Let’s start a dedicated thread for Taaleri. This “mini-Sampo” of Helsinki definitely deserves active discussion and monitoring.

Edit: Latest comprehensive company report Waiting for corporate restructurings 29.6.2018

Let’s start a dedicated thread for Taaleri. This “mini-Sampo” of Helsinki definitely deserves active discussion and monitoring.

Edit: Latest comprehensive company report Waiting for corporate restructurings 29.6.2018

Here, too, we are waiting for comments on the latest acquisitions (Suomen Vuokravastuu Oy / Evervest Oy), even though they are not very significant in terms of their size.

This discusses Wärtsilä, sorry, but more generally about the world’s energy needs…

Thanks to Warren Fyffet (Shareville) for the heads-up. Taaleri is Kauppalehti’s stock of the month

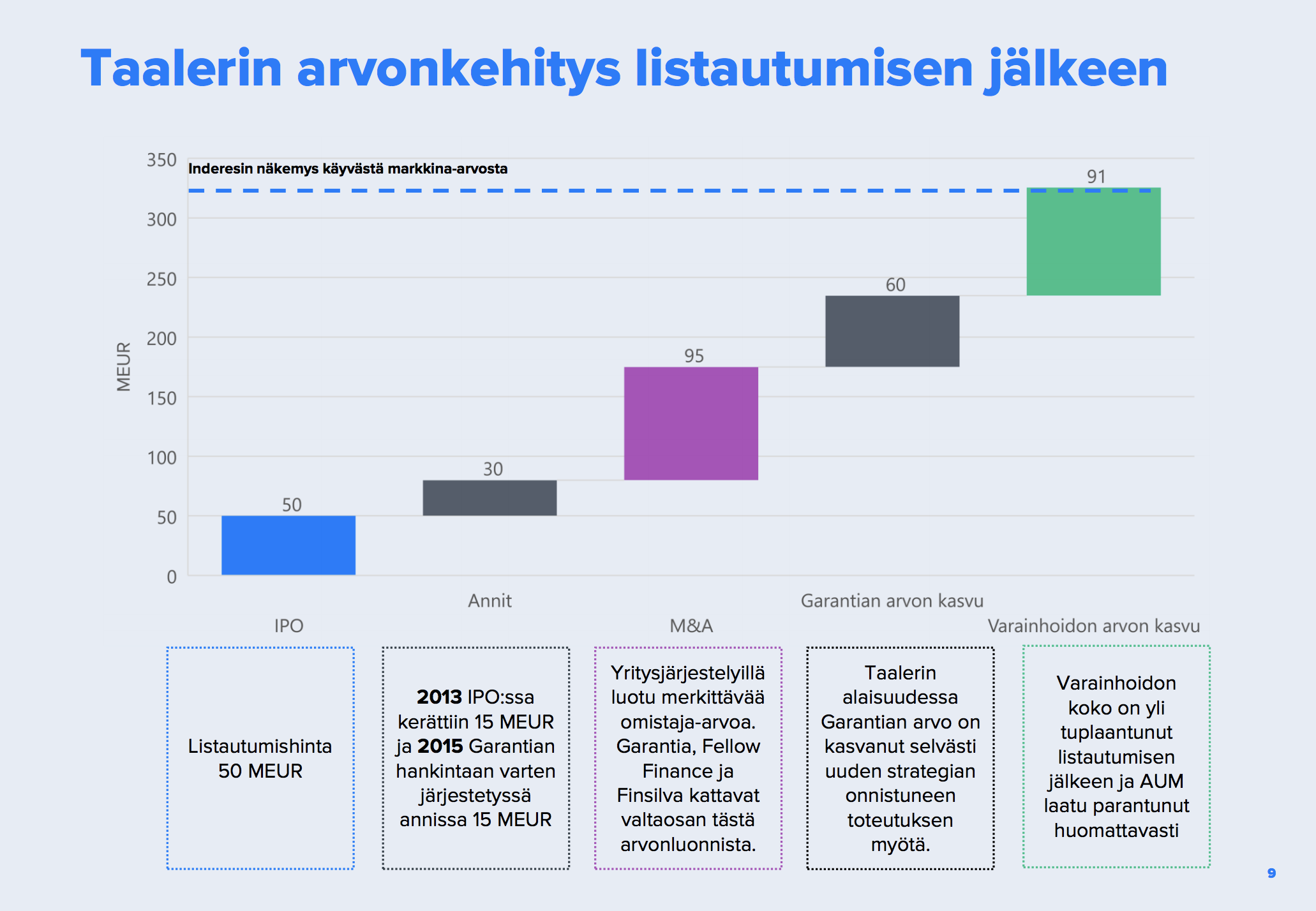

€9.8 means a market cap of ~280 million… However, considering the “sum of the parts” of the company, Garantia’s estimated total would be in the range of ~360 million… This would mean a share price of around €12.5.

Do others see significant upside here? Is my beginner’s logic badly flawed? To what extent should Garantia’s value be reflected in the share price today?

Edit: Edited the figures slightly downwards, apparently the original news has also been modified.

There should probably be a clear message about Garantia’s (Garantia) spin-off that would act as a catalyst for the stock. This case always seems to “fall asleep”.

I’ll have to slowly refuel more below ten. There’s plenty of time to wait, and the margin of safety is sufficient with this valuation.

Yep, Taaleri, like certain other stocks, is like my calathea plant – I only remember to water it when all the leaves are already drooping towards the ground, at which point the plant springs back to full strength in a couple of hours and soon starts pushing out flowers, then slowly droops again until I remember to water it. I like these dozing stocks in my long-term portfolio; instead of watering, I get to buy more at a reasonable price when they slump. It’s a different story with those that wither for a reason.

I already teased Juhani about this in ROAST, asking if patriotism at Taaleri (Taaleri) outweighs economic logic… I don’t know what the ROI (Return on Investment) is on these ships, but the flags are flying https://www.inderes.fi/tiedotteet/aalto-shipping-varustamon-kaksi-laivaa-liehuttaa-nyt-upeasti-suomen-lippua-aalto

For patriotic investors, Taaleri is a perfect fit ; )

Watering the calathea is a good comparison. I bought more now that it’s under ten.

Taaleri is also likely looking to get its share from energy investments: Kauppalehti

1000 billion (i.e., a trillion?) will be spent by 2040, which is about ~45 billion USD per year globally. Surely it’s possible to carve something out of that.

Can someone explain Taaleri’s business model in this scenario? Energy funds in the making, or what?

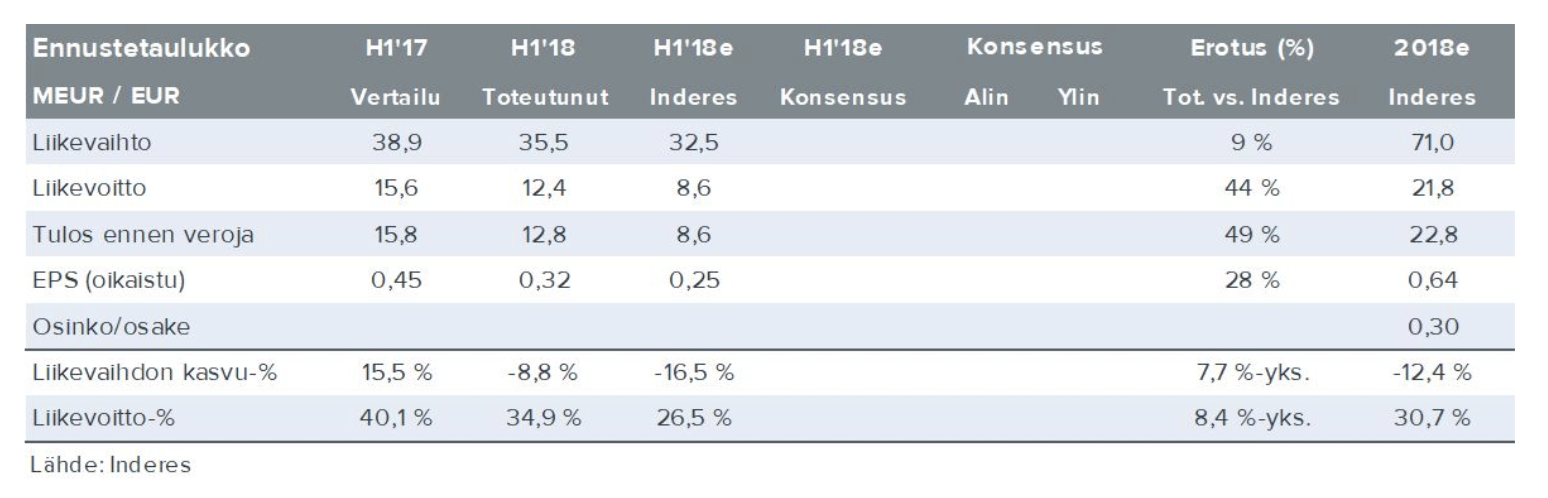

Well, we received a good and high-quality extensive report today. Hopefully, those corporate arrangements (G and FF) will be realized at a good price before the next bear market begins.

Let’s put this here too: Sauli’s comments can also be found on InderesTV (Taaleri sijoituskohteena - Inderes). Taaleri’s track record in corporate reorganizations is admittedly impressive ![]()

July 9, 2018: Rauma Shipyard’s Last Year Severely Loss-Making

I wonder if the current poor situation has any impact on the parent company (Taaleri Oyj)? Fortunately, the rather large Squadron 2020 project is in sight…

Yours, Amateur

I’ve now been investing in the stock market for about 10 years, and a lot has happened along the way. Diversification has radically decreased year by year, based on the quality of the stock. My owner-occupied apartment has changed to a rented one, and my car is now leased.

Today was the day when there’s no more diversification, and my portfolio only contains one stock – Taaleri. All my assets are tied up in Taaleri. It’s by far the highest quality and most interesting company on the Helsinki Stock Exchange. Top management and significantly undervalued at the current price. In my own sum-of-parts calculation, the value is just under €15.

I will continue to follow Taaleri’s movements very closely on different channels, but today I raise a toast to myself and to the characteristic that connects me and Taaleri. To courage. ![]()

Hoivatilat, Remedy, and Taaleri are the most important and largest positions for me. I might add a bit more Taaleri if it drops below €10.

Edit: Inderes’ recent analysis naturally still lacks the effects of future acquisitions on the target price, but their potential effects are well explained in the analysis. After GARANTIA, a €15 target price for Taaleri is very possible if it finds a suitable investment target for the money…

Taaleri, by the way, partly sold its ownership in Inderes last winter…

Interesting tidbit… Who bought them? Would fit Nordnet at least. Other banks have their own analysis operations (but bad ones) but Nordnet lacks this and they use Inderes. They could also help Inderes conquer Sweden.

…the Finns themselves bought to put in their pockets… ![]()

Congratulations, I also have a very strong feeling about the company’s development. It’s definitely staying in my portfolio. ![]()