Taboola is an advertising and marketing platform for the open web. Its operations are based on user analytics rather than standard tracking and user data collection, as is the case with large players in more or less closed environments like Amazon, Google, Facebook, etc.

Taboola’s motto, “Content you may like,” largely describes its business principle. In other words, ads that display “Recommended for you” or similar are often produced by Taboola or its competitor Outbrain.

Thus, the user is presented with things and content that they are likely interested in. This is the opposite of, for example, searching for a specific item via Google. It’s an inverse search engine, in a way.

Furthermore, the technology used is significant. It does not use cookies, which currently cause problems and are likely to be phased out or have their functionality significantly restricted in the future. Taboola’s operations are based on machine learning and will increasingly rely on deep learning:

Four years ago we evolved our technology from Machine Learning to Deep Learning. In simple terms, Machine Learning looks at known parameters to try to predict user behaviors and needs. While effective, it depends on us knowing exactly what the right parameters were to predict behaviors. Deep Learning is more advanced in that it figures out what the parameters are, making behavioral predictions much more accurate, self-learned, and independent of our intervention. We believe this puts us far ahead of our competitors and our significant experience makes it harder for them to catch up.

Clients and references

Globally, many media companies find it important to keep visitors on their pages. Content marketing is essential, and here Taboola’s algorithms help visitors find interesting content.

SPAC merger

Taboola is going public via a SPAC merger in Q2 or early Q3 of 2021. ION Acquisition Corp. (which trades under the ticker $IACA) will be the target of the merger. After the merger, the ticker will be $TBLA.

At the time of the binding agreement’s publication, Taboola was widely discussed, and its share price reached $17, maintaining a good level around $13 as a promising target. Due to the meltdown in growth stocks and especially SPACs, the share price is currently at NAV (Net Asset Value) level. However, the valuation at this level is favorable, and after the merger, many institutions can also buy once purchasing restrictions are lifted. De-SPAC (companies that have completed a SPAC merger) share price movements have been varied, so volatility is to be expected with this one too.

Investor material, January 2021.

Other recommended reading

Investopedia - Taboola: How “Content You May Like” Makes Money

https://www.investopedia.com/articles/personal-finance/032515/taboola-how-content-you-may-makes-money.asp

A very good Seeking Alpha article explaining the operations, risks, and potential:

https://seekingalpha.com/article/4415134-taboola-out-of-favor-adtech-presents-good-buying-opportunity

Comments from CEO and founder Adam Singolda in connection with the Q1 report. Further clarifies the company’s operations:

https://sec.report/Document/0001140361-21-017575/

A few excerpts from the articles:

Business model - where the money comes from

How Content Marketing Business Works

- The content contributors (advertisers) who wish to drive traffic to their sites and are willing to pay for it in the role of advertisers.

- The publishers (bloggers/site owners) who put a Taboola widget on their site and get paid for displaying the links.

- The interface (Taboola) which connects the contributors and publishers and facilitates the functioning of the marketplace.

Ad blockers are a risk; if ads are not displayed, revenue is lost. When produced through the server to the pages, they are more visible, and ad blockers do not catch them as easily.

Although Taboola is at risk of revenue loss from adblockers, unlike many other advertisers they do not make use of any third-party cookies. Third-party cookies are already blocked in some web browsers such as Safari and Firefox, and will soon be blocked in Chrome. This makes Taboola a little more resilient than some other adtech platforms. The rise of adblockers however will likely continue to be a threat to Taboola’s business model.

Ads appear in many places other than browsers. Online stores, games, applications, TVs, etc.

Over the next 10 years I see Taboola growing to power recommendations for anything, such as eCommerce, games, applications, and I see those recommendations everywhere, on every device. They will live on our connected TVs at home, recommending shows people love, as well as in people’s cars surfacing content they love, podcasts, and text-to-audio from the open web. – Adam Singolda, Founder and CEO of Taboola

Competitors

Outbrain operates in a very similar way. Together with Taboola, they have an 80% market share in, for example, the UK (source: previous Seeking Alpha article) in open web advertising.

Large online advertisers: Google, Facebook, etc. - These, however, are primarily within their own ecosystems. Google, of course, does a lot otherwise.

Smaller niche players.

Economy and business

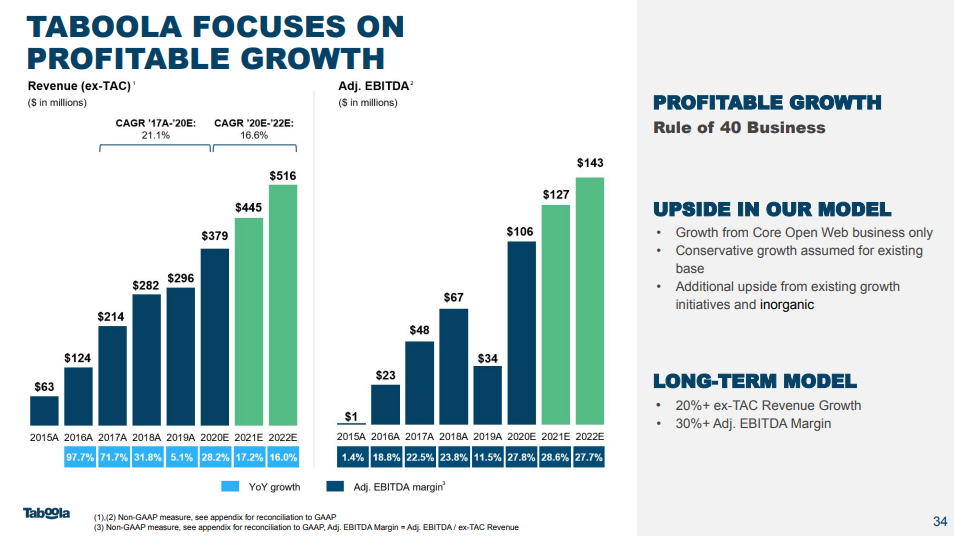

At the time of listing, the valuation was $2612M, with revenue (ex-TAC) of $379M in 2020 and an estimated $445M in 2021.

Ex-TAC (Traffic Acquisition Cost) is the figure where the portion returned to advertisers has been deducted from gross revenue. Compare this to the business model where money flows are explained.

After the merger, $582M will remain in cash, which is intended to be used to accelerate growth.

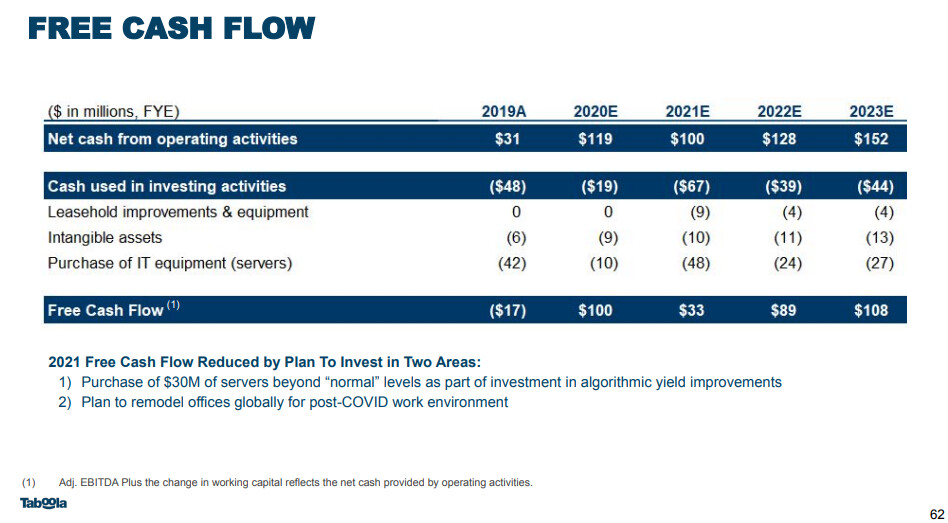

Unlike many SPACs, Taboola is already profitable, has positive free cash flow, and its growth figures are robust. Based on investor materials, the valuation is favorable at an assumed price of $10:

2021E: P/S ~5 and P/E ~16

2022E: P/S ~4 and P/E ~14

Q1 2021 exceeded estimates, and Q2 and FY2021 forecasts have been raised, making the above figures even more favorable.

2021 Q1 report and new outlook:

https://sec.report/Document/0001140361-21-017574/

Disclaimer: At the time of writing, I hold a significant position in my portfolio - at least part of the position is intended for long-term holding.