Well then, I didn’t guess/notice that EPS is in euros; I assumed it was in SEK, just like the target price.

1 Like

Bumping the thread:

Verve, … announced a streamlining of its organizational framework and the accelerated implementation of AI-driven automation to increase agility, enhance operating leverage, and align its cost structure with its primary growth drivers.

As part of this reorganization, Verve is addressing a historical personnel over-representation in Europe resulting from its M&A history, whereas acquired European businesses have seen their primary growth in the U.S. By reducing its German footprint - including headcount reductions and the closure of selective office locations - Verve is aligning its cost base more closely with its revenue profile and growth potential and deploys its commercial resources where they generate the highest impact.

A core element of the organizational streamlining is the accelerated and broad implementation of Artificial Intelligence across all of its internal workflows. By embedding AI-driven automation deeper into its operational processes, the Company expects - based on first very promising outcomes - to achieve unprecedented levels of product and platform development as well as scalability. Consequently, Verve expects to be able to further scale its operations without having to add significant additional resources in the medium term.

For the fiscal year 2026 and based on the organizational optimization, Verve anticipates cost savings of approximately EUR 1.5 million, taking into account one-off restructuring costs, with effects materializing from the second quarter onwards. On an annualized basis, these measures are expected to reach approximately EUR 5 million of annual savings from 2027 onwards.

Demonstrating its commitment to market proximity and strategic growth, Verve has appointed ad-tech veteran David Simon as President of Verve Marketplace and Chief Revenue Officer of Verve Group.

Things are moving forward and efficiency measures continue. It makes a lot of sense to review personnel locations after acquisitions, especially if revenue growth is happening entirely elsewhere. It sounds good if €5 million in savings are achieved in 2027 through these measures, provided there are no other negative impacts.

9 Likes

Here is a new pre-report on Verve from Christoffer, as the company publishes its Q1 report on May 27th. ![]()

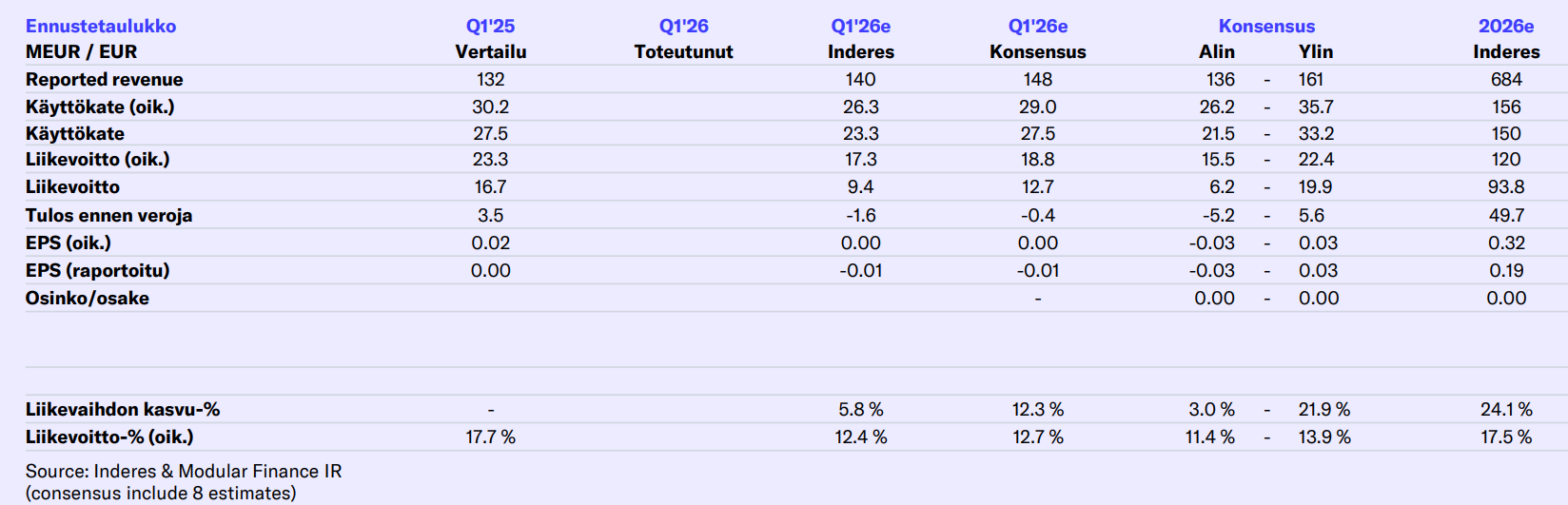

We expect the report to reflect a seasonally softer start to the year, further dampened by currency headwinds, front-loaded sales force investments, and the continued impact of a major customer loss from late 2025. In the near term, we are monitoring two things: whether the company can stabilize cash conversion by expanding its securitization program and when sales productivity will turn around. Ahead of the Q1 report, we have adjusted our forecasts to reflect a more cautious Q1 outlook, a lower IFRS 15 revenue recognition impact, and H1-weighted one-off costs, while keeping our full-year view largely unchanged. As such, we reiterate our Accumulate recommendation and leave our target price unchanged at 18 SEK.

4 Likes

Here are the latest comments from Christoffer regarding Verve’s latest announcement ![]()

Verve Group announced today its retail media offering, creating a closed-loop system between mobile advertising and in-store purchases in Germany. While we view this as a logical and strategically sound expansion that leverages the point-of-sale capabilities acquired through Acardo in late 2024, we remain cautious about its near-term impact on earnings. Management has explicitly stated that the current 2026 guidance does not include any impact from this expansion, except for the modest growth already expected from the 2025 acquisitions. However, the guidance remains unchanged. Therefore, the announcement does not lead to immediate changes in our forecasts.

8 Likes

So this result has finally arrived:

Comments by the CEO

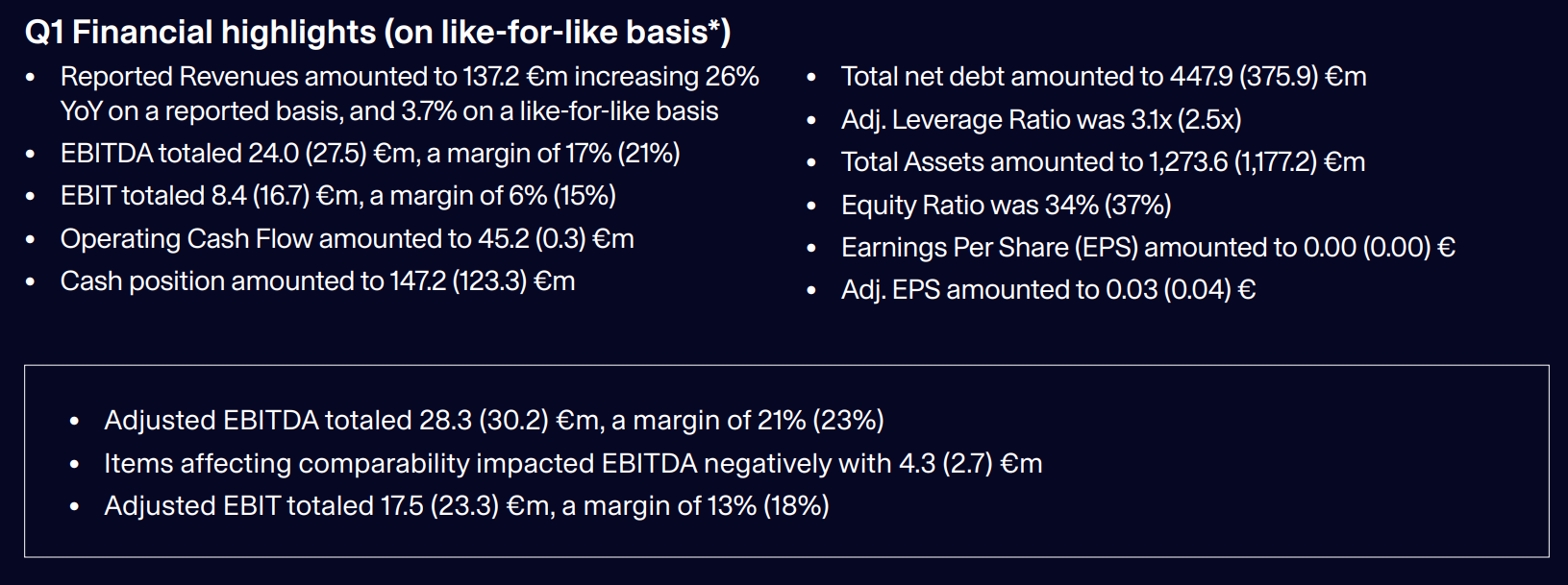

On a like-for-like basis, revenue increased to 137.2 €m. Organic growth was strong at 6.4 percent, and the inorganic contribution from recent acquisitions was even slightly higher. This shows that the underlying business continues to move forward. At the same time, we had to absorb a negative currency effect of almost 10 percent from the weaker US dollar.

What matters most to me is that the quality of our revenue and platform economics continued to improve. Gross margin rose to 41 percent, clearly above the prior-year level

Adjusted EBITDA of 28 €m was lower year-on-year. This development, however, does not reflect a weaker business model, it reflects a deliberate investment phase that we had already communicated in our outlook. We are investing in the areas where we see the strongest medium-term growth potential, particularly in our global sales team, where we planned additional investments of 10 €m in 2026. These costs start immediately, while new sales talent typically needs 9 to 15 months to reach full productivity. In other words: The first half of 2026 carries part of the cost of growth that we expect to translate into revenues later in the year.

Cash flow improved significantly compared with the prioryear quarter, supported by solid operating performance and more effective use of our securitization capacity. A lower utilization of securitization in the fourth quarter furthermore resulted in a delayed conversion of customer receivables into cash. Consequently, these inflows shifted into the first quarter, bolstering Q1 operating cash flow instead of being realized in Q4. At the same time, the balance sheet remains positioned to support the next phase of growth. Net debt was virtually unchanged from year-end, while cash and cash equivalents increased significantly. This gives us the flexibility to continue investing while keeping a clear focus on leverage and cash generation.

Financial Guidance 2026

The Company expects revenue for fiscal year 2026 in a range of 680 – 730 €m and adjusted EBITDA in a range of 145 – 175 €m.

At a quick glance, there’s a lot of good here and money is coming in. Guidance was maintained, with confidence in H2 strength.

26 Likes

Since a very large part of our revenue is invoiced in USD while we report in euros, this remains a visible factor in our reported numbers and is one reason why we aim to

adopt USD reporting by 1 January 2027, subject to AGM approval of the planned relocation to Ireland.Board proposes to relocate registered office to Ireland aligning corporate structure with international and US peers

The intention to relocate the registered office from Sweden

to Ireland was announced during the quarter, marking an

important strategic step in further aligning Verve’s corporate

structure with internationally recognized and US-listed

peers. The proposed relocation is expected to simplify

access to international capital markets and strengthen the

company’s long-term strategic flexibility. In addition, the

relocation would enable the possibility of a potential future

direct US listing. Management highlighted that Ireland

offers a highly established corporate and legal framework

widely used by leading global technology and advertising

companies. The proposal remains subject to shareholder

approvals at 2026 Annual General Meeting.

The intention is to start reporting in USD as of 1 January 2027; I hadn’t noticed this myself before. And it enables a direct US listing.

Unification of Jun Group and Captify US under Verve For Advertisers

In January Verve announced the unification of Jun Group

and Captify US under the brand Verve for advertisers,

marking an important milestone in the company’s strategy

to simplify its market positioning and strengthen its offering

for brands and agencies. By consolidating its demand-side

activities under a single commercial identity, Verve enhances

operational efficiency and reinforces Verve’s positioning as a

scaled alternative in the privacy-first advertising ecosystem.

The rebranding reflects the company’s long-term objective

of deepening direct relationships with global advertisers and

agency partners while leveraging its differentiated data and

AI-driven targeting capabilities.

It feels like the train is chugging along quite well on this front too. Guidance was maintained, and Inderes is currently pretty much at the lower end of the forecasts.

Cash flow growth is explained:

Cash flow improved significantly compared with the prior-

year quarter, supported by solid operating performance

and more effective use of our securitization capacity.

A lower utilization of securitization in the fourth quarter

furthermore resulted in a delayed conversion of customer

receivables into cash. Consequently, these inflows shifted

into the first quarter, bolstering Q1 operating cash flow in-

stead of being realized in Q4. At the same time, the balance

sheet remains positioned to support the next phase of

growth. Net debt was virtually unchanged from year-end,

while cash and cash equivalents increased significantly.

This gives us the flexibility to continue investing while keeping

a clear focus on leverage and cash generation.

Cash balances amounted to 147.2 (123.3) €m.

Net Debt as of the end of the first quarter amounted to 447.9 (375.9) €m.

5 Likes

Cristoffer also wrote a quick comment, and it seems our thoughts are pretty much aligned. Based on the report, things are moving in the right direction, just as the headline suggests.

This was definitely a good report for the company during a quiet quarter. The company surely has strong confidence in the upcoming major global events and the momentum of the advertising market there.

The market didn’t seem to like this report at the opening, so there was enough weakness to be found, or expectations were simply higher.

8 Likes

A satisfactory report, at the very least. Other lines apparently missed forecasts slightly, but EPS beat expectations and there were no negative line items? Cash flow was good, though likely included some “one-offs” given how high it is compared to the profit lines. The amount of debt did not rise significantly from the end of 2025 levels.

This is a good place to continue towards a better rest of the year. I assume the upcoming US midterm elections will be fairly intense, so election advertising should provide good support for the business, even if it isn’t as strong a boost as presidential election years.

And the markets never seem to like anything Verve puts out ![]()

8 Likes

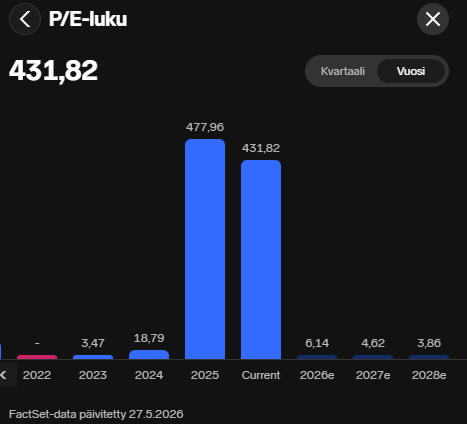

In my opinion, this image makes it quite clear that the market either does not trust:

- Analysts’ earnings forecasts

- The realization of cash flows consistent with those earnings forecasts in the near future.

It would be quite humorous if, in 2027, Verve were trading at a trailing P/E of 6-ish while the coffers were ringing in sync with earnings (cash flow conversion ~100%) and earnings simultaneously continued their annual growth.

12 Likes

@christoffer.jennel Will you be arranging a video interview with the CEO?

5 Likes

New report

Yesterday the share price went on quite a roller coaster ride and eventually closed at a much higher level.

Has the rubber band been stretched tight enough to the downside and the bottom been seen? Of course, if there is a larger market correction, this outfit is certainly not immune to it ![]()

At least my own faith in the company’s direction was strengthened. Waiting for the CEO interview? @christoffer.jennel

6 Likes

@Putti @Gwertheney Hopefully we can make it happen this time as well! The last two interviews took place a couple of weeks after the report, and it would likely be the same this time around. But I will keep you updated on that front, and if the interview happens, I will turn to you here in the forum to see if you have any questions ![]()

21 Likes

Hi everyone! I have now received confirmation that there will be a new interview with Remco in just over two weeks. If you have any questions, please feel free to ask them here by replying to this post. Please send these no later than Friday, June 19th. I will try to include as many questions as possible in the interview.

19 Likes

On recent CEO acquisitions:

You’ve been adding to an already large position. Buying the stock, what were you underwriting — a re-rating of today’s depressed multiple, or the H2 2026 earnings acceleration actually landing? At what point do you personally consider the stock cheap, and on what metric?"

On leverage:

Net leverage is 3.1x against your own 1.5–2.5x target, and you’ve tapped the bond market rather than deleveraging. What’s the realistic path back inside the range — is it EBITDA growth or actual debt reduction — and under what conditions would you use the €147m cash balance to buy back bonds at a discount versus fund more M&A?

You now have over 45 M€ quarterly operating cash from Q4, will you prioritize aggressive debt paydown, or do you intend to conserve cash for another acquisition round?

Do you have a rough timeline when could we see leverage levels on your target level?

On sales organisation growth

You’ve grown the sales significantly and this is given as one of the reasons the Operating cash flow before working capital dropped by nearly half in Q1

-

What early productivity signals can you point to today (bookings, pipeline, or revenue per rep, etc) that tell you the first wave is tracking toward full productivity on schedule rather than slower?

-

what’s your retention and attrition rate on those new hires, since a 9-to-15-month ramp only pays off if they stay? If a meaningful share of the hires leave before they’re productive, you’ve absorbed the cost without the return

11 Likes

Regarding point one, we won’t get a definitive stance with 100% certainty, but the question could be phrased in a “QT-style” (those who know, know): Do you sleep well at night with such a large stake in the company (around 25%)?

Consumer confidence seems to have been pretty much at rock bottom based on various surveys and such, but at the same time, the economy and employment (outside of Finland) are doing quite well despite the rise in oil prices. Has Verve noticed any major impacts on its business from the Iran crisis yet? (ad volumes/prices, customer bankruptcies, or anything else). This crisis has been talked about for months now, so one would think weaknesses would start showing if they were going to appear?

How has Verve prepared for a potential renewed rise in interest rates?

7 Likes

-In 2025, the biggest disappointment was the weakness of the cash flow, and the market still seems to doubt Verve’s ability to convert earnings into cash flow. If you look at 2027 or 2028 in a normalized situation without exceptional working capital movements, acquisitions, or other one-off factors, what do you see as Verve’s sustainable cash conversion relative to EBITDA, and why?

-If you were an outside investor in Verve and not the CEO, which 3–5 metrics or trends would you monitor most closely over the next 12–24 months to evaluate whether Verve’s long-term investment thesis is materializing?

-You have repeatedly bought more Verve shares, even though the market has been very skeptical. Regarding value, what is the most important thing you believe you understand about the company today better than the average investor, and which you believe the market will only realize in a few years?

12 Likes

- Will the new AI solutions improve pricing power with customers—meaning, can a higher price be justified by a higher-quality product, or will the price remain the same with the customer simply receiving better service?

- How much incremental revenue does the company expect to generate from the 2026 FIFA World Cup, and how has this been factored into the 2026 guidance?

- Once the integration carried out last year is complete, what will organic growth look like in 2026?

3 Likes

When the Jun Group acquisition was announced in 2024, management guided to around €170 million of pro forma adjusted EBITDA for 2025, including synergies.

Since then, 2025 was described as a transition year with major integration work, and the company also completed the acquisitions of Acardo, Captify, and Viewento while delivering modest organic growth.

Given all these initiatives, why is the 2026 adjusted EBITDA outlook still around €145–175 million? Were the original synergy assumptions too optimistic, or have unexpected headwinds offset the benefits? In particular, the lower EBITDA outlook does not appear to be explained solely by the additional investments in sales hires, so what are the main factors driving the gap versus the original expectations?

13 Likes

It occurred to me that I came across this news earlier, as there has been talk here about how the 2024 US elections were a positive earnings driver:

11 Likes