Terveystalo is coming to ROAST ![]() , so let’s open a dedicated thread for the company here.

, so let’s open a dedicated thread for the company here.

ROAST LIVE starts on inderesTV on August 21st around 10:15 AM ROAST Terveystalo 21.8.2018 - Inderes

Terveystalo is coming to ROAST ![]() , so let’s open a dedicated thread for the company here.

, so let’s open a dedicated thread for the company here.

ROAST LIVE starts on inderesTV on August 21st around 10:15 AM ROAST Terveystalo 21.8.2018 - Inderes

Excellent!! Good that we’re getting this place roasted. I’m interested in the health and social care sector (Sote) and how this differs from Pihlajalinna!!

Competitor Pihlajalinna continues to struggle with profitability issues https://www.inderes.fi/tiedotteet/pihlajalinnan-puolivuosikatsaus-11-3062018-6-kk

Has the Attendo acquisition created a competitive advantage in the public or private sector?

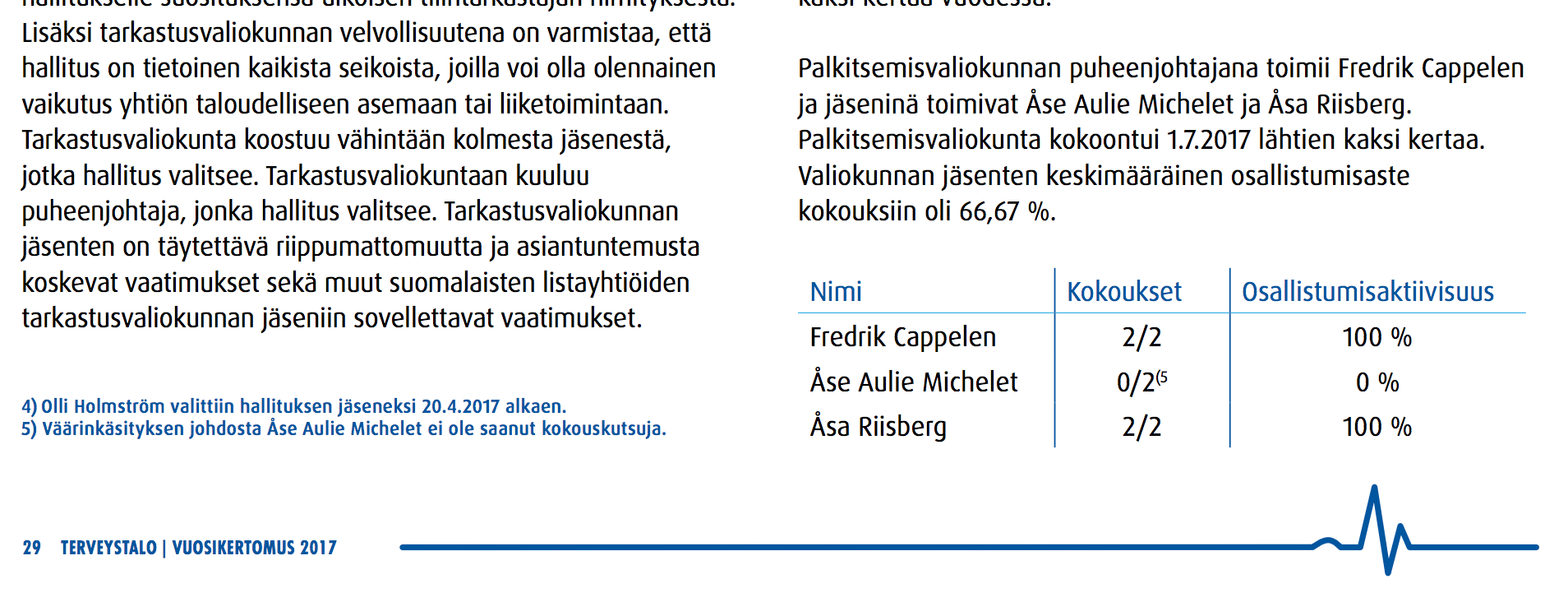

A funny curiosity in Terveystalo’s annual report:

“5) Due to a misunderstanding, Åse Aulie Michelet has not received meeting invitations.”

It happens even in the best circles.

(The duties of the Remuneration Committee include, among others, “The Board’s Remuneration Committee identifies persons who would be qualified to serve as the company’s CEO and provides the Board with its recommendation on the selection of the CEO.”)

Heated debate on the social and health care reform increases:

Here is the entire ROAST, and the same link provides a timed breakdown of what was asked and discussed: ROAST Terveystalo 21.8.2018 - Inderes

Here is the content:

00:40 Who are you and where are you from?

01:20 What does Terveystalo do?

02:01 A short pitch: why would Terveystalo be a good investment?

02:41 Is it acceptable to make money from healthcare?

04:10 Big data and leveraging patient data: can it be monetized?

06:12 The importance of culture in Terveystalo through the eyes of the CEO?

07:58 Insurance companies and healthcare companies collaborate at different levels. How does Terveystalo position itself in relation to insurance companies and competitors?

09:40 How has Terveystalo prepared for the departure of key personnel?

11:28 How have occupational health customerships developed this year, and what advantages does Terveystalo have in this market?

14:50 Diacor acquisition: how has the integration gone from the perspective of occupational health customer retention? The ROAST production team has referred to customers switching to competitors.

16:50 What is the competition authority delaying in scrutinizing the Attendo acquisition?

18:00 Will there be co-determination negotiations at Attendo once the acquisition is finalized?

19:30 Many of Attendo’s municipal outsourcing contracts end in 2019 or in the coming years; did Terveystalo acquire expiring contracts?

21:20 Surgical operations and legislative changes: have you had to, for example, scale back surgical operations in Varkaus?

22:33 What proportion of occupational health contracts are fixed-price?

24:30 What is the role of digitalization at Terveystalo?

26:45 If the Sote (social and healthcare reform) is implemented, what will happen to occupational health?

29:32 How do you see the municipal outsourcing market when municipalities’ outsourcing possibilities are restricted?

33:48 What do Pihlajalinna and Mehiläinen do better than Terveystalo?

34:50 Is it difficult to find skilled professionals in Northern and Eastern Finland?

38:10 Terveystalo’s balance sheet contains significant goodwill, which the auditor has also noted. Should investors be concerned?

41:30 Most common challenges in corporate acquisitions?

43:00 Competition has intensified among private customers: is this a permanent state or temporary?

44:20 How would a recession affect Terveystalo?

46:20 Terveystalo’s goodwill on the balance sheet, combined with intensifying competition and political risks, is not dynamite?

48:00 Big game: are all the biggest healthcare companies sacrificing profitability for growth to become so large that they cannot be “ignored” if Sote comes into play?

50:54 Taxpayer’s perspective: is the market starting to concentrate worryingly on Mehiläinen and Terveystalo? At the same time, Sote is being rushed through, which would lead to inexperienced regions allocating funds…

54:10 How is Terveystalo positioned if Sote passes, or alternatively, if it does not pass?

56:15 Terveystalo’s profitability is reduced by large depreciation. Would you like to shed light on Terveystalo’s true profitability potential?

57:45 Where will Terveystalo be in five years?

Who’s next in the line of fire? ![]() Thanks @Verneri_Pulkkinen for the Terveystalo Roast. You do valuable work for investors, and for free!

Thanks @Verneri_Pulkkinen for the Terveystalo Roast. You do valuable work for investors, and for free! ![]()

Thanks, the best reward for the work is hearing that it brings joy! ![]()

Next ROAST: Information will be available on September 12th =)

Haha jokes best Roast ever coming. Knowledge is the monster that municipalities pay to get rid of ![]() absolutely brilliant!! Market this!

absolutely brilliant!! Market this!

Let’s push TTalo up again. The price has slipped to around 8€, and on Friday’s market panel, Taaleri’s Elomaa hinted that it’s now available “at good multiples.” For me, it would be important to find the deepest and highest quality analysis possible before making a purchase decision. Has anyone followed more closely why the price is lagging, and are there any analyses available? Thanks!

Edit: Annisa’s staff apparently got it at a price of 8.6-8.7€. Has the limit been breached, so the staff are panic selling to save their capital? Or what’s weighing it down… healthcare reform (sote)?

Aston is in a difficult position, considering that a stock that once cost 11 euros now costs 8 euros, and this change requires justification. The market doesn’t care at what price each investor bought the stock. Is 8 euros even dragging, or is it still a high price? It’s better to calculate the value of companies “from the bottom up.” What is the required rate of return on capital, what is the predicted development of interest rates? What is the risk level of the company and the industry, and what is the GDP development? In an ideal situation, you get a market value for the stock, which you can then compare to the price offered by the market.

Well, now it’s practically insider trading. EQT sold off its remaining ownership. EQT probably has a better view of Terveystalo than these new Finnish insiders ![]()

These acquisitions are purely related to Terveystalo’s listing and EQT’s subsequent divestment, so no conclusions can be drawn from them. And they haven’t been adding to their holdings at around eight euros now ![]()

P/E appears to be 18x for this year based on market forecasts… It’s uncertain whether the intensifying competition (everyone is investing heavily before the social and healthcare reform, Sote), as discussed in ROAST, will bring it down. And of course, the possibility of Sote failing is a concern, even though TT has played its cards well for both scenarios.

The Arttendo deal was apparently finalized recently. We’ll see if it has an impact on TT’s stock price development…

Please note that Terveystalo only acquired Attendo’s healthcare business, and Attendo (listed on the Stockholm Stock Exchange) still retains its care services in Finland.

Hehku departs. Olo arrives.

The government resigns and social and healthcare reform collapses. Olli comments.

Spot on.