Let’s also put one of my favorites here, namely BPC Instruments.

BPC develops, manufactures, and sells measurement and analysis instruments for both industrial customers and research use. The instruments increasingly replace time-consuming manual work where raw materials are analyzed in biogas production. Previously, customers didn’t have precise information about what material was being put into the process, resulting in poor efficiency. In Europe, biogas production is expected to grow at a 32% CAGR until 2030. Additionally, BPC has made strides in the US and Asia; for example, India has become a significant market for BPC alongside China.

The company went public in late 2021. At the time, the IPO prospectus spoke of attractive opportunities to expand business beyond the biogas industry. We’ve seen evidence of this recently. For instance, BPC Blue was launched last year, which can be used to analyze the biodegradability of plastic materials. Other industries worth mentioning include wastewater analysis.

BPC was founded in 2005 by Jing Liu (CEO), Gustaf Olsson (Chairman of the Board), and Kristofer Cook (Board Member). Jing owns 65% of the company, while the other two have 12% and 5% ownership.

Jing is the only one among them who is currently active in operations. In fact, he plays a very significant role at BPC. At the end of 2023, the company had only 12 employees, and when I visited their office in Lund, Sweden last April, it felt like he was responsible for everything. R&D, sales, marketing, Chinese contacts, etc. What would happen to the company if Jing, for one reason or another, was no longer in the picture…? Perhaps from a shareholder’s perspective, a bodyguard by his side might be appropriate? ![]()

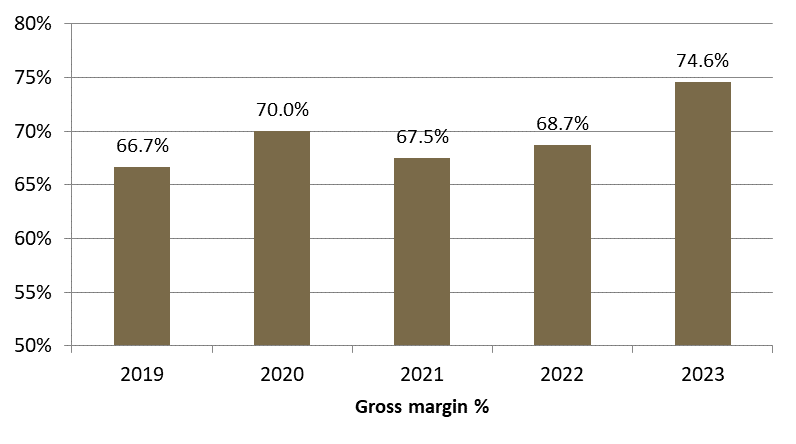

During the couple of hours visit to Lund, we went through all their existing devices and what was in the R&D pipeline at the time. Jing mentioned that the next-generation hardware (updated 2023 hardware) allows for an even better gross margin, and this has held true. Furthermore, the current hardware is much more easily scalable, and the “brains” of different devices are very similar to each other, as are the user interface and appearance.

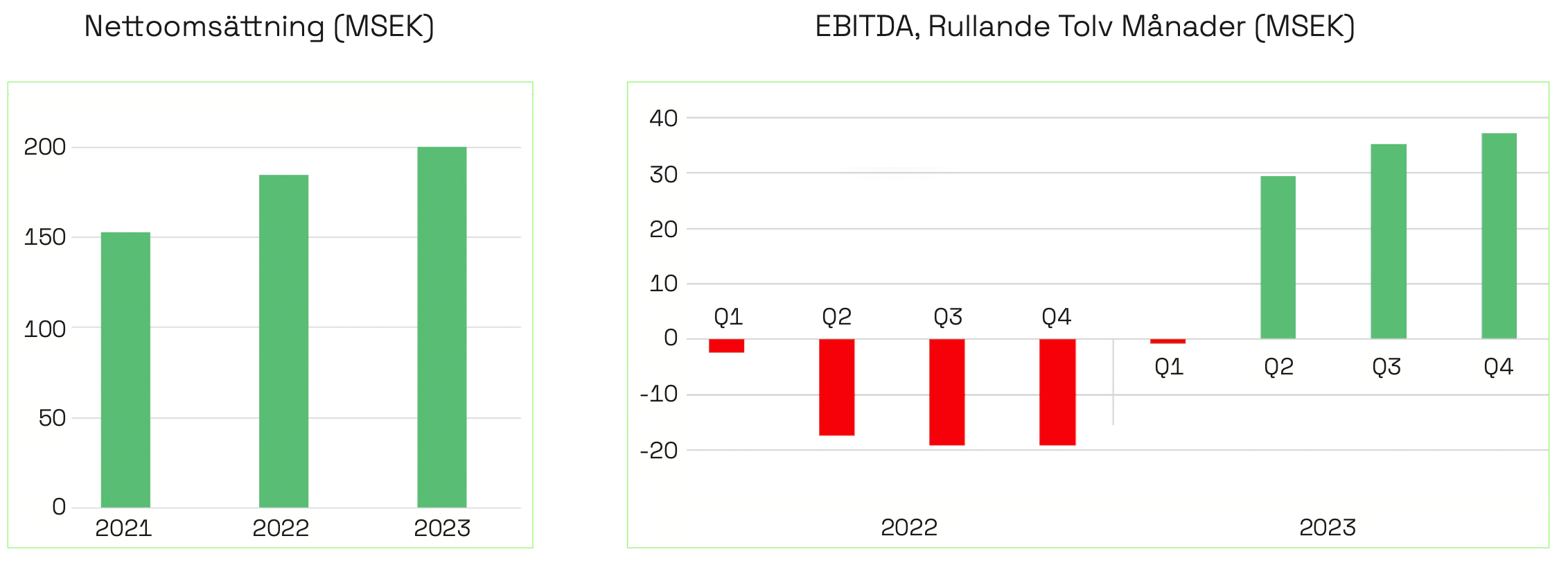

Due to the high gross margin, the company achieved a 30% operating margin last year. In my opinion, this level is sustainable. If volumes grow, the margin should rise to an even higher level. On the other hand, it’s worth remembering the increase in staff from 12 to 16 for this year, which will be reflected in higher personnel costs, especially this year. The company’s products are sensitive to capital expenditure, recurring revenue is non-existent, and in the worst-case scenario, the company could post a loss in a single quarter. BPC operates in a niche market and, if I remember correctly, they have a market share of over 90% in biogas. Competition may intensify, which could cause price pressure, but on the other hand, volume growth provides tailwinds due to economies of scale.

Currently, BPC is listed on Spotlight in Sweden. I believe that in the near future, the company intends to move to First North. In connection with this, I also believe Jing will slightly reduce his current 65% stake (perhaps a reduction of 5-10 percentage points).

Summa summarum. An interesting, profitable small instrument company operating in niche markets. The main industry is growing, and the penetration rate into other industries is still in its early stages. 95% customer satisfaction reflects the quality of the products. Let’s remember, however, that as recently as 2023, the company had only 12 employees. When I visited their office last year, there were devices all over the office ![]() There were many stacks of hardware on the secretary’s desk

There were many stacks of hardware on the secretary’s desk ![]()