Vahva tuloskasvu parantuneen operatiivisen tehokkuuden ansiosta

Heinä-syyskuu 2024 lyhyesti

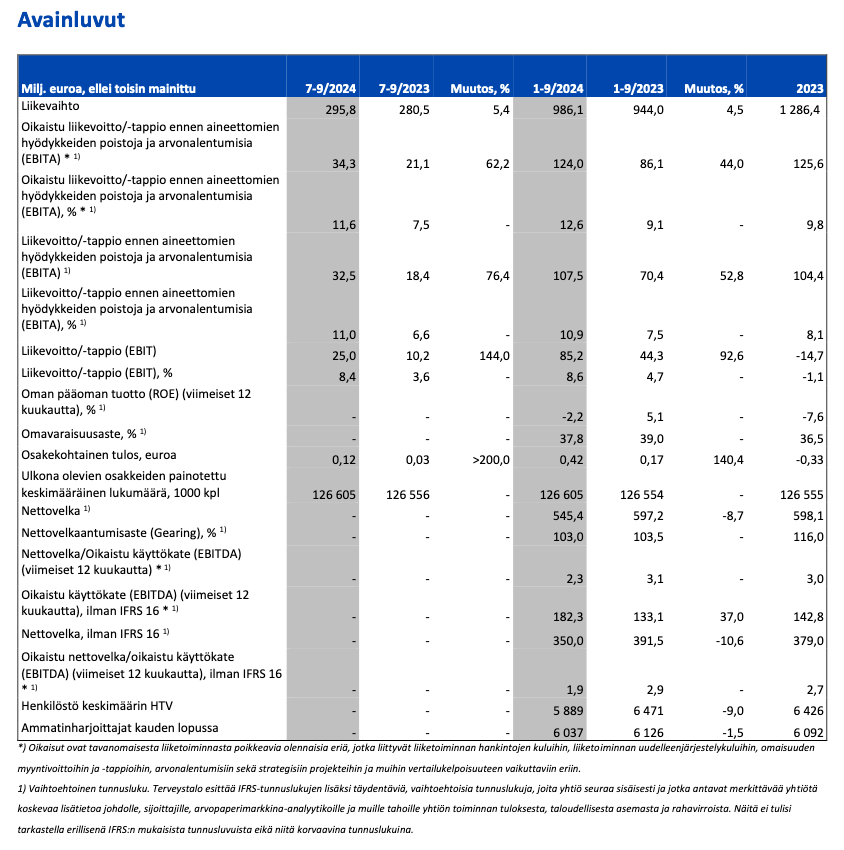

- Liikevaihto kasvoi 5,4 prosenttia vertailukaudesta 295,8 (280,5) miljoonaan euroon.

- Katsauskaudella oli yksi työpäivä enemmän kuin vertailukaudella. Terveydenhuollon palveluiden liikevaihto kasvoi 10,8 prosenttia ja oli 232,0 (209,3) miljoonaa euroa. Portfolioliiketoimintojen liikevaihto laski 9,9 prosenttia ja oli 54,5 (60,5) miljoonaa euroa. Ruotsi-segmentin liikevaihto laski 9,7 prosenttia ja oli 14,2 (15,8) miljoonaa euroa.

- Oikaistu[1)] liikevoitto ennen aineettomien hyödykkeiden poistoja ja arvonalentumisia (EBITA) kasvoi 62,2 prosenttia 34,3 (21,1) miljoonaan euroon ja oli 11,6 (7,5) prosenttia liikevaihdosta. Kannattavuus vahvistui Terveydenhuollon palveluissa ja Portfolioliiketoiminnoissa. Tulosparannusohjelman myötä vahvistunut operatiivinen tehokkuus, suotuisampi myynnin jakauma, tasapainoisempi katejakauma, sekä onnistuneet kaupalliset toimenpiteet vahvistivat kannattavuutta sekä euromääräisesti että suhteellisesti vertailukaudesta. Ruotsin liiketoiminnan kannattavuus laski selvästi vertailukaudesta päättyneiden sopimusten ja heikentyneen kysynnän aiheuttaman liikevaihdon laskun vuoksi.

- Vertailukelpoisuuteen vaikuttavat erät[1)], jotka vaikuttivat negatiivisesti EBITAan, olivat 1,8 (2,7) miljoonaa euroa.

- Kauden tulos oli 14,7 (3,3) miljoonaa euroa.

- Osakekohtainen tulos, EPS nelinkertaistui edellisvuodesta ja oli 0,12 (0,03) euroa.

- Liiketoiminnan rahavirta oli 41,3 (35,6) miljoonaa euroa.

- Asiakassuositteluindeksi NPS, vastaanotot, oli 86,8 (85,8). Sairaaloiden NPS oli 96,0 (96,8).

Tammi-syyskuu 2024 lyhyesti

- Liikevaihto kasvoi 4,5 prosenttia vertailukaudesta 986,1 (944,0) miljoonaan euroon.

- Terveydenhuollon palveluiden liikevaihto kasvoi 9,7 prosenttia ja oli 761,5 (693,8) miljoonaa euroa. Portfolioliiketoimintojen liikevaihto laski 9,0 prosenttia ja oli 181,8 (199,9) miljoonaa euroa.

- Ruotsi-segmentin liikevaihto laski 9,9 prosenttia ja oli 59,4 (65,9) miljoonaa euroa.

- Oikaistu[1)] liikevoitto ennen aineettomien hyödykkeiden poistoja ja arvonalentumisia (EBITA) kasvoi 44,0 prosenttia 124,0 (86,1) miljoonaan euroon ja oli 12,6 (9,1) prosenttia liikevaihdosta. Kannattavuus vahvistui Terveydenhuollon palveluissa ja Portfolioliiketoiminnoissa. Tulosparannusohjelman myötä vahvistunut operatiivinen tehokkuus, suotuisampi myynnin jakauma, tasapainoisempi katejakauma, sekä onnistuneet kaupalliset toimenpiteet vahvistivat kannattavuutta sekä euromääräisesti että suhteellisesti vertailukaudesta. Ruotsin liiketoiminnan kannattavuus laski selvästi vertailukaudesta päättyneiden sopimusten ja heikentyneen kysynnän aiheuttaman liikevaihdon laskun vuoksi. Vuoden 2023 neljännellä vuosineljänneksellä käynnistettiin Ruotsin liiketoiminta-alueella tulosparannusohjelma, jolla tavoitellaan kannattavuuden rakenteellista muutosta vuonna 2025. Ohjelma on edennyt suunnitellusti, ja kustannusrakennetta on sopeutettu vastaamaan heikentynyttä kysyntää. Toimenpiteiden vaikutukset alkoivat näkyä muun muassa palkkakustannusten laskuna kolmannella vuosineljänneksellä. Seuraavaksi ohjelman painopiste siirtyy operatiivisen tehokkuuden parantamiseen ja kaupallisiin toimenpiteisiin.

- Vertailukelpoisuuteen vaikuttavat erät[ 1)], jotka vaikuttivat negatiivisesti EBITAan, olivat 16,4 (15,7) miljoonaa euroa.

- Kauden tulos oli 52,7 (21,9) miljoonaa euroa.

- Osakekohtainen tulos, EPS kasvoi 140,4 prosenttia ja oli 0,42 (0,17) euroa.

- Nettovelka/oikaistu käyttökate oli 2,3 (3,1).

- Liiketoiminnan rahavirta oli 134,9 (97,4) miljoonaa euroa.

Toimitusjohtaja Ville Iho: Vahva tuloskasvu jatkui, luoden vankan perustan tulevalle arvonluonnille

Terveystalo jatkoi vahvaa kehitystään vuoden 2024 kolmannella neljänneksellä. Liikevaihtomme kasvoi noin 5 prosenttia 296 miljoonaan euroon, ja kannattavuutemme parani merkittävästi vertailukaudesta. Tulosparannustoimenpiteemme ovat osoittautuneet tehokkaiksi myös kausiluonteisesti alhaisemman kysynnän aikana. Oikaistu EBITA kasvoi yli 62 prosenttia 34 miljoonaan euroon, mikä vastaa 11,6 prosenttia liikevaihdosta. Osakekohtainen tuloksemme nelinkertaistui vertailukaudesta 0,12 euroon.

Terveydenhuollon palvelut segmentin erinomainen tuloskehitys jatkui kuudetta kvartaalia peräkkäin. Segmentin liikevaihto kasvoi lähes 11 prosenttia vertailukaudesta, saavuttaen 232 miljoonaa euroa vuoden kolmannella neljänneksellä. Liikevaihdon kasvuun vaikuttivat vahva tarjonta, parantunut myynnin jakauma, onnistuneet kaupalliset toimenpiteet, sekä aikaisin ja vahvana alkanut flunssakausi. Liikevaihto kasvoi kaikissa asiakasryhmissä. Kasvu ja parantunut operatiivinen tehokkuus nostivat segmentin oikaistun EBITAn 67 prosentilla 34 miljoonaan euroon, mikä oli noin 15 prosenttia liikevaihdosta. Ydinliiketoimintamme perustukset ovat vankalla pohjalla, ja jatkavat vahvistumistaan. Tulemme keskittymään kannattavaan kasvuun sekä vahvistamaan asiakkaillemme arvoa luovia palveluita, lääketieteellistä laatua ja operatiivista tehokkuutta.

Portfolioliiketoimintojen kannattavuus parani merkittävästi liikevaihdon 10 prosentin laskusta huolimatta. Segmentin oikaistu EBITA kasvoi 70 prosenttia vertailukaudesta noin 3 miljoonaan euroon ja oli 6 prosenttia liikevaihdosta. Segmentin liikevaihto oli noin 54 miljoonaa euroa. Tappiolliset ulkoistussopimukset ovat pääosin päättyneet, ja henkilöstöpalveluissa on tehty proaktiivista asiakasvalintaa kannattavuuden vahvistamiseksi. Suunterveyspalveluiden kysyntä jatkuu vaimeana, ja uudelleenjärjestäytyneen julkisen markkinan myynti etenee edelleen hitaasti. Uusia kilpailutuksia on nähty vain digitaalisissa palveluissa.

Tulosohjeistus vuodelle 2024

Terveystalo arvioi koko vuoden 2024 liikevaihdon kasvavan (2023: 1 286 miljoonaa euroa), ja oikaistun liikevoiton ennen aineettomien hyödykkeiden poistoja ja arvonalentumisia (EBITA) olevan 12,0-12,5 prosenttia liikevaihdosta (2023: 9,8 prosenttia).

Tiedotustilaisuus

Terveystalo järjestää englanninkielisen tuloswebcastin ja puhelinkonferenssin perjantaina 25.10.2024 klo 10.30. Webcastia voi seurata osoitteessa: Q3 2024