Q3 ulkona. En tiedä mitä johtopäätöksiä pitää tehdä, kun jokaisen teknopainotteisen small cap ruotsalaisosakkeen kohdalla tuntuu kurssi nousevan tulosjulkistuksen jälkeen. Ehkä nyt sentimentti näiden riskisiksi koettujen osakkeiden kohdalla on lopultakin kääntynyt. Harmillista näissä on se, että Inderes ei näitä seuraa, saisi kuunnella työmatkalla aina sopivat 10 min kiteytyksen kustakin osavuosikatsauksesta. Joka tapauksessa nopealla silmäyksellä ainakin kassavirta on vahvistunut.

Uskon että tämä on ruotsalaisten oma suosikki ja konsa sentimentti kääntyy niin tämä lähtee keulilla ryntäämään.

Yritysosto briteistä

Ketju on ollut hiljainen, mutta otsikoihin nousi viime viikolla SUS:n tulosvaroitus vuoden kakkoskvartaalia koskien.

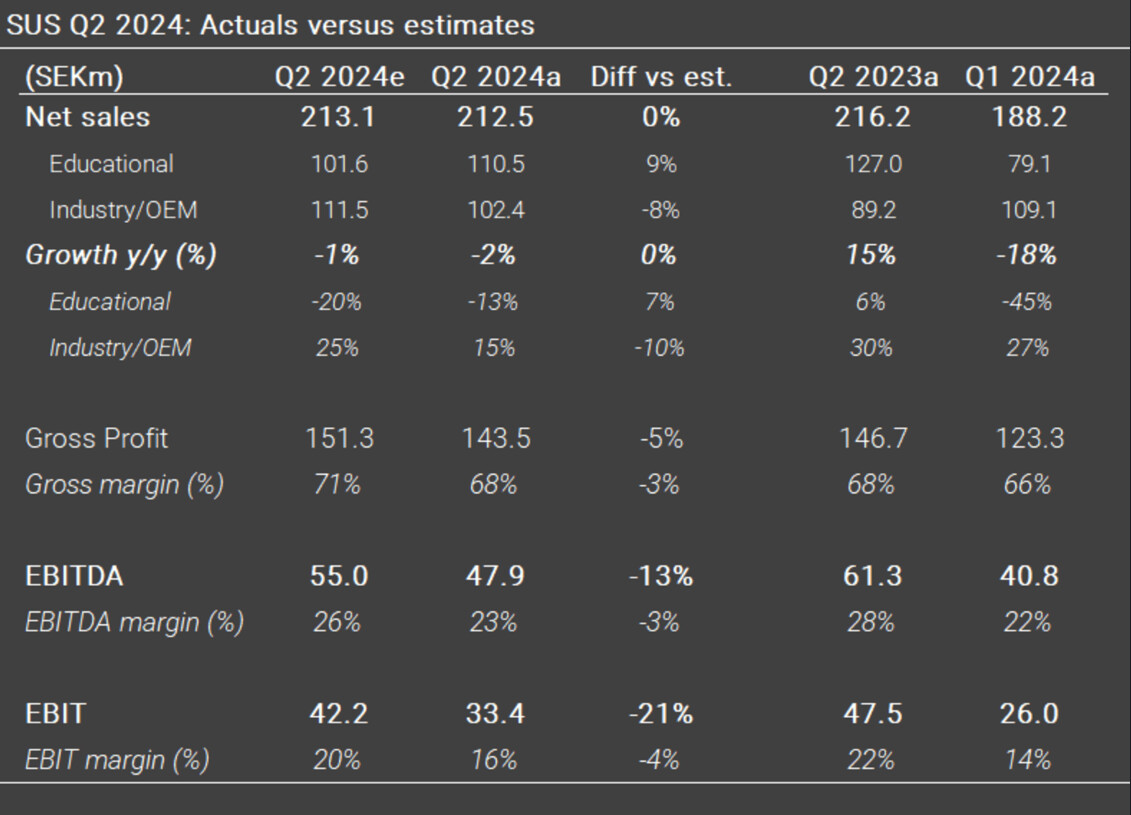

Liikevaihto: 209 MSEK, -2 % vrt. Q2/2024

Liikevoitto on tappiollinen, –22 miljoonaa kruunua.

Aikamoinen ryppy kasvutarinaan ja kurssi romahti kolmanneksella.

Jos uskoo robottikirurgian etenemiseen ja SUS:n olevan siinä vahvasti mukana, niin sietää ehkä tarkastella yhtiön suorittamista loppuvuoden aikana. (Ei omistusta juuri nyt, mutta saapa nähdä.)

EDIT: Hauska nähdä Pareton aiempia tavoitehintoja ketjun alkupuolella ![]()

Sipaisin tämän dipin, koska haluan katsoa dV5 rolloutin H2/2025-2026. Toivottavasti perse kestää merivettä, tämä laiva kiikuttaa varmasti puolelta toiselle.

Pari päivitystä:

Pareto 11.8.

Danske 12.8.

Löytyyhän tämä TIN fonder NY Teknik isoimpana sekä RE Top Picks ym. Eri asia onko ensimmäinen tietysti ‘meriitti’ ![]()

Löytyy myös RE:n rahastosta. En yllättyisi, jos olisivat lisäilemässä. Itsekin tätä nappasin ekstra possan lähinnä pompun toivossa, kun tämä 100sek tuntui niin ilmeiseltä tukitasolta.

Tin Ny Teknik on kyllä mallisalkkuuntunut pahasti viime vuosina ja kontraaminen olisi ollut fiksumpaa ![]() Taisivat istua NOVO:ssakin melkeen koko pulkkamäen hupulta asti. Nyt sitten nautiskellaan Surgicalista ja QT:stä isolla painolla

Taisivat istua NOVO:ssakin melkeen koko pulkkamäen hupulta asti. Nyt sitten nautiskellaan Surgicalista ja QT:stä isolla painolla ![]()

Re kommenttia negariin ketjussa ei vielä tainnut olla.

Konferenssipuhelu Q2 osavuosikatsauksesta

Kutsu osallistua Surgical Sciencen konferenssipuheluun koskien tammi-kesäkuun 2025 osavuosikatsauksen esittelyä. Esitys pidetään englanniksi.

Aika: Torstai, 21. elokuuta klo 11.00 CET

Jos haluat osallistua verkkolähetyksen kautta, käytä alla olevaa linkkiä. Verkkolähetyksen kautta on mahdollista esittää kirjallisia kysymyksiä.

Jos haluat osallistua puhelinkonferenssin kautta, rekisteröidy alla olevan linkin kautta. Rekisteröitymisen jälkeen saat puhelinnumeron ja konferenssitunnuksen konferenssiin pääsyä varten. Puhelinkonferenssin kautta on mahdollista esittää suullisia kysymyksiä.

Surgical Sciencen osallistujat ovat:

Tom Englund, toimitusjohtaja

Anna Ahlberg, talousjohtaja

Lehdistötiedote Surgical Sciencen tammi-kesäkuun 2025 osavuosikatsauksesta julkaistaan 21. elokuuta 2025 klo 07.30 CET.

Ennen konferenssipuhelun alkua esitysmateriaali on saatavilla yhtiön verkkosivuilla kohdassa Sijoittajat, Esitykset.

Göteborg, Ruotsi, 11. elokuuta 2025

Surgical Science Sweden AB (publ)

Lehdistötiedote kokonaisuudessaan on saatavilla liitteenä tai osoitteesta:

Katsotaan nytkähtääkö kuollut lahna mihinkään lähipäivinä

Tulos oli jo tiedossa. CEO kootut selitykset:

2026 jälkeisiin tavoitteisiin tulossa päivitystä syksyllä. En kyllä itse odota, että v. 2026 tavoitteeseen päästään välttämättä, katsotaan. Ehkä ensi vuoden tavoitteita viilataan samalla kuin seuraavan strategiakauden tavoitteita tarjotaan?

Joulukuussa CMD:

DNB päivitellyt analyysiä pre Q3. Iso kysymys lähteekö da Vinci 5 rollout odotetusti käyntiin, palaako kasvuluvut parempaan ‘karmean tariffiquarterin’ jälkeen? Jos palaavat, niin osake on halpa. Kvartaaliheilunta on massiivista, joteen kannattavaa katsoa vuosittaisia lukuja ja ennusteita

Leikkaussimulaattorit on kiinnostava kokonaisuus.

Yhtäältä jokaisen mieleen on järkevää, että leikkaustoimenpidettä voisi kuivaharjotella, tai tehdä perehdyttää peruskoulutuksessa, jne.

Mutta se mikä unohtuu herkästi on, että leikkauksissa on jo teknologiaa joilla tehdään kuivaharjoittelua, eivätkä ne ole simulaattoreita vaan laitteita.

Sitten on paljon teknologiaa jota pitäisi käyttää. Otetaan yksi esimerkki: magneettikuvauslaitteet.

Mayo Clinicassa on ainakin 8 magneettikuvauslaitetta, joita EI käytetä potilaiden kuvantamiseen tai diagnostiikkaan, vaan pelkästään kehitystyöhön. Kirurgit ja yritykset mallaavat erilaisia magneettikuvauksen aikana käytettäviä työkaluja ja menetelmiä (niin sanottu leikkauksenaikainen kuvantaminen tai jargonisesti intraoperative MRI eli iMRI).

Jos hankkisimme rompetta ja laitetta, se täyttäisi simulaattorin tarpeet. Ja toisin kuin simulaattori, se olisi täydellisesti yks-yhteen käytettyjen työkalujen kanssa.

Näistä syistä asenteeni simulaattoreita kohtaan sairaanhoidossa on hieman pessimistinen: Jos simulaattori oikeasti toimisi ja se todettaisiin erinomaiseksi, simulaattoriyrityksellä olisi kaikki osaaminen mitä se tarvitsisi valmistaakseen täsmäkirurgian edellyttämiä robotteja ja laitteita.

Koska sillä ei tätä osaamista ole, ei sen simulaattorinkaan markkina tiettävästi kovin laaja ole.

Eräs sijoittaja kuvasi minulle aikanaan hyvin, että aina kannattaa katsoa onko kyseessä Need to Have vai Nice to Have ratkaisu. Nice to Havesta saa kyllä pakollisen, mutta tässä on suhteellisen suolainen todistustaakka.

Intuitive tekee robottileikkureita, ei simulaattoreita. Toki voi simuloida, mutta tuota sanoin toteamalle: “Mutta se mikä unohtuu herkästi on, että leikkauksissa on jo teknologiaa joilla tehdään kuivaharjoittelua, eivätkä ne ole simulaattoreita vaan laitteita.”

Surgical Science Sweden ei tee robottileikkureita, vaan simulaattoreita. Intuitiven myynnissä kohta “accessories” korvaa SSS:ää.

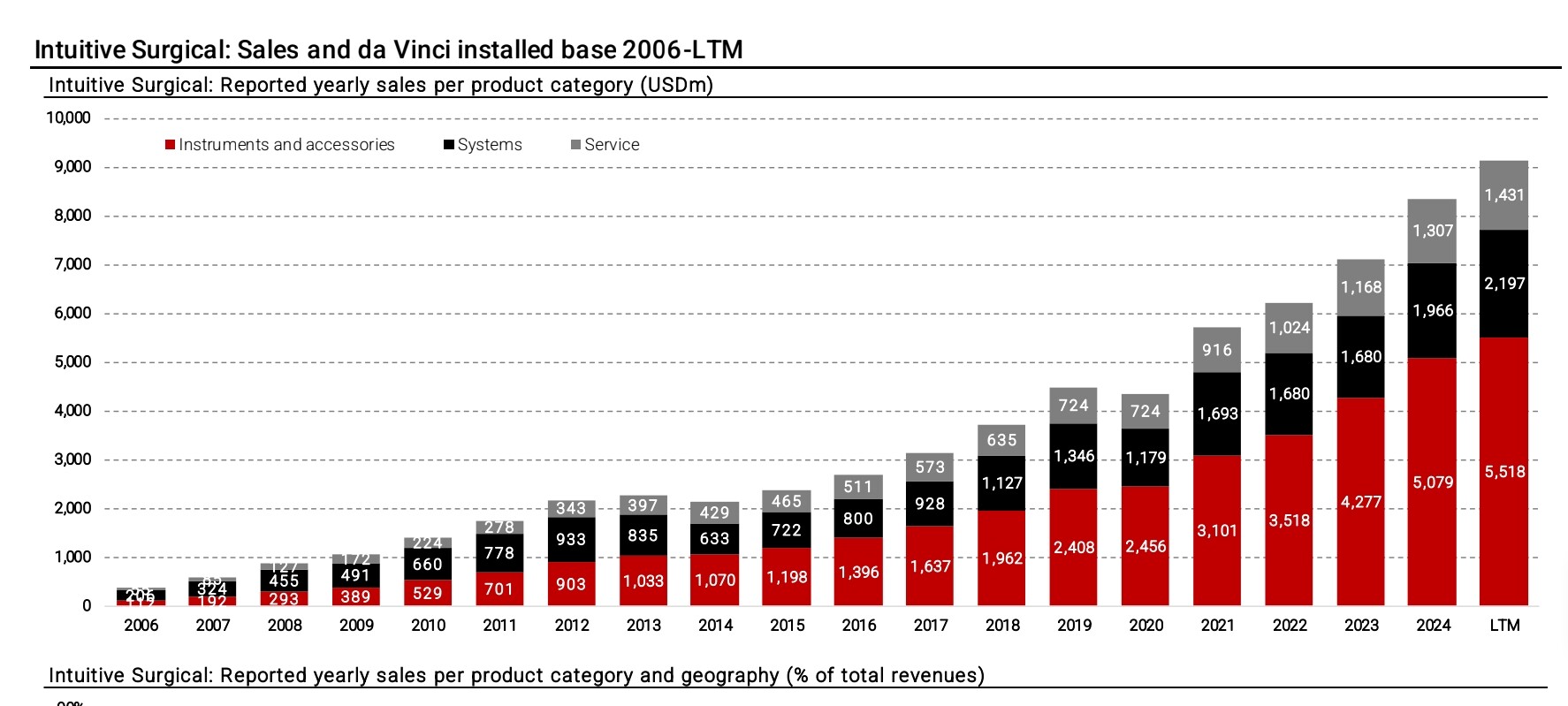

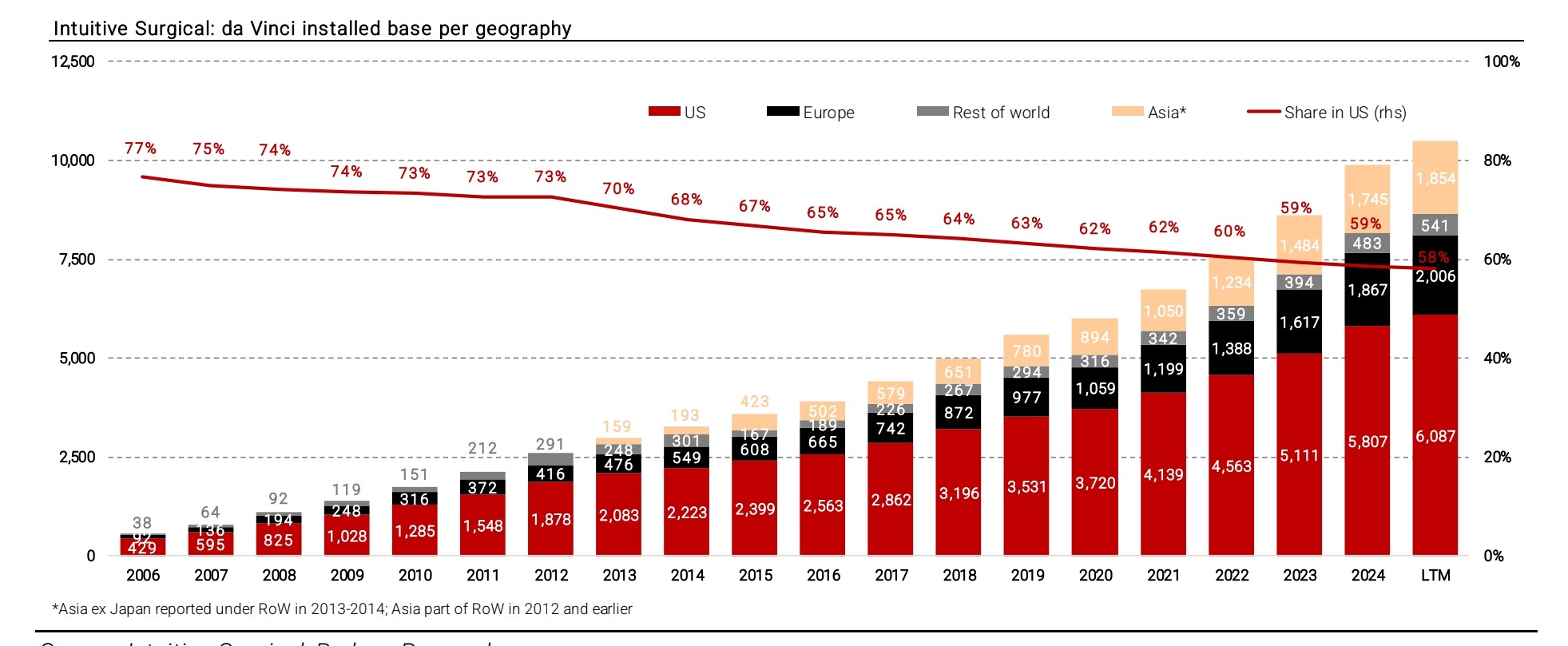

Intuitiven myyntiluvut kiinnostavat, koska ISRG on Surgical Sciencen suurin asiakas ja yhteistyötä yhtiöt ovat tehneet pitkään.

Ainakin osana jokaista ISRG:n myymää Da Vinci 5 - leikkausrobottia toimitetaan Surgical Sciencen kehittämä simulaatio- ja koulutusohjelmisto.

Aiemmissa malleissa softaa on ilmeisesti kaupattu loppuasiakkaille valinnaisena optiona. Tästä ja lisenssisopimusmalleista johtuen korrelaatio ISRG:n laitemyyntilukujen ja Surgical Sciencen myynnin välillä ei toki ole lineaarinen.

Kiitos tästä, en tiennyt.

Mielestäni on uskottavampaa että SSS löytää itsensä osana jotakin toista yritystä ajan mittaa, koska laitteiden väliset erot ovat niin suuria, että simulointia täytyy räätälöidä. Se mitä totesin laitteista näin yleensä edelleen pitää - simuloinnin käytöt ovat limittäisiä suhteessa varsinaiseen leikkaustoimenpiteeseen ja raudanvalmistajalla on aina optio tehdä itse. Tässä rajoite ei ole tekninen vaan asiakkaiden maksuhalu; parasta olisi jos asiakas hankkisi useamman järjestelmän, osan toimenpiteitä varten ja osan koulutus-, perehdytys-, ja leikkaussuunnitteluun.

Näkisin siis simuloinnit hyvänä niin kauan kuin länsimainen erikoissairaanhoito, etenkin Euroopassa, nähdään kustannuksena jota pitäisi vähentää.

En nyt ihan tarkkaan tiedä millaiseen mielipiteeseen päädyit tämän osalta, mutta tosiaan tosiaan ainakin ISRG näkee jotain järkeä tässä.

Largest customer Intuitive Surgical will roll out its cutting-edge da Vinci 5 surgical robot in 2025e and include simulation in all systems, increasing attach rate from c30-35% previously to 100%. Simulation for da Vinci 5 systems will be a purely subscription-based model,

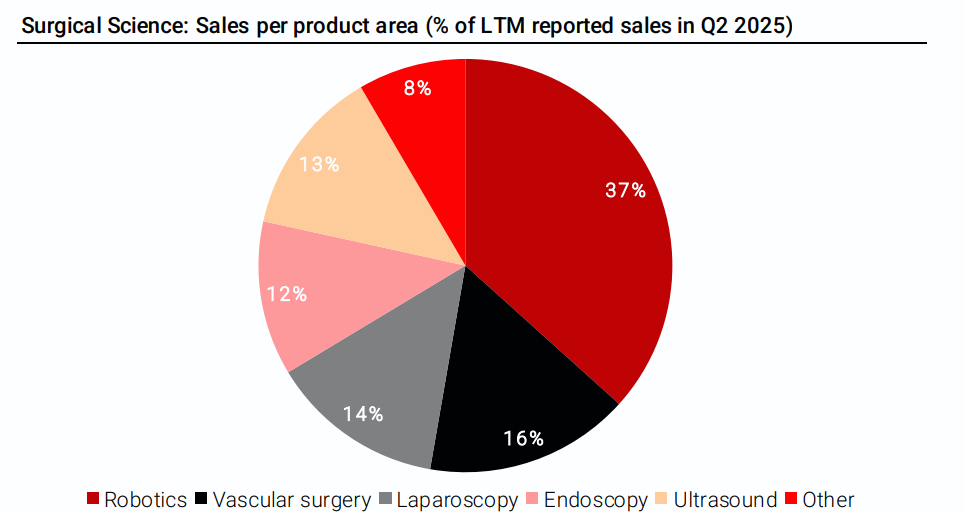

Firma on hankintojensa myötä kyvykäs tarjoamaan monenlaiseen segmenttiin:

We judge that Surgical Science currently holds a quasi-monopoly or oligopoly position in several niches of the medical simulation industry. Additional acquisitions may extend this position to further niches. Such a dominant position is an excellent position from which to extract high profit margins, but it could also breed complacency among incumbents. Potential complacency could lead to new challengers entering the space with innovative products, winning over key customers despite Surgical Science’s sticky customer relationships and high switching costs.

Q3, ehkäpä askel oikeaan suuntaan vaikka kannatavuus onkin vielä paineessa. CMD ensi kuussa.