatGPT generative AI to IOS 18 (tweaktown.com)

7 Likes

No, they won’t.

Apple is a special case. It’s worth looking into the business relationship between Arm and Apple so that things don’t get out of hand with excessive bullishness. Apple accounts for less than 5% of Arm’s revenue.

Here’s one short piece, for example. You can find more on Google.

https://9to5mac.com/2023/11/29/apple-arm-licensing-revenue/

Apple was one of the founders of Arm and still owns a stake. And Arm doesn’t really have the leverage to change the deal because Apple is too important to lose. Arm already tried once, Tim Cook said “nope,” the whole thing fizzled out, and Arm settled for the current deal which, after the latest arm-wrestling, is valid until 2040.

5 Likes

Additionally, those new AI features will arrive with iOS 18, not just a new phone.

On the server side, however, they intend to use their own M2 chips.

Bloomberg had also suggested that Apple would turn to cloud-based processing for the more advanced AI features, however. To facilitate that, it’s believed that Apple will use its own chips to power the servers that handle its AI capabilities. More recently it’s been suggested that Apple will use M2 chips in its data centers, similar to those that are already used in the Mac Studio and Mac Pro.

To me, this indicates that they plan to run AI software on the phone’s standard chips and offload more intensive operations to the cloud, which uses a unified architecture.

3 Likes

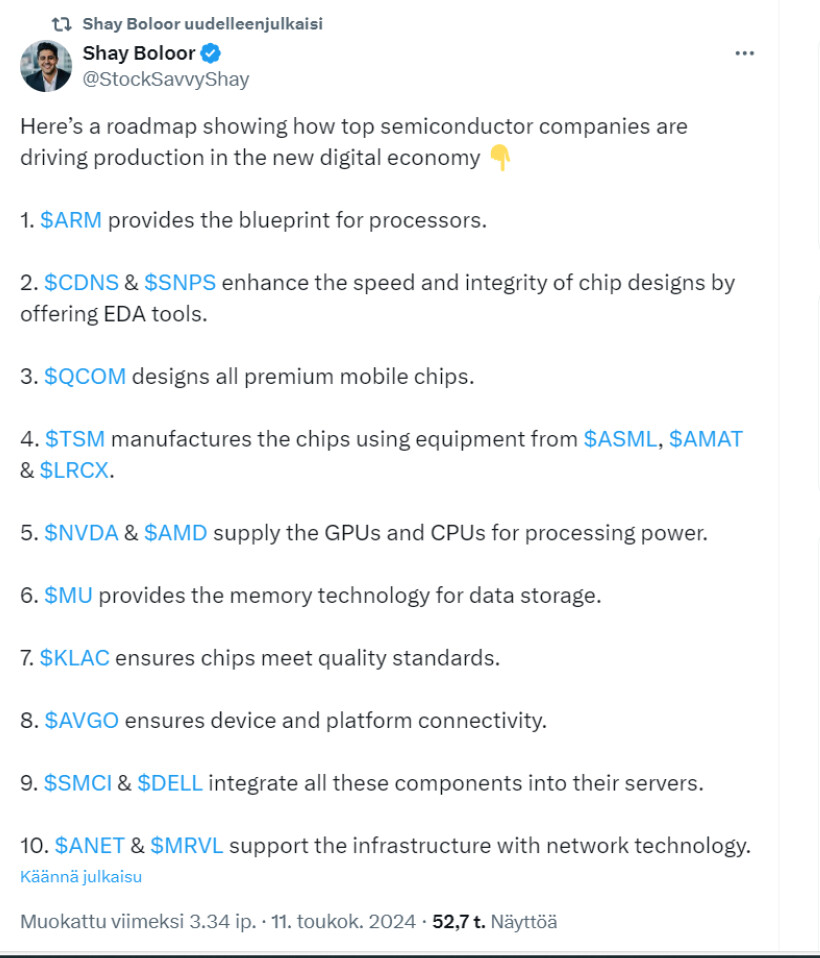

Let’s post this here as well:

A writer on X has gone to the trouble of mapping out the roles of semiconductor companies across the entire production chain. Not a bad breakdown, in my opinion. Anyone can use this as a framework for their own perspective.

5 Likes

Today we received SoftBank & Arm news, which I think bring quite a lot of new dynamics to the chip market (and more volatility to Arm’s valuation, making it an even tougher task)

I asked Copilot: is Arm starting AI chip manufacturing?

Answer: Yes, Arm Holdings is planning to start manufacturing AI chips. The company intends to set up a new AI chip unit and aims to have a prototype ready in spring 2025. Mass production is expected to begin in autumn 2025, and production will be handled by contract manufacturers12. Arm Holdings, known for supplying its architecture to chipmakers like Nvidia, is expanding into AI chips as part of SoftBank’s strategy to become a major player in AI technology34.

8 Likes

At COMPUTEX 2024, Jensen announced NVIDIA’s new Rubin architecture, the successor to Blackwell. The key point here is that NVIDIA continues to use the Arm architecture for CPUs in its platforms. This CPU is named Vera.

Excerpt from the keynote blog on Nvidia’s website:

More’s coming, with Huang revealing a roadmap for new semiconductors that will arrive on a one-year rhythm. Revealed for the first time, the Rubin platform will succeed the upcoming Blackwell platform, featuring new GPUs, a new Arm-based CPU — Vera — and advanced networking with NVLink 6, CX9 SuperNIC and the X1600 converged InfiniBand/Ethernet switch.

More about Rubin in the NVIDIA thread and, for example, here:

Nvidia Rubin revealed as Blackwell successor, powerful Vera CPU coming too | Tom’s Hardware (tomshardware.com)

5 Likes

You can find a pretty interesting story at that link and in the video behind it.

It’s about the fact that Arm isn’t just selling architecture (license and royalty income) but is designing Arm Compute Subsystems (CSS) for Client—a blueprint (concept) where the CPU and GPU can be designed directly down to the silicon chip, accelerating chip production lead times by about a year or so. Arm has mentioned these before. What’s new is CSS for Client, i.e., for mobile and PC. In addition, Arm announced the new Arm Kleidi software library to facilitate the development of AI and AI Computer Vision. So, CSS for Client and Arm Kleidi were new announcements, and the video stated that their outputs will be seen by customers in just a few months for CPU and GPU needs. Arm is really staking a claim on its future here. It is creating the tools that allow the likes of Apple, Microsoft Windows, and the Android world to get their future needs to market quickly, while Arm enjoys the base income from architecture licenses and royalties on top. So the company has a dual role: accelerating industry development with libraries and CSS systems, and getting customers into its own licensing ecosystem faster. There’s definitely an NVIDIA-style approach here. Especially if Arm also starts its own chip production.

9 Likes