https://keskustelut.inderes.fi/t/inderesin-kahvihuone-osa-9/50229/2471?u=sijoittaja-alokas

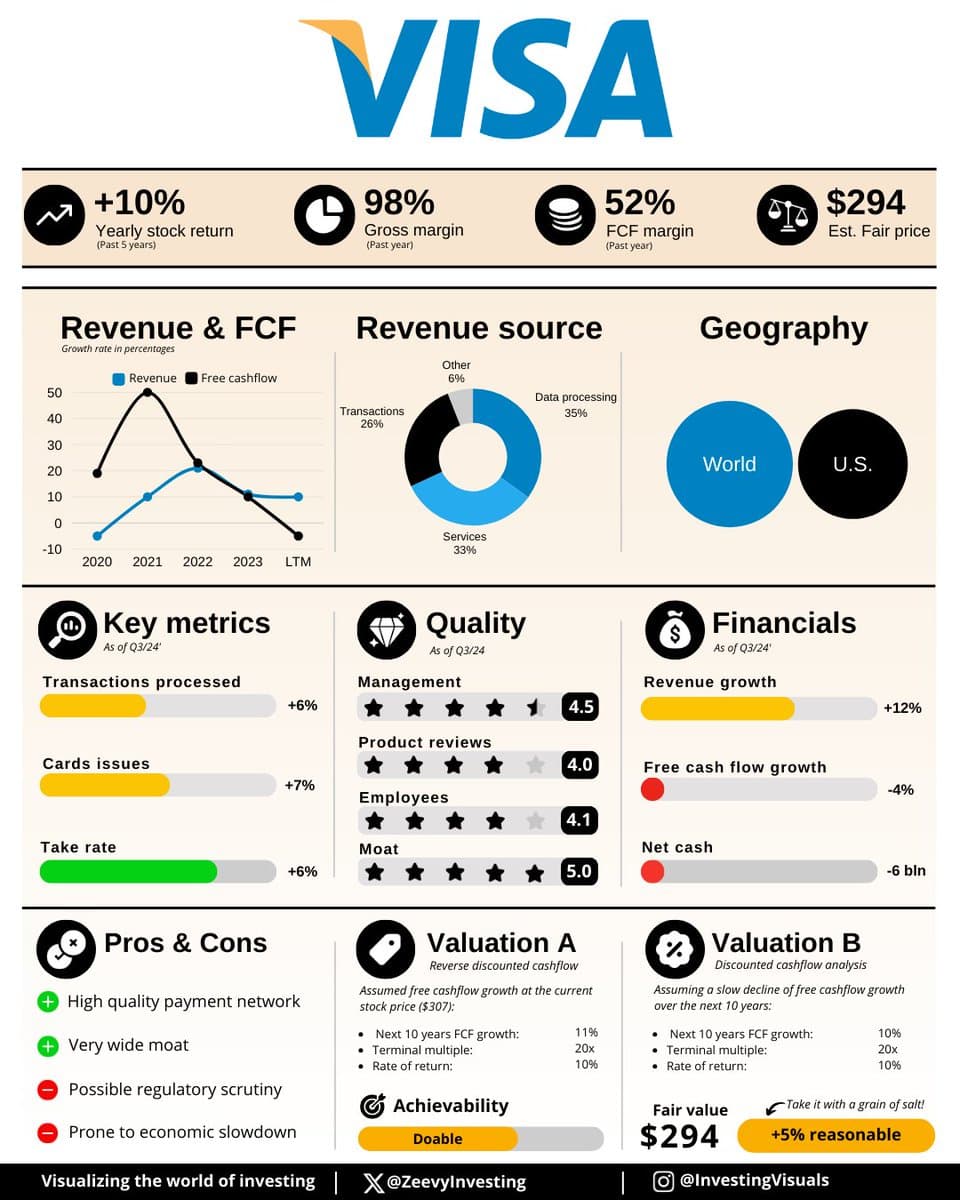

I tried to make a 3/5 thread opening, but it turned out 2/5. Sources: Visa’s own pages, X, Inderes, and a few investment sites. ![]() And I haven’t mentioned AI.

And I haven’t mentioned AI. ![]()

INITIAL CHATTER ABOUT VISA

Visa Inc. is an American multinational financial services corporation headquartered in California. Visa is one of the world’s most well-known payment card companies.

The Birth of the Visa Card

The story of the Visa credit card began back in 1958, when Bank of America launched a paper card called BankAmericard. This was the first general-purpose credit card with a revolving credit feature. At the time, credit cards were a completely new idea, and they allowed customers to make purchases without having to carry large amounts of cash.

In the 1970s, the card became international and combined the services of several banks into a single product. In 1976, the card was renamed Visa.

Development and Expansion

Visa released its first debit card as early as 1975. This allowed customers to make direct bank account payments, but it wasn’t until the 1990s that debit cards became significantly more common and became an important part of Visa’s operations.

Visa’s payment card product range has grown over the years. Today, it includes the online card Visa Electron, chip-based debit cards, and prepaid cards etc., which can be used as reloadable payment cards or gift cards. The company offers virtual cards for online payments, which have no physical card at all.

In 2013, there were a total of 2.1 billion Visa cards in the world, and they were accepted as a means of payment at approximately 24 million points of sale. In Finland, Visa cards entered the market in the early 1980s, when Luottokunta began issuing them through its member banks. Later, major banks like Osuuspankki, Nordea, S-Pankki, and Danske Bank were responsible for issuing the cards.

Current State and Future

In the 2000s, Visa brought a credit feature to its charge cards, and from the beginning of 2005, also actual Visa credit cards. This expansion allowed customers a more flexible way to manage their finances—or ruin them.

The company has continued to develop and innovate in payment methods, aiming to provide its customers with secure and efficient solutions across the world. The company’s goal is to stay at the forefront of technology and meet the needs of a changing world where digital payments and mobile technologies play an increasingly important role.

INVESTOR’S PERSPECTIVE

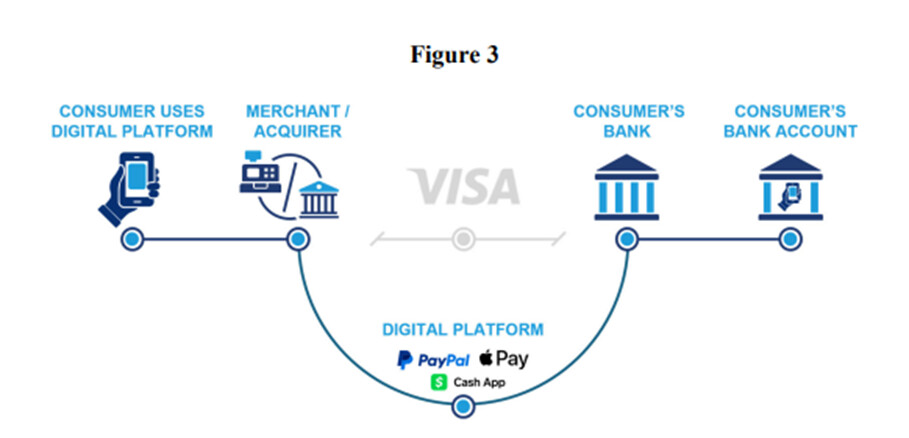

Visa acts primarily as a payment processor and is not a lender itself. At the heart of the company is VisaNet, which is a global payment processing system. This technology is an important part of Visa’s ability to maintain its position as a market leader and grow its customer base globally. Visa’s business model is divided into three main segments: consumer payments, new flows, and value-added services. Of these, consumer payments are the most significant and continue to grow as cash and check purchases shift to digital equivalent payments.

Visa benefits from significant economies of scale, which allow it to maintain higher margins compared to other competitors. Visa has also shown an ability to innovate and utilize technological solutions, such as collaborations with FinTech companies, which improves the company’s competitiveness. Additionally, Visa has made strategic acquisitions, such as Currencycloud and Tink, which have expanded its service offering.

Risks and Opportunities

While Visa enjoys a strong market position and particularly the brand recognition that comes with it, it faces risks such as a constantly changing regulatory environment and rapid technological development. Competition, especially with FinTech companies, can pose challenges but also offers collaboration opportunities.

Visa’s ability to maintain its brand value and innovate to stay at the forefront of development is crucial for the company’s long-term success. Visa is strategically well-positioned to take advantage of the global shift from cash to digital payments, which makes it interesting in the eyes of an investor.

Visa might be boring, but it’s familiar to everyone. The company is very profitable and isn’t perceived as being particularly risky.

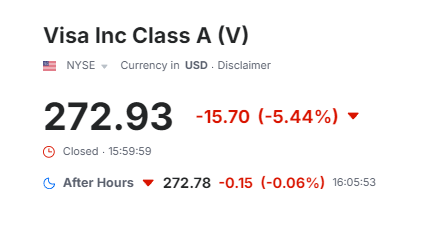

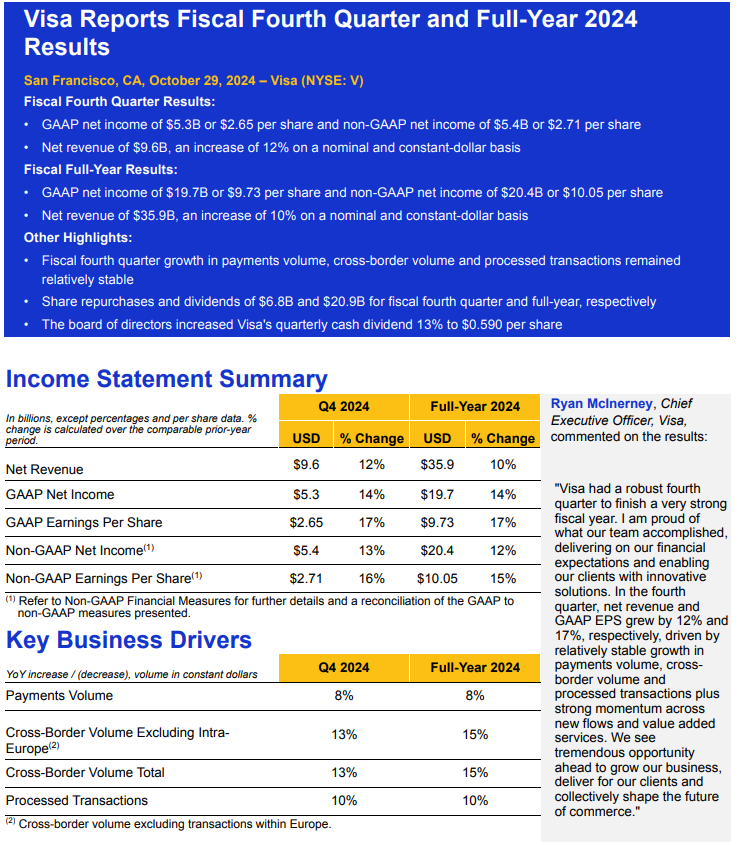

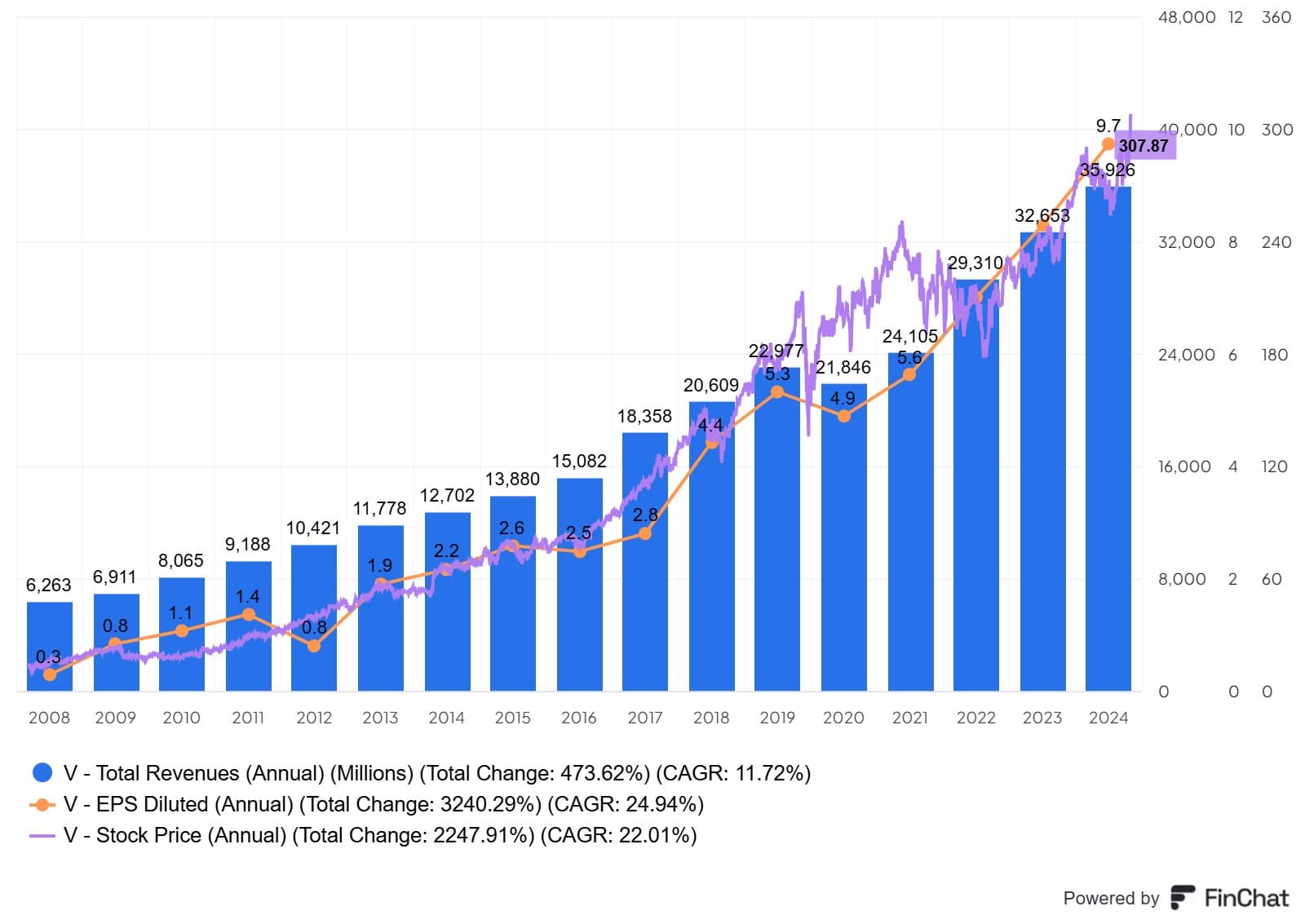

A few words about the recently published Q2:

The company reported that quarterly revenue fell short of forecasts. Visa announced third-quarter revenue of $8.9 billion, which was $60 million below the analyst average—so not by a huge amount… but this is rare for Visa, which last narrowly missed forecasts in 2020.

The company’s adjusted net income rose 9% to $4.9 billion, or $2.42 per share, while the forecast was $2.43. Global card usage grew by 4.9% and in the US, where Visa gets about 40% of its revenue, growth was 5.1%. The Fed is close to cutting interest rates, suggesting economic resilience.

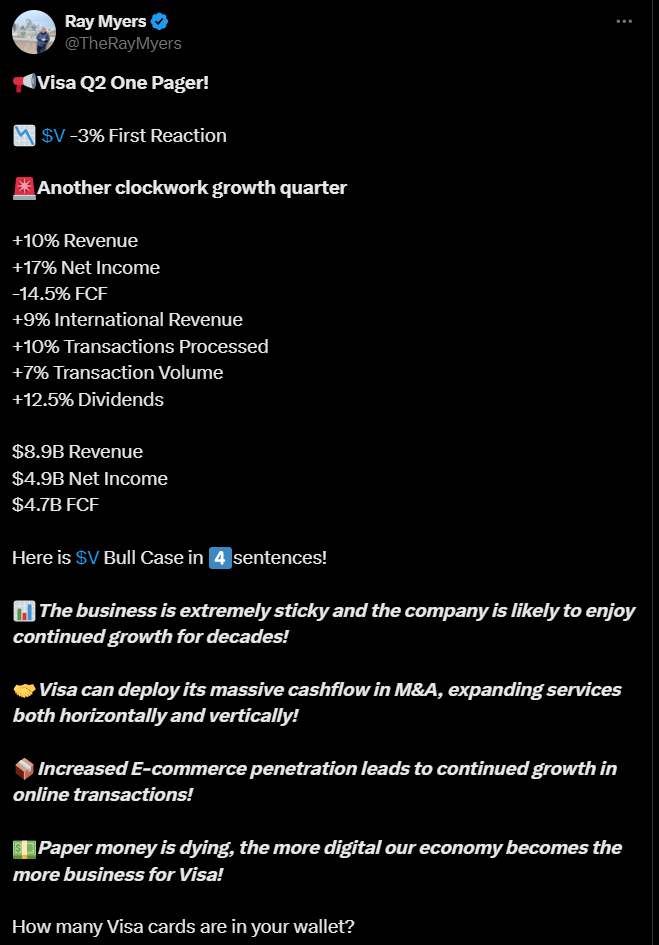

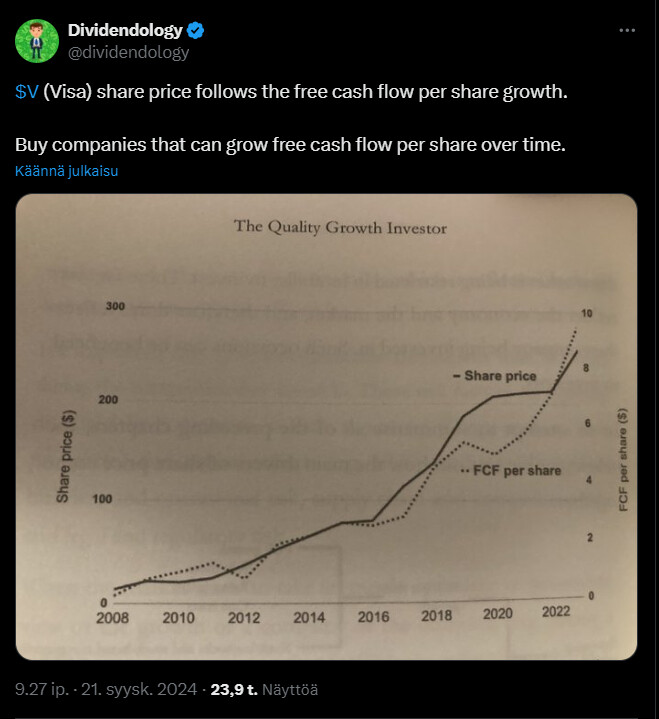

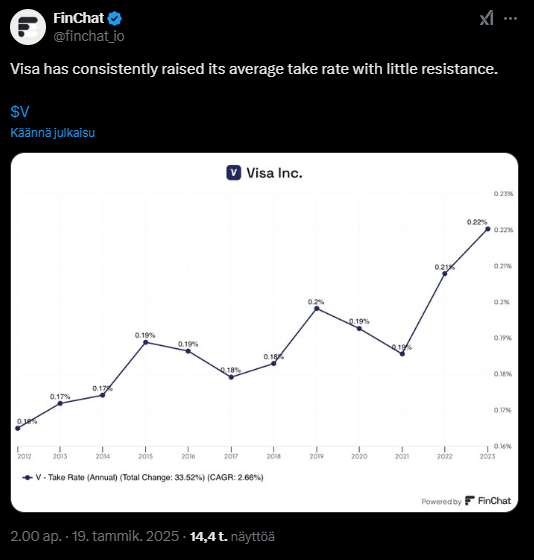

Here is a tweet about Q2 that explains everything better than I can. ![]()

https://x.com/TheRayMyers/status/1815858112525427065