I think Veoneer, a Swedish company that produces safety technology for passenger cars, deserves its own thread. The company has many similarities to SmartEye, which has generated a lot of interest.

Veoneer produces advanced driver-assistance systems (ADAS), which are electronics and software that reduce human errors. This includes various lane keeping assist systems, automatic emergency braking systems that prevent collisions, and signals that warn or guide the driver. News in recent years suggests that fully self-driving cars are still many years away. This increases the demand for ADAS systems.

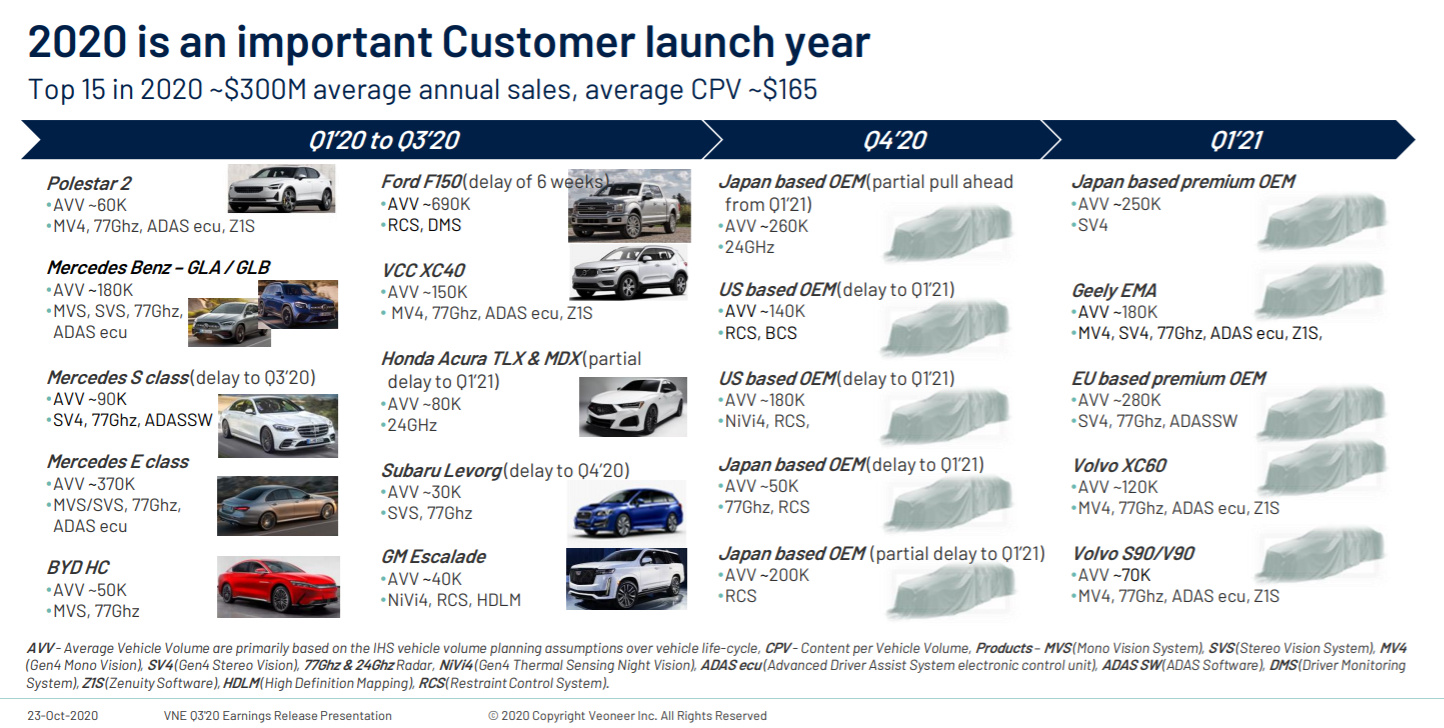

Veoneer has won several “design wins,” similar to SmartEye. Both companies are well-positioned to benefit from the growing demand for automotive safety technologies. Handelsbank estimates Veoneer’s order book at USD 13.5 billion, which promises strong growth for many years to come, considering that this year’s revenue level is about USD 1.3 billion.

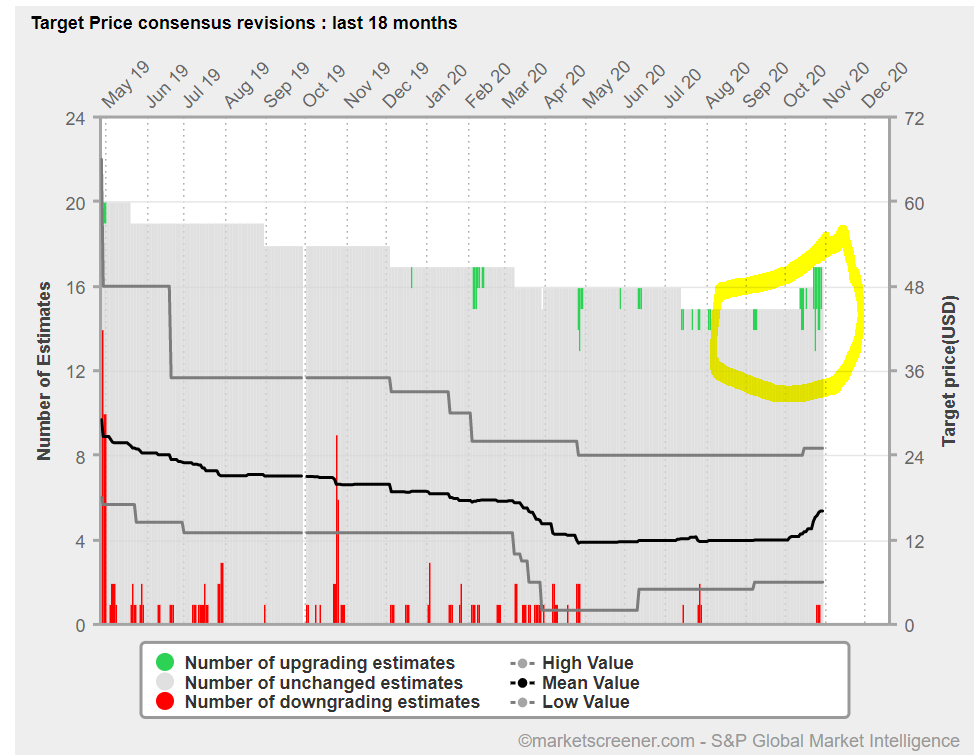

However, the company is priced more like a traditional automotive subcontractor than a growing technology company. Currently, EV/sales 2020e is 1.0. This year, revenue will decrease due to business divestments and the coronavirus crisis, but from next year onwards, growth is expected to be well over 20% per year. Handelsbanken’s analysts give a DCF value of USD 49 per share. The company is still unprofitable, but at the turn of the year, it had 699 million in cash, and according to management, the cash is sufficient to implement the company’s strategy.

During the summer, Veoneer announced a cooperation agreement with Qualcomm. Based on this cooperation, Handelsbanken’s analysts believe Veoneer will compete on equal terms with Intel and MobilEye. The fact that Qualcomm chose Veoneer as its partner validates the company’s position and technology.

I see this as an attractive opportunity to get involved in a growing technology company with a very moderate valuation.

Here you can find the company’s company preset and other additional information: