Nice to see some good buzz in a quiet thread ![]() . I agree with many things, but I’ll write down my own thoughts.

. I agree with many things, but I’ll write down my own thoughts.

One big factor at Anora right now is the change in management. In October, it was announced that a new CEO (TJ) was being sought. I don’t believe Anora’s strategy will be greatly changed. Anora has a couple of large owners, and I assume the CEO (TJ) will be chosen to implement the strategy, not the other way around. A new CEO (TJ) is always a threat and an opportunity. Anora has a lot of cost base, and it’s easy to see that after lean years, someone who “streamlines” will be chosen to steer the ship, but the business’s greatest value lies in its brands and high-margin products, so a brand-growth-hype person who wants acquisitions and marketing might become the CEO.

Anora’s business is established, and it’s easy to think that the return expectation in the long run will largely consist of dividends. However:

https://anora.com/fi/sijoittajat/anora-sijoituskohteena

"Significant change in scale promotes productivity

We have a strong production and logistics footprint across the Nordics. Our industrial operations and supply chain are based on an integrated business model, which brings us economies of scale and improves capacity utilization. This leads to higher productivity, a smaller carbon footprint, and more responsible operations.

Growth opportunities in the Nordics and beyond

We have a strong drive for growth. Our industry is very stable and profitable, and our investments are small. This results in strong cash flow and a low debt-to-equity ratio. Our strong financial position and increased borrowing capacity give us good opportunities for growth both in the Nordics and beyond. Acquisitions play an important role in Anora’s growth strategy."

Investors like to play with SOTP (Sum-of-the-parts) calculations, and especially industrial buyers/private equity investors can realistically calculate that by buying company X and breaking it into parts, they would get Y amount of return. I don’t believe anyone is considering buying Anora, but rather the opposite. I would assume that Anora’s board and top management are repeatedly considering whether there are parts whose sale would be sensible or whether there are targets whose acquisition would be sensible.

Investors often look at companies quite hectically, but from a few years’ perspective, there has been

A merger into a larger scale about four years ago

https://anora.com/fi/sijoittajat/yhdistyminen

Three years ago, wines were bought for a large sum

https://anora.com/fi/anora-ostaa-globus-winen-tanskan-johtavan-viiniyhtion-vahvistaen-asemaansa-johtavana-pohjoismaisena-viinien-ja-vakevien-alkoholijuomien-talona-220620221030

Two years ago, cognacs were sold

https://anora.com/fi/sisapiiritieto-anora-myy-larsenin-konjakkiliiketoimintansa-international-beveragelle-060920231520

It must be remembered that most acquisitions fail!! ![]()

But Anora’s market value is “only” 220 MEUR. It doesn’t seem realistic to expect anyone to buy Anora or for the company to be broken up, but I would assume the value obtained from breaking it up would be more than Anora’s current price. But certainly, money could also be made for owners through other acquisitions; by divesting “something”, through mergers, or suitable acquisitions.

The markets for Anora’s individual operations are stable, but the market situation is constantly evolving.

When looking at Anora’s share pricing, it’s perfectly appropriate to reflect on analyst assumptions. Inderes is a good place to find data, and the latest forecasts are the best and most up-to-date, so for example, @YoungKaptah’s calculations are a good starting point in themselves.

BUT…

Analysts’ forecasts change over time. Inderes’ latest comprehensive report is a year and a month old. 13 months ago, Inderes suggested BUYING Anora with a target price of 5.5 euros.

The cash flow model stated that Anora’s enterprise value was 847 MEUR.

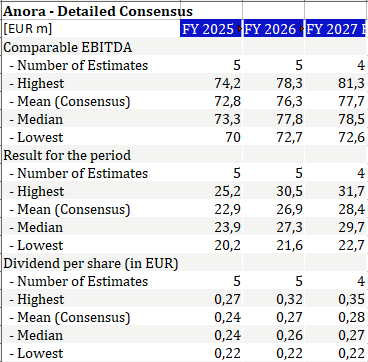

Anora’s consensus forecast has been updated after the earnings report. The update is so close to the earnings report that I would guess not all forecasts have been updated in this table. I must say I am very surprised that the forecasts are very close to each other:

If the forecasts were to materialize, Anora would pay ~0.26 € in dividends annually (now less and slightly increasing) reflecting the current share price of 3.26 €. This would give owners an 8% dividend yield, which is the historical stock market return over time.