Yay, some evening reading!![]()

@Antti_Jarvenpaa and @Thomas_Westerholm talked about Wetteri. ![]()

Yay, some evening reading!![]()

@Antti_Jarvenpaa and @Thomas_Westerholm talked about Wetteri. ![]()

Wetteri’s information is a bit off on Nordnet right now ![]()

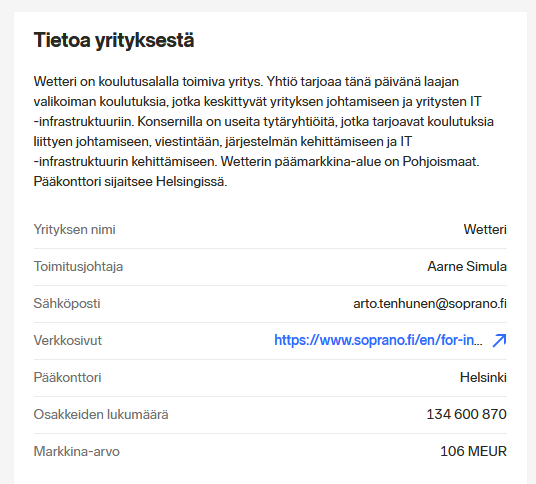

Edit. Or have I misunderstood something? That’s basically Soprano’s description, which is now Wetteri though ![]()

Here is Salkunrakentaja’s Jorma Erkkilä’s piece on Wetteri.

The listing took place through what is known as a reverse listing, in which the listed company Soprano, specializing in training, signed a conditional share exchange agreement at the beginning of June. In accordance with it, Soprano will purchase all shares of Themis Holding Oy, the parent company that fully owns the Wetteri Group.

Themis Holding was established for the purpose of the corporate restructuring and has no prior business operations. The main owners of the Wetteri Group and the active owners becoming investors in connection with the arrangement will own approximately 6/7, or about 86 percent, of the new corporate entity.

It seems the stock exchange bell was rung with buying pants on

Not just ready to buy, but some pretty massive growth targets have been set to go with it

Reaching Kamux’s current figures in three years ![]()

Inside information: Wetteri’s financial guidance for 2023 and 2024

Wetteri Oyj Inside Information 19.12.2022 at 9:45 am

Entrepreneur-led automotive growth company Wetteri announces its financial guidance for 2023 and 2024.

Wetteri Oyj financial guidance for 2023

Revenue 460 million euros

Adjusted operating profit 13 million euros

Wetteri Oyj financial guidance for 2024

Revenue 730 million euros

Adjusted operating profit 21 million euros

The company’s medium-term (3 years) target is to achieve a revenue of 1,000 million euros and an operating profit of 30 million euros.

Markku Kankaala, Chairman of the Board of Wetteri Oyj:

”Wetteri has a strong will and the capability to carry out several high-quality acquisitions in the near future. These enable our bold targets for the company’s growth. Industry consolidation has begun, and Wetteri is a pioneer in it.”

@Matias_Arola spoke about Wetteri’s recent acquisition, the company’s strong guidance, and its financial targets.

The fact is likely that Wetteri’s combined net profit for the last four fiscal years has been approximately 3.3 million euros, or less than 1 million euros per year.

Apparently, the current stock price is about 100 times the company’s earnings over the last four years.

If the company intends to grow its revenue through acquisitions paid for in cash or new shares, I don’t see such revenue growth having any significance for the company’s value.

The valuation has been driven quite high compared to the company’s size and earning capacity.

The current valuation level has little to do with the business and its earnings.

From Matias’s comments:

“Wetteri’s stock market pricing is currently driven by Simula Invest’s upcoming 0.82 euro tender offer for the former Soprano shares. As the special situation created by the tender offer ends, we still see clear downside potential in Wetteri’s valuation over the next 12 months.”

Wetteri’s forecasted growth figures are based on acquisitions. Will it be possible to execute these at sensible valuations in the future, when the stock’s valuation level—and consequently its use as a transaction currency—is driven by earnings performance after the tender offer?

Market consolidation has been ongoing for a long time; private-to-private trade is declining and shifting toward dealerships. Kamux and Saka are taking this market organically from smaller players, and if one wants to compete on equal footing, one way is to grow into the same size category through acquisitions. At Wetteri, profitability is positively impacted by maintenance operations compared to these peers.

If you want to grow aggressively, you have to get into Uusimaa, Pirkanmaa, and Southwest Finland, etc., in a BIG way.

The problem I see here is that in these market areas, there aren’t really any small players left to acquire.

Almost everything is already starting to be multi-brand dealerships and larger chains.

What does Wetteri have the muscle for, and which large car dealerships / chains are for sale?

At the same time, Hedin is on the lookout for acquisitions and they also want to grow big.

You can always grow by establishing new branches as well, but in a city where there are already long-standing dealerships for new brands, it’s difficult and expensive to win customers away from the old operators.

Then there are the upcoming agent models, which eat into profitability even further…

There was talk about the maintenance business being Wetteri’s competitive advantage.

Maintenance used to support car sales in generating profit, but as I understand it, it’s already the other way around.

Maintenance is a mandatory burden that comes with many new brands, which simply must be under the same roof.

Another thing is that as the car fleet becomes electrified, there will be even less to service in new cars in the future.

When people here talk about Saka and Kamux, asking why they don’t have maintenance operations? It’s precisely because those millions are better off invested in car sales. ![]()

Others are shopping too.

Today’s price is about 14% below the upcoming takeover bid. It is admittedly a peculiar situation for the stock, and it’s not made any clearer by the analyst’s sell recommendation, which is significantly below the offer price.

Is it the case that there is an arbitrage opportunity available here? Does the tender offer apply to all shares, meaning if you buy today, is the majority shareholder still obligated to redeem the shares at 82 cents under the upcoming tender offer in January?

That is how I have understood the situation, and it is also what the Inderes analyst writes in their report. Apparently, the confusion has been caused by the fact that the analyst is giving a “sell” recommendation and a €0.45 target price even though the tender offer will be €0.82.

It really does look quite strange, I wonder if something is being missed here? Then again, in previous days trading has been fairly close to that tender offer price, so maybe not. Maybe someone just wants the trades for this year’s taxes. ![]() Surely it’s not possible that only some of the shares being traded would be eligible to accept the offer.

Surely it’s not possible that only some of the shares being traded would be eligible to accept the offer.

@Thomas_Westerholm Could you clarify the situation regarding Simula Invest’s tender offer a bit? Are the Wetteri (ticker: WETTERI) shares currently purchased from the exchange covered by Simula Invest’s tender offer, which would naturally suggest that the current share price is at a relatively significant discount compared to the €0.82 tender offer price?

Or could it really be that both the old Soprano shares and the new Wetteri shares are mixed in there now, and only the old ones are covered by the tender offer… Since no lock-up is mentioned in the terms except for the major shareholders, meaning the smaller owners could sell their shares without restrictions already. That would at least explain the willingness to sell at these prices, and the caution among buyers if you can’t be sure when buying whether you’re getting the “right” shares. ![]() Who knows…

Who knows…

All shares of the same series certainly have the exact same rights. Or how would you separate the shares into two different classes when they are traded on one and the same marketplace?

My interpretation of the recent price behavior is uncertainty, resulting from the unclear communication in Inderes’ analysis, coupled with a €0.45 sell recommendation. Before that analysis, the share price was very close to the takeover bid level for several weeks, and at the same time, Inderes’ target was €0.82, matching the takeover bid level, as has been the custom in these types of situations.

A public tender offer is always for all minority shareholders and, by law, it cannot include any additional conditions.

It’s really strange that those former Soprano shares haven’t been designated as a separate share class, such as wetteri_new, which would make it easy to distinguish them from the original Wetteri shares. Alternatively, the original Wetteri shares should have a lock-up period for the duration of this tender offer; this might be the case, but there is no information easily available about it. Otherwise, I don’t see how these shares could be differentiated for the tender offer.

Is there any more detailed information on when the Simula Invest tender offer is expected to be completed?