The bear is always lurking around the corner, but it rarely shows up in the end

This is a very different case than Enersense. In Enersense, the visibility into individual projects was really poor (read: non-existent), and thus investors were largely dependent on what management said. In addition, mergers and acquisitions had a clear weight in the case, which equally required trust in management. In Fellow Finance, the platform has proven its functionality in Finland, and visibility into strategy and international expansion is actually quite good. Here, the question is more about whether the investor believes in the industry and the company’s competitiveness in international markets. Of course, when talking about a company that wants to multiply its turnover in a relatively short period, the investor must also believe in the management’s ability to lead the company to its goals.

Two major owners, Berling Capital Oy and Capercaillie Capital Oy, have been selling a large portion of their holdings for over a year now. Soon they will run out of chips to sell, and this will certainly have its own impact. It will be interesting to see the effect of the write-up made in connection with FellowFinance’s listing on the share price. Several significant launches are scheduled for the end of the year, and projects are progressing! The situation looks really good if the market just holds up

Berling Capital (one of the founders) has been selling for several years already. This has naturally put pressure on the share price, as there is constant pressure on the sell side.

Why is Berling Capital selling if the stock is undervalued?

Taaleri’s recommendation should now logically decrease, as FF is gradually being divested at significantly below its true value. Taaleri will receive some cash, for which it needs to find a profitable investment to compensate for the FF sales.

I don’t know the exact reasons for Berling Capital’s sales. I haven’t been on the board for years.

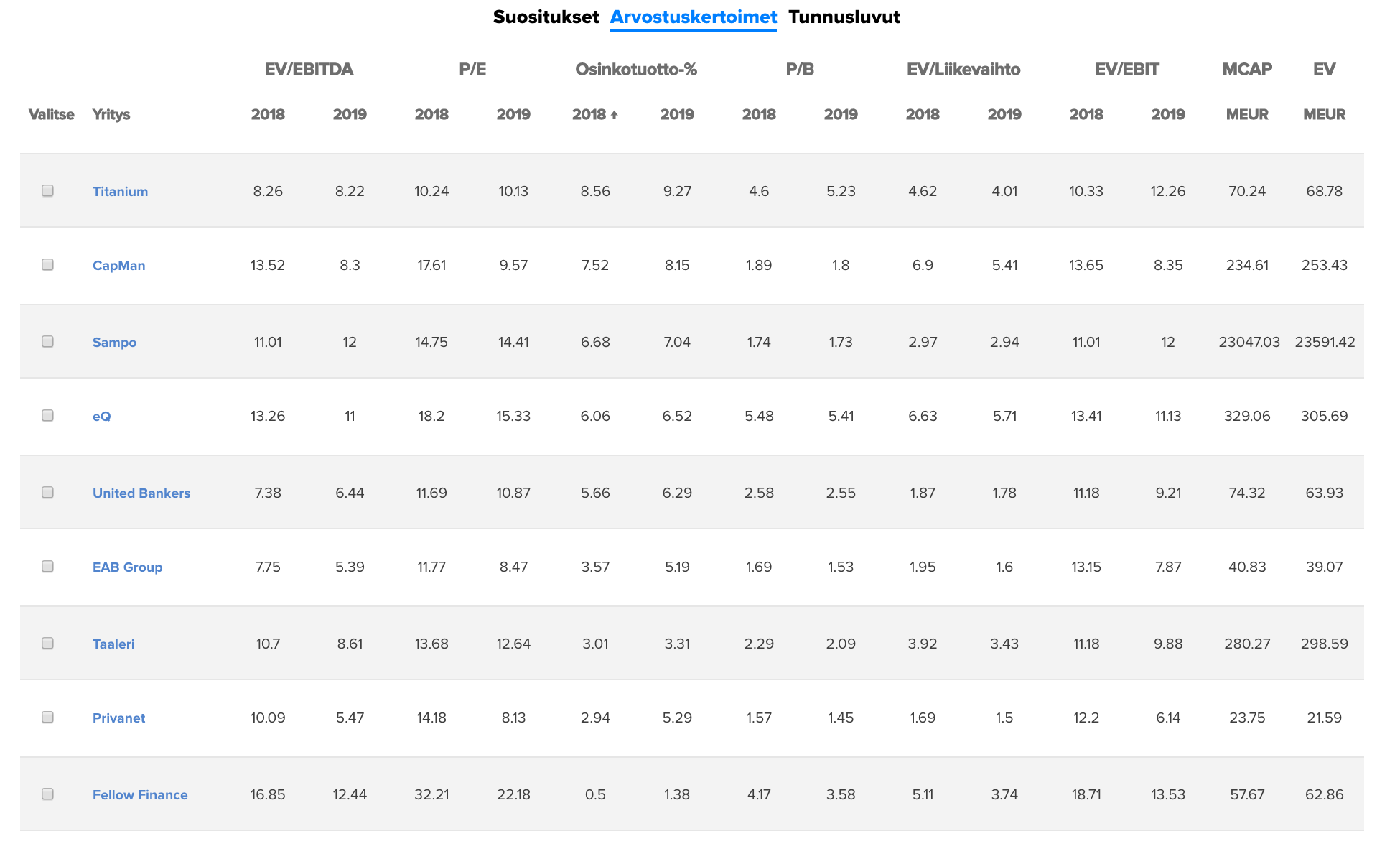

The effect of FF on the sum of Taaleri’s parts also depends heavily on the price at which the markets value FF. If the price remains at the IPO price level, FF’s value will slightly decrease our sum of parts. Conversely, if the markets price FF above the IPO price (as we expect in our analysis), the negative impact will be smaller. If the market were to price FF at our predicted level, the IPO would have a small positive effect on the sum of Taaleri’s parts overall. It’s important to remember that Taaleri will ultimately sell less than half of its FF ownership and will remain FF’s clearly largest owner. We will update our view on Taaleri as soon as FF’s trading begins.

Taaleri: Records approximately 5 million euro capital gain on Fellow Finance’s IPO

Taaleri announced yesterday that it had sold 813,262 shares of its associated company Fellow Finance Plc in connection with its First North listing. Taaleri’s ownership in Fellow Finance, which provides a crowdfunding platform for businesses and consumers, will thus decrease from 45.7% to 26.0%. Taaleri will record a capital gain of approximately 5 million euros from the sale in the second half of 2018.

The capital gain will significantly strengthen the results for the second half of 2018. Our forecast for H2 operating profit has been 10.8 million euros and does not include the Fellow Finance IPO. Our 2018 forecast has been 23 million euros and, taking into account the capital gain, would rise to approximately last year’s level (27.6 million euros in 2017).

Taaleri’s share keeps lingering, but the entire financial sector seems to be in a somewhat hesitant waiting mood: high dividend yields, but shares still not appealing?

Sauli just commented on how the increased market uncertainty at UB (United Bankers) raises the risk level.

It’s interesting that the target price decreased so much. According to Sauli’s previous reports, the target price had taken into account “the market moving into a mild recession” (not an exact quote).

A full recession is not yet upon us: Although the market situation is still reasonable and the market decline has been limited (especially in relation to the long boom), it is important for investors to remember that financial companies’ results are very sensitive to capital market movements.

Not that it matters, I naturally trust Sauli’s assessment.

Earlier, I had noted a slight weakening of the market situation in the forecasts, but not a correction of the current kind. In addition, in my report from a couple of weeks ago, I was too optimistic about the company’s performance fees. In hindsight, it’s easy to say that they should have been cut more aggressively back then. The same applies partly to Garantia’s (Guarantee’s) portfolio as well.

First you buy high, then you sell low. This kills the profit!

But I’m wondering about the measure of the goodness of these analyses. It’s not valuable at all to look at turning points and then state that a turning point occurred and it affects the assessment. Should those giving recommendations calculate the integral between target prices? With a “Buy” recommendation, a future share price level that is higher than the share price level at the time of the recommendation would have a positive effect, and a share price drop a negative one. Perhaps the frequency of recommendations should be controlled, or otherwise a single “Buy” recommendation in the spring of 2009 would have been enough for a huge profit. “Buy” recommendations at market peaks lead to huge losses, so it’s good that recommendations are changed and we return closer to fundamentals. I’m off to roll the dice.

But what’s happening here is typical for recommendations. They always predict growth. For which company are declining earnings or declining revenue predicted? Probably not many. Then when things start to go down, predictions have to be lowered accordingly.

The function model should probably be calculated with some program, or maybe it’s easier to just sum the daily price differences with a snippet of code. It seems to me that many companies’ stock prices go up and down. The length of the cycles varies. Analysts sometimes give accurate reduce and sell recommendations. It would be interesting to know how often they are on the right track.

According to the Ministry of Finance, Finland’s economic growth is slowing down, but is still fast. The Ministry forecasts growth of 2.5 percent for this year and 1.5 percent for next year. The Ministry estimates that economic growth will slow down in the coming years as export growth slows and willingness to invest decreases.

Director General Mikko Spolander states that the economic boom has peaked and growth is returning to near normal pace.

Finland’s economic situation does not look entirely hopeless for next year. @Sauli_Vilen Should Taaler be allowed a “12-month target price” based on fair value, or should we continue to emphasize sector valuation multiples for now?

Another issue, of course, is macro political risks, etc. Are these more significant for Taaler than Finland’s economic outlook for next year? The macro situation is certainly causing a lot of uncertainty right now…