An updated view will only be available tomorrow, but it’s nice if we can liven up the discussion, so I can throw out some scattered thoughts at this point. To my eyes, this is a very likeable company. Maintenance generates stable cash flow. Management seems reliable. There are units all over Finland (over 30), and they produce very varied results (these can be seen from their own financial statements). I like this entrepreneurial, decentralized management, because then the incentives in the units are in place, and the work of the installers is monitored closely. Some acquisitions have been more successful, and some a bit more subdued. Overall, however, the company has avoided major mistakes, and the share price has risen well from its lows, even though the market has not yet provided tailwinds.

Vilpon Olli has prepared a new company report after Viafin Service’s Q3 results. ![]()

Viafin Service’s Q3 revenue decreased by 0.7% from the comparison period to EUR 23.8 million, but it exceeded our forecast by EUR 1 million. Strong growth was achieved in the Maintenance segment, as its revenue increased by 15% from the comparison period to EUR 21.8 million. Approximately half of the growth was, in our estimation, due to the Karhu acquisition. Project business revenue, on the other hand, decreased by 60% to EUR 2.0 million due to strong comparison figures and profitability prioritizations made in project selections (i.e., increased price competition). The company’s Q3 operating profit of EUR 1.8 million was close to the comparison period (Q3’24: EUR 1.9 million) and also our own expectations (EUR 1.9 million).

Quoted from the report:

For H2 2026-2027, we expect project sales growth, in particular, to gradually accelerate with the recovering operating environment and the economic boost coming from the European investment wave. Through this, we forecast the company’s earnings to grow by an average of 10% per year between the last 12 months and 2027.

Will there be a comment from Olli soon regarding that relatively small acquisition? At a quick glance, the figures for Vaajakosken Sähkösepät Oy look quite strong.![]()

Here is the press release:

"Viafin Service Oyj (“Viafin Service”) is implementing its growth strategy and strengthening its electrical maintenance expertise by acquiring the business operations of Vaajakosken Sähkösepät Oy, which provides electrical maintenance primarily in Central Finland. As a result of the business acquisition, 9 employees will transfer to Viafin Service. Vaajakosken Sähkösepät Oy’s revenue in 2024 was EUR 867 thousand and EBITDA was EUR 193 thousand. The company’s business operations will become part of Viafin Service’s Central Finland operations under Viafin Industrial Service Keski-Suomi Oy.

Through the acquisition, Viafin Service expands its electrical maintenance expertise in the Central Finland region, offering its customers an even broader range of services. Vaajakosken Sähkösepät Oy’s strong expertise and good reputation in electrical maintenance excellently complement Viafin Service’s existing maintenance business in Central Finland.

”The business acquisition enables the expansion of Viafin Service’s service portfolio into electrical maintenance in line with its strategy, by leveraging Vaajakosken Sähkösepät Oy’s strong expertise and customer base. Combined with the expertise and customer relationships of Viafin Service’s local unit in Central Finland, this allows us to serve our current and new customers even more efficiently. We are excited to join forces and offer even more extensive services to our customers,” says Heikki Pesu, CEO of Viafin Service.

”Vaajakosken Sähkösepät Oy becoming part of the Viafin Service Group enables the growth of our current electrical maintenance and the development and implementation of value-added services for customers in a new way. I am convinced that our electrical maintenance expertise, combined with Viafin Service’s extensive network of locations and comprehensive maintenance business, creates a strong foundation for a growth path for the current electrical business in the Central Finland region,” comments Jouni Rahkonen, CEO of Vaajakosken Sähkösepät Oy.

Vaajakosken Sähkösepät Oy is a company founded in 2013 and 100% owned by Jouni Rahkonen. Today, Vaajakosken Sähkösepät’s business is based on strong expertise and excellent customer relationships in providing electrical maintenance services."

I only noticed this acquisition of Vaajakosken Sähkösepät Oy just now, as I was on vacation at the time of the original announcement, and as a press release, it somehow also slipped past the holiday coverage. Below are some thoughts on the deal, and we will also include this in the forecasts in connection with the Q4 report once the purchase price is known.

This is a small but strategically suitable bolt-on acquisition relative to the company’s size, which strengthens the company’s electrical maintenance expertise in Central Finland.

The revenue of the acquired business in 2024 was 867 thousand euros and the EBITDA was 193 thousand euros. In light of historical figures, the target’s profitability has been at an excellent level, as the EBITDA margin was approximately 22% in 2024. Although the acquisition target is small on the scale of Viafin Service (less than 1% of the group’s revenue), its profitability profile is healthy and supports the group’s profitability target.

The deal implements Viafin Service’s growth strategy, at the core of which is expanding the service offering and strengthening local expertise. The acquisition brings more electrical maintenance expertise to the company in the Central Finland region. 9 new people are joining now, and the company already had a team of about 100 people on the electrical side.

The transaction also shows that Viafin continues to actively screen for acquisition targets and utilizes its strong balance sheet to support growth.

Here are Olli’s preview comments ahead of Viafin’s results release on Monday, February 9. ![]()

We expect the company’s end of the year to have proceeded steadily overall, although weak demand in the Project business is weighing on group-level growth figures. However, strong momentum in the Maintenance business and completed acquisitions are filling the gap left by projects. The main interest in the report will be on the 2026 guidance and comments regarding the recovery of industrial investment activity, which we expect to be weighted towards the second half of the year. There might also be updates on the strategy side, as the previous strategy period has come to an end.

How does Inderes view the significant maintenance contract lost by Viafin Service’s subsidiary Viafin GAS Oy with Gasgrid Finland Oy? How does this affect the company’s stock valuation?

Is this public information and is there a source? Viafin’s report will be released tomorrow and the CEO will be interviewed, so I can ask for more details on the matter.

When the contract was won, it was announced separately and we commented on it earlier like this: Viafinille merkittävä sopimus kaasun siirtoalustan kunnossapitopalveluiden toimittamisesta - Inderes

Peculiarly, a flagging notification from Viafin is almost two years late. I wonder if there will ever be consequences for these MAR violations, or is the FIN-FSA (fiva) just focused on eating pastries? At least there probably won’t be any major fines for Viafin from this.

The companies that participated in the tender have been notified, and the appeal period has likely also ended. Another operator is expected to take over maintenance.

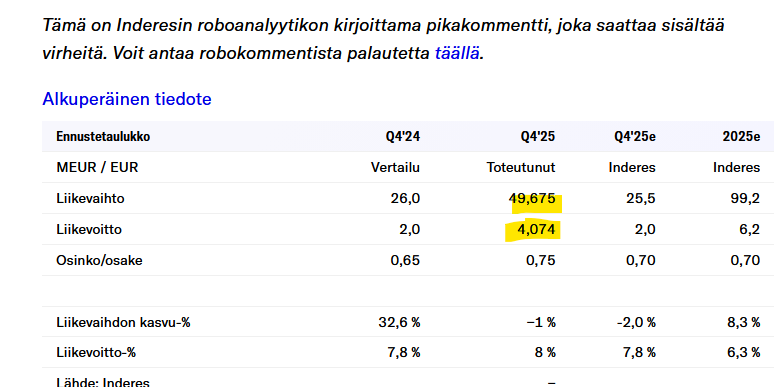

As the headline suggests, the entire year was a record-breaking one for Viafin.

Cash assets of around three euros per share. Dividend proposal EUR 0.75.

Targets are also kept unchanged according to a separate release.

Guidance anticipates a similar year ahead:

We estimate net sales for the 2026 financial year to be EUR 90–100 million and the operating profit (EBIT) for the financial year to be EUR 5.8–7.4 million.

Still need to watch Heikki Pesu’s interview, and then the Viafin investor can go back to sleep for another six months. ![]()

Regardless, expectations were exceeded.

Q4/2025 revenue decreased -1%. Hardly any organic growth for this company. All growth through acquisitions. Reflects Finland’s economic situation and stagnation (Stagflation) well.

I asked management about this this morning, and indeed, the winner of the tender has not yet been officially announced, so there is no more specific information available yet. I did manage to gather that the portion Viafin lost in the tender was relatively small and not even of a scale that would warrant a press release. Regarding the previous release from 2021 mentioning 13 MEUR over 4 years, that was not this entire package but only a part of it.

Here is also a fresh video from today ![]()

![]()

2025 went well for Viafin. There’s also a nice increase coming to the dividend.

Yes. ![]()

Investing in Viafin is wonderfully meditative and sleepy. ![]()

A peaceful oasis in a hectic world.

Here is an updated report Viafin Services Q4'25: Nautitaan rahavirrasta, kun 2026 kasvu on kiven alla - Inderes

It would be quite interesting to hear if @Olli_Vilppo has any insight and/or information on how Viafin might operate in the future and be part of the data center lifecycle → especially from a maintenance perspective. This could also be asked in the next interview!

As the latest Portfolio Review episode reveals, Viafin Service has made its way into @Verneri_Pulkkinen’s portfolio as the fifth-largest position. At 45:37, there’s talk about Viafin and how pleasant it is to own the company. ![]()