Opening a thread to identify AI bottlenecks. The starting shot for AI development has been fired, and in my view, development isn’t stopping for years—it’s accelerating. In the post below from the “Pörssien suunta” (Market Direction) thread, I tried to outline these bottlenecks, so I recommend reading it first as a primer.

The market is massive and will offer investors extensive opportunities over the coming years, even if many might feel they’ve missed the best rallies. I can assure you that’s not the case; by diving deep into the value chain, various subcontracting chains start to emerge that the market hasn’t focused on yet. For example, outside the USA, there are vast investment targets where money hasn’t flowed yet. I believe every investor’s portfolio should include at least one stock or ETF related to AI value chains—the megatrend is that significant. My own watchlist now contains 220 “bottleneck stocks,” and additions are made daily.

I am not an expert on AI or bottlenecks, though I study the field daily and am an AI power user. A key reason for starting this thread is so that we could collectively, through swarm intelligence, find the winners of the coming years.

I fed Claude Opus 4.7 a massive amount of information/data regarding AI bottlenecks and am listing the first result directly here. The text hasn’t been edited at all and I translated it into Finnish, so there are some slightly funny expressions. Regardless, it should serve as an excellent starting point for the discussion:

Tier 1 Bottlenecks — Atoms and Substrates (Most Asymmetric Return Expectation)

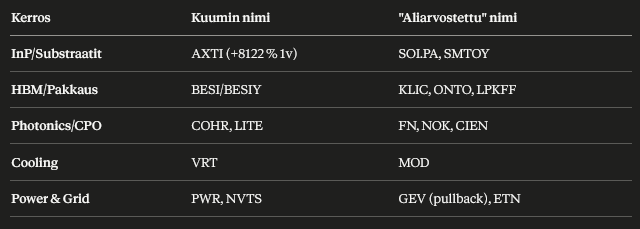

1. AXTI — Indium Phosphide Substrate The tightest bottleneck in the entire CPO supply chain. By 2026, global effective InP capacity will be 600–750 thousand wafers, with demand at 2.6–3.0 million — a gap of over 70%. AXTI controls 60–70% of the world’s InP substrate production through its Beijing facility. RS 86, and only -0.8% today — lagging behind the trend.

2. SMTOY / 5802.T (Sumitomo Electric) — InP + Japan Anchor One of the three global giants of InP substrates, and the only one operating purely in a Western alliance country. SMTOY +13.8% today, RS 77 — the market has started pricing this in. Another “ground floor” InP name to invest in alongside AXTI, providing diversification against geopolitical risk.

3. SOI.PA (Soitec) — SOI and Substrate expertise for RF front-end and photonics A quiet anchor for the silicon photonics wave. RS 78. This hasn’t taken off like AXTI yet; that’s the reason to look at it.

4. MP / LYC.AX — Raw Materials (Rare Earths) for magnets and generators Datacenter cooling motors, wind generators, EV traction — all need NdFeB magnets. Power & Grid theme +369% over 2y. MP RS 56, fading momentum figures, but this is a physical bottleneck name well past 2027. I consider this “late but essential.”

Tier 2 Bottlenecks — Wafers, Lithography, and Advanced Packaging

5. BESI.AS / BESIY — Hybrid Bonder Monopoly The Korean hybrid bonder market will grow to about $2 billion by 2028, and its share in the HBM4E era will rise to about 50% by 2028. Both Samsung and SK hynix are applying hybrid bonding in the 20-layer stack HBM5 generation. BESI and ASMPT are the two global hybrid bonder suppliers. This is the alpha bottleneck for the HBM5 era 2027–2028.

6. AEHR — Burn-in / SiC and Photonics Testing On the watchlist with RS 88, +6.75% today. A yield bottleneck for AI packaging and silicon photonics. A small name, but clearly institutional buy flow is underway.

7. KLIC (Kulicke & Soffa) — Thermo-Compression Bonding for 16-layer HBM4 The JEDEC revision (775 µm height limit clearance) kept traditional micro-bump technology alive for 16-layer HBM4, and Fluxless TCB has taken center stage before hybrid bonding. KLIC is the TCB leader. RS 85.

8. ONTO (Onto Innovation) + CAMT (Camtek) — Packaging Metrology Quality assurance for the HBM stack has become a key yield driver (metrology is a mandate in a world of $30,000 wafers where the cost of failure is existential for margins). Onto RS 68, Camtek RS 55 — both are below the hottest point, making them interesting while waiting for a catalyst.

9. LPKFF (LPKF Laser & Electronics) — Glass core packaging +7.2% today, RS 85. Glass core materials are the core of the 2027–2028 packaging trend (Intel, AMD, and Samsung are all investing). LPKFF is one of the narrowest pure-plays.

Tier 3 Bottlenecks — Optical Components (Highest Asymmetry)

10. COHR (Coherent) — EML Lasers, vertically integrated from InP substrate In March 2026, NVIDIA announced a $4 billion investment split between Coherent and Lumentum — Coherent revealed the collaboration expands NVIDIA’s access to five additional product families related to CPO. RS 83, T-17 days from earnings — one of the best risk/reward profiles on your watchlist right now.

11. LITE (Lumentum) — Same NVIDIA allocation as Coherent Lumentum is currently the only supplier shipping 200G-per-lane EMLs in volume — a critical component for next-gen 1.6T pluggable transceivers. RS 80. The EML supply deficit could reach 17% in 2026, and the shortage is expected to persist into the second half of 2027.

12. FN (Fabrinet) — The “TSMC” of Optical Assembly Almost all Nvidia/Coherent/Lumentum optics pass through Fabrinet’s factories in Thailand. RS 67 — below the peak, but this is a structural winner in all optics scenarios.

13. CIEN (Ciena) — Pluggable optics and DCI McKinsey estimates that 800G transceiver production could fall 40–60% short of demand by 2027, and the 1.6T supply deficit will be 30–40% until 2029. CIEN RS 87. A plug explosion before the CPO volume ramp in 2027+.

14. NOK (Nokia) — Photonics and optical IP via Infinera deal +11.7% today, RS 88. The market has started pricing a photonics option for Nokia. This is a “Finland bonus” where there is a clear optical bottleneck thesis but valuation is not yet overheated.

Tier 4 Bottlenecks — Power, Cooling, and the “Last Mile”

15. VRT (Vertiv) — Liquid Cooling Ecosystem A January 2026 Dell’Oro Group report stated the liquid cooling market nearly doubled in 2025, approaching $3 billion, and is forecasted to reach $7 billion by 2029. RS 86. Vertiv’s liquid cooling solutions are the final safety net for the HBM4 thermal redline.

16. MOD (Modine) — Midcap of Datacenter Cooling RS 76. The Cooling theme on your watchlist is +145% over 2y — Modine is an undervalued part of that basket compared to VRT and TT.

17. GEV (GE Vernova) — Gas Turbines and Grid Equipment Gas turbine OEM queues are ~80 GW in orders vs ~30 GW/year capacity, pushing CCGT deliveries into the next decade. Lead times for high-power transformers have stretched to as much as 5 years; before 2020, it was 24–30 months. GEV was today’s laggard (-0.9%) — an opportunity to enter on the next pullback cycle.

18. PWR (Quanta Services) — Power Transmission Construction RS 88. Datacenter grid buildout is a multi-year bottleneck, not a cyclical issue. 11 GW is in the “announced” phase without physical progress, and 25% of these projects haven’t revealed a power strategy at all. PWR is direct leverage to this.

19. ETN (Eaton) — Switchgear, busways, low/medium voltage RS 61, but modest valuation relative to growth. The stretching of transformer and switchgear lead times to 5 years makes Eaton a beneficiary of a multi-year demand pull.

20. NVTS (Navitas Semiconductor) — GaN for 800V HVDC Datacenter Architecture +10% today, RS 78. NVIDIA’s new datacenter architecture has catalyzed collaborations with TI, Navitas, Infineon, Innoscience, and onsemi to integrate GaN devices into 800V HVDC systems, and Yole Group predicts the first commercial implementations around 2027. Navitas is a pure-play GaN — small, but strategically important in the NVIDIA ecosystem.Finally, a summary. Claude included our Nokia in the Top 20 as an “undervalued” pick

and intentionally left out the so-called obvious memory manufacturers, such as MU and SNDK, as well as giants like Nvidia, AMD, and AVGO and the entire AI Cloud sector.

Summary of Claude’s picks: