Roni on täydessä vastuussa. Kävin kyllä seurannan aloitus -tapaamisessa kuuntelemassa SSH:n kuulumiset ja sparraillut Ronin kanssa tässä prosessin aikana keissiä. Mutta ihan mielenkiinnosta tulin nyt osallistumaan keskusteluun, koska haluaisin oikeasti ymmärtää osakkeeseen 3-5 euron tasoilla positiivisesti suhtautuneiden ajatuksia siitä, miten he näkevät SSH:n tulevaisuuden numeroiden valossa.

12 tykkäystä

Kysymykseni on miksi toisinaan on ja toisinaan ei ole - perustelua/luottamusta preemiosta analyysissa.

Esimerkkien kautta: Withsecure - DCF oli mitä oli ja rakennejärjestelyt sisäisesti, eikä skaalaus toiminut - siitä maksettiin preemio. Selvä miksi? Oliko se analyysin tavoitehinnoissa? Jos oli miksi ?

Qt pettää. Analyysit perustuu paljolti historialliseen kannan toipumiseen. Onko historiassa nähty DCF jotenkin varvempi kuin tulevaisuuden DCF potentiaalin arvioiminen? Miksi ?

SiloAi - olisiko sille saatu analyysin kautta koskaan sellaista DCF:n, että se olisi perustanut M&A hinnan ? Miksi ?

Tilanteet vaihtelee, ja halu ymmärtää miksi analyysi toisinaan on niin orjallisesti DCF.n lähellä kulkevaa, ja toisinaan taas ei?

4 tykkäystä

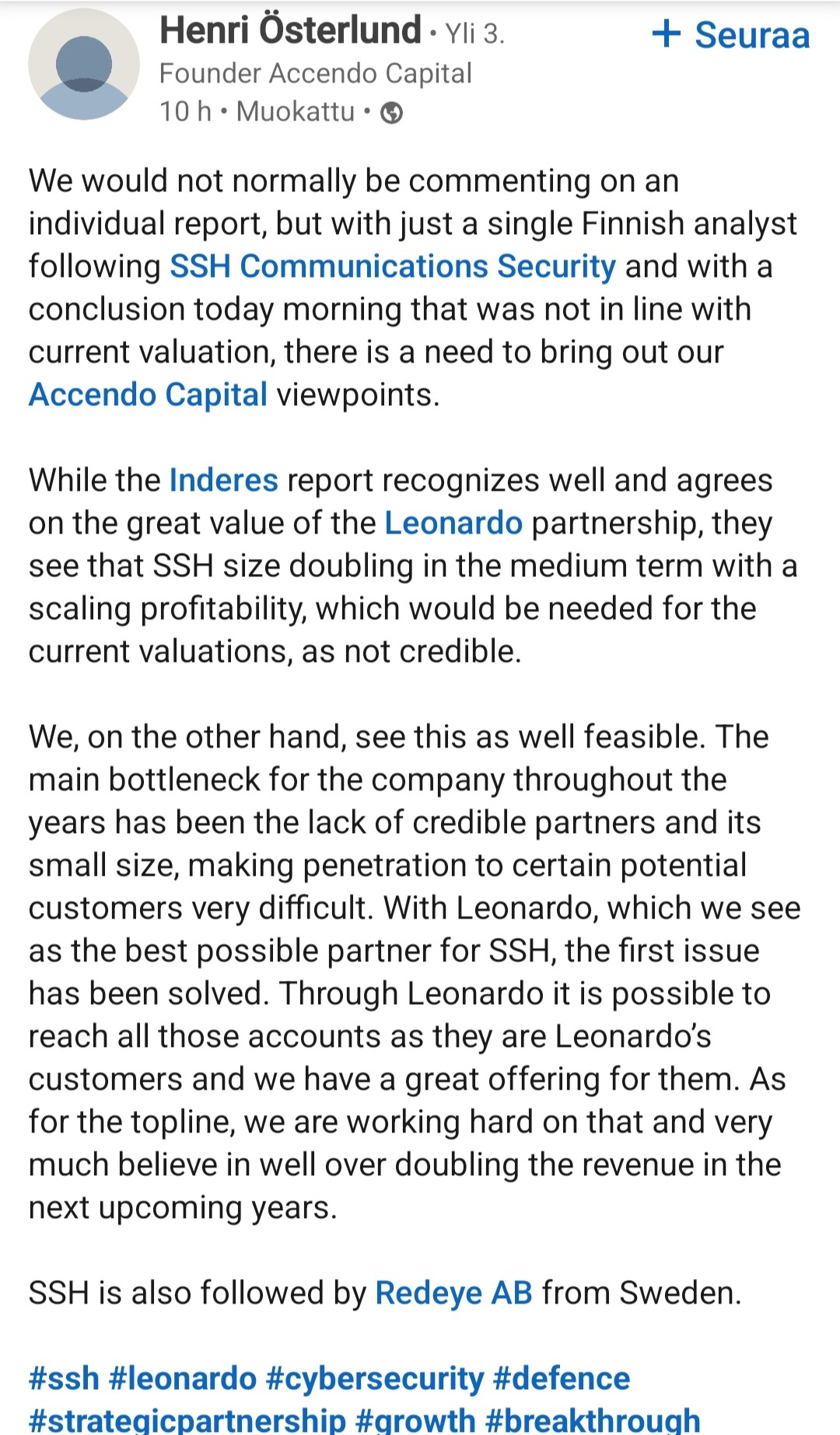

Leonardo integroi SSH:n Zero Trust -suiteen syvällisesti ja myy sitä valtiollisille asiakkaille, puolustukseen, NIS2-kriittisiin ympäristöihin.

Jos yksikin “referenssimaa” lähtee rullaamaan esim Italia, Saksa tai joku Nato organisaatio, niin KUVITTELEN, että liikevaihdon kasvu on 20% paremmalla puolella.

2 tykkäystä

Meidän analyyseissa tuodaan sanallisesti ilmi, mikäli ostotarjousta pidetään mahdollisena yhtiön X kohdalla, mutta lähtökohtaisesti analyysit tehdään siltä pohjalta, että yhtiö jatkaa itsenäisenä pörssissä.

Nuista nostamistasi esimerkeistä WithSecurea hinnoiteltiin pörssissä reilu 1x EV/S, kun luottamus kasvutarinaa kohtaan oli vuosien pettymysten jälkeen rapistunut. Ostotarjous tehtiin 2,3x EV/S-kertoimella, missä maksettiin jo jossain määrin tulevaisuuden kasvuodotuksista. SSH:n tapauksessa osakkeen EV/S-kerroin oli eilisen päätöskurssilla tälle vuodelle 7,8x eli odotuksia on leivottu hintaan jo moninkertaisesti verrattuna WithSecureen. Sitten jos toivot ostotarjousta vielä mehevällä preemiolla, niin arvostuskertoimenhan pitää nousta selvästi yli 10x EV/S, mikä tarkoittaa arvostusta, jolla vain hyvin harvoja yhtiöitä maailmassa hinnoitellaan. Mutta olen kyllä kaikkien SSH-omistajien kannalta hyvin iloinen, jos tämä yrityskauppaoptio lähivuosina realisoituisi ja yhtiöstä maksettaisiin vielä merkittävästi nykyarvostusta enemmän.

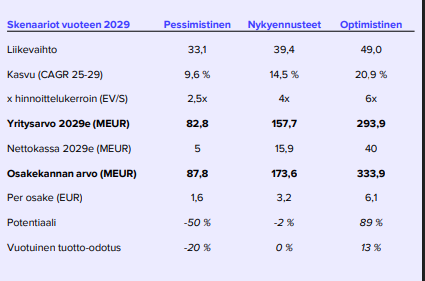

Roni oli raportissa myös hahmotellut skenaariota, missä SSH:n liikevaihto kasvaisi reilu 20 % vuodessa vuoteen 2029 asti ja tuossa vaiheessa osakkeelle hyväksyttäisiin edelleen korkea 6x EV/S-kerroin. Silloin osakkeessa on nousuvaraa, mutta se vaatii huippusuoritusta ja arvostusta tulevina vuosina. Onko riski-tuottosuhde riittävä, että tähän skenaarioon kannattaa nojata, se on jokaisen itse määriteltävissä.

16 tykkäystä

Näillä euroopan puolustusbudjeteilla, ja yhteiskunnan kriittisten tarpeiden suojaamisen tarpeet on vasta euroopan jälkiherännäisyyden (kiitos USAn herättelyn) myötä niin lähtökuopissaan, niin miksi LV ei lähtisi rullaamaan ++20%. Ottaen huomioon vielä omistusjakauman (ts. suuret inst. omistajat vähissä) vrt. vaikka kuutti (ts. inst. omistajat laajasti edustettuina), niin joskun homma lähtee rullaa, kulkee peemion odotuskin omilla tasoillansa, se me tiedetään kaikki ilman DCF perustetta.

Tietty homma on nyt SSH:n hallituksen, tj. Raulaksen sekä Leonardo yhteistyön käsissä tuleeko tästä odotuksesta timanttia💎 vai tuhkaa😂. Katellaan.

Vaikka en nyt osaketta omista, niin sehän olisi iso plus ja ovat kovin luottavaisia tulevaisuuden suhteen, jos SSH taas suostuu maksamaan näistä analyyseistä. Eikös ne hermostunut aikaisemmin niihin myy suositukseen ? Tai sitten Leonardo vaati, ajatuksena , että saavat koko firman halvemmalla, kun on myy suositus päällä ?

3 tykkäystä

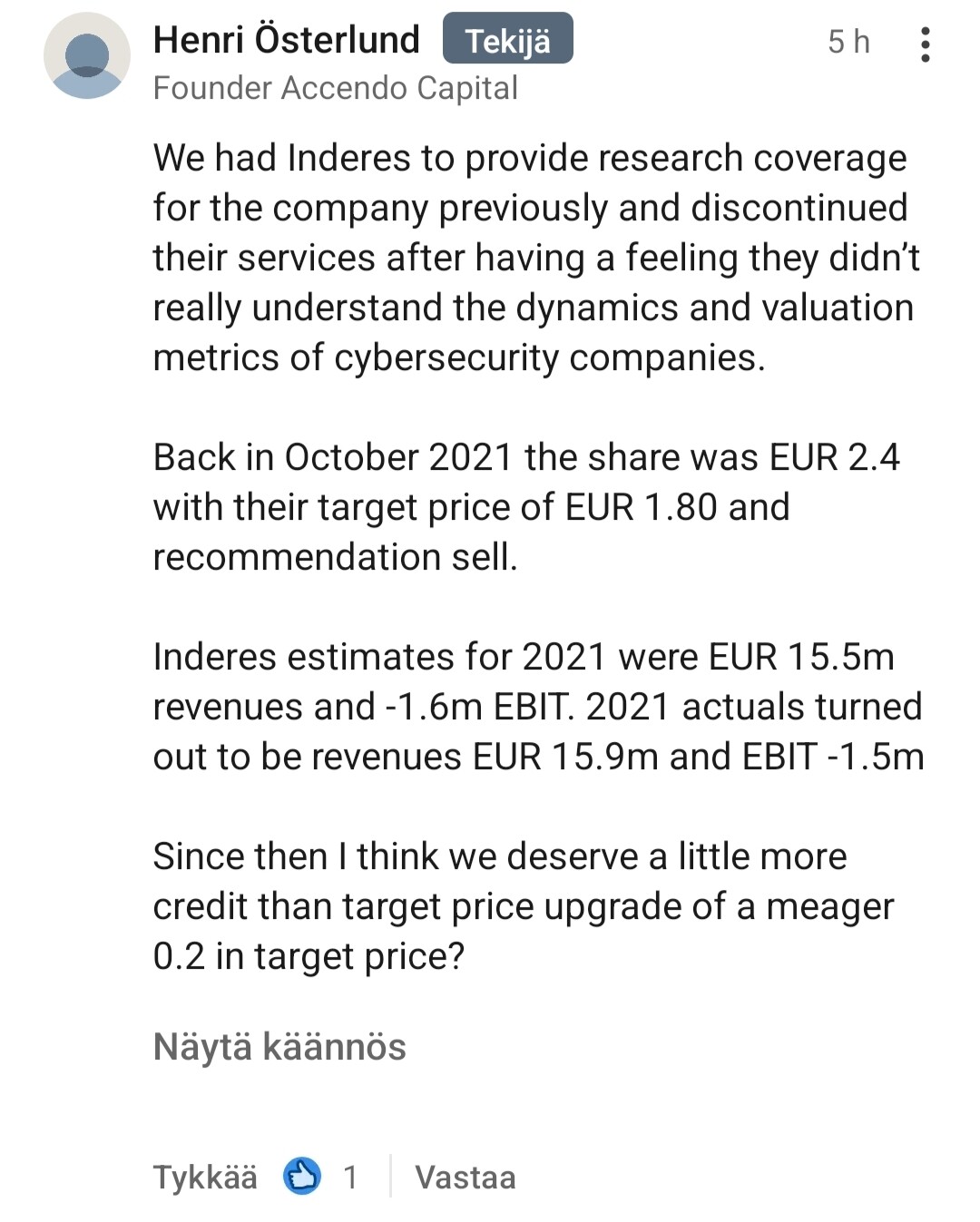

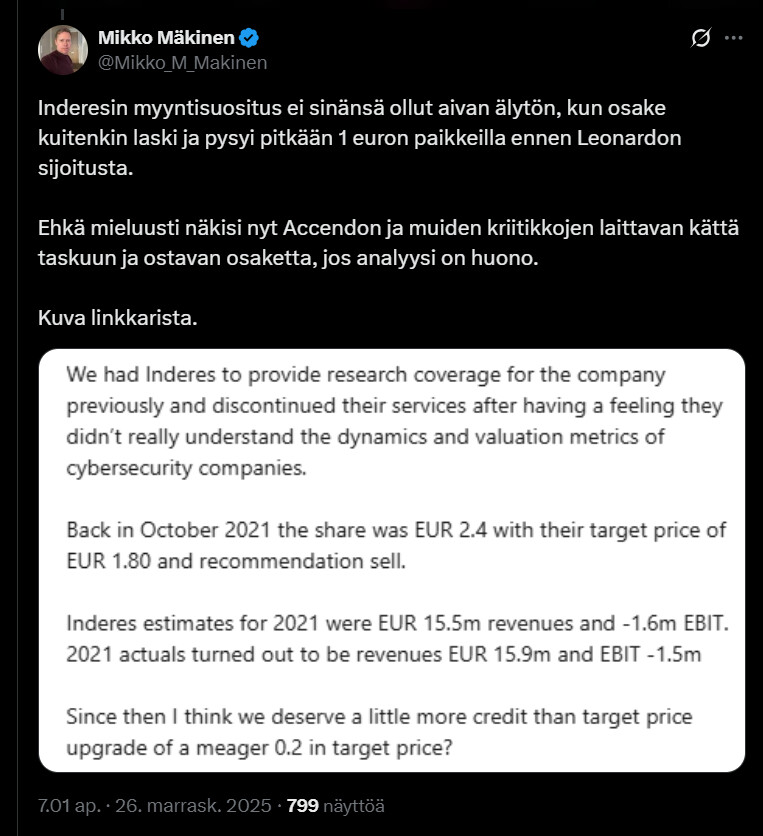

Kyllä tyhmyyden huippu SSHn johdolta ostaa analyysi samalta yhtiöltä, joka ’edellisellä kierroksella’ nuiji raportillaan yhtiön kurssin puoleen (kahdesta eurosta yhteen), ja kurssin pysyneen euron tasolla ever since Leon ostoon asti. Olettivatko SSHlla, että nyt tulee samoilta kavereilta bullish raportti jollain 10€ tavoitehinnalla. Give me a break ![]()

Yhtiö olisi 10x arvokkaampi jos se olisi listattu jenkkeihin, imo. Liikevaihto on vielä niin matalalla tasolla, että sen tuplaaminen verrattain nopeasti ei ole mikään temppu, jos puolustusteollisuus vetää. Ja siihen voi sitten lyödä kivan kertoimen kasvulle ja hottis toimialalle, niin ollaan jossain 500m€ arvostuksessa helposti, kuten Olli Viitikkokin jossain haastattelussa maalaili.

6 tykkäystä

Seurantamme päättyi edellisen kerran 30.12.2021, jolloin kurssi oli seurannan lopetus raportin mukaan 3,05€. Kyllä se taisi olla markkina itse joka nuiji kurssin euroon.

Hieman eri mieltä liikevaihdon tuplauksen helppoudesta. Toki keskipitkällä aikavälillä toivottavasti näin käy, sillä kyllähän tuo arvostuskin sitä edellyttää. Jotta tuo nykyisestä arvostuksesta 10x korkeampi arvo olisi perusteltu ei liikevaihdon tuplaus riittäisi arvostusta perustelemaan alkuunkaan. Eiköhän yhtiön hallitus olisi asiaa selvitellyt enemminkin, jos jenkeistä saisi arvostukseen helposti 10x.

19 tykkäystä

Tästä kyllä täysin samaa mieltä. Jos Leonardo-integraatio onnistuu edes kohtalaisesti: PrivX + NQX myynti eurooppalaisille valtiotoimijoille, EU:n NIS2- ja PQC-regulaatio ajaa kysyntää, Yksi iso sopimus → SSH +20–40 % hetkessä. Koen tämän scenaarion ihan muuna kuin “huippusuorituksena”, enemmänkin rakenteellisena seurauksena.

6 tykkäystä

Vaan no hätä oli niin tai näin, tämähän on sitten enempi mahdollisuus päästä mukaan ja kuten jäljempänä "@monistuskone maalaili, niin se tarvitsee vain merkityksellisen tilauksen/infon ja ollaan eri tasoilla.

On myös mahdollista päinvastoin, että koska SSH:n johto hyvin tiesi jo kokemuksestaan Inden aikaisemmankin “ei tulevaisuutta” katsontakannan, niin saattaa olla, että ajoittivat laajan raporttitilauksen tähän saumaan eli kovaa maata on jalkojen alla. SSH:n johto osoitti Leonardo saavutuksellaan osaamista.

Eikä 35-40% LV:n kasvu ole mikään juttu, joskun homma lentää. Ajatella, jos SiloAI tai Woltti ois tilannu itsestään analyysin - siinä olisi DCF ja arvostus lyöneet ![]() kättäpäälle:gem_stone:. On nää ihmeellisiä juttuja.

kättäpäälle:gem_stone:. On nää ihmeellisiä juttuja.

1 tykkäys

Inderesin analyysi on todella laadukas ja syväluotaava. Analyytikko porautuu uskomattoman moniuloitteisesti yritykseen luoden sijoittajalle tarkan kuvan yrityksen menneisyydestä, nykytilasta ja tulevaisuudesta. Tällä hetkellä markkina ja analyytikko ovat hyvin erilinjoilla yrityksen arvosta, mutta vastaan väittämättömästi tulee perustelluksi, että markkina on ollut väärässä. Tämän voi selvästi havaita EV/S kertoimista ja DCF-laskelmasta.

Seuraavaksi jäämme odottamaan kasvutarinan etenemistä kentän laidalta. Leonardo sijoitti tähän 1,5 euron osakekohtaisella hinnalla, joten tästä ei kannata tämän enempää odottaa. Näin se on nähtävä, sillä mitään vastaväitteitä en ketjussa näe.

Kiitos analyysista ja hyvää syksyn jatkoa foorumille ja etenkin foorumin hygieniasta vastaaville.

15 tykkäystä

Vähälle huomiolle jää puolustusteollisuuden ja turvallisuusalan yleinen ilmapiirin muutos, josta on selvästi aistittavissa, että valtion ja erityisesti puolustusvoimien kanssa yhteistyötä tekevät alan keskeiset yhtiöt saavat nyt aidosti markkinoida ja myydä.

Olen ehdottomasti sitä mieltä, että SSH olisi jo myyty aikapäiviä sitten, jos valtio olisi siihen suostunut. Yhtiö on kuitenkin niin keskeinen toimija maanpuolustuksen kannalta, ettei tähän ole mahdollisuuksia. Tämä Leonardon mukaan tulo oli jo aivan totaalinen yllätys, mutta oikeastaan vain vahvisti tuon epäilyn. Kun ei kokonaan saanut, niin edes jotain.

Myynti ja kasvu sakkaa samasta syystä. Eihän koko yhtiöstä saa edes puhua. Kun vapaaehtoisessa harjoituksessa kysyy täsmäkysymyksen yhtiöstä keskustelut ovat loppuneet siihen. Nyt tilanne on kuitenkin muuttunut. Uusi kansainvälinen sijoittaja tuo yhtiön, sen tuotteet ja tekemiset näkyviksi kaikille, mikä kyllä laittaa myyntiin vauhtia.

Tähän saakka valtiolle on sopinut aivan mainiosti kehittää ja käyttää parasta ja sen parempi mitä vähemmän ihmiset tietävät.

Näitä aspekteja analyytikon on tietysti mahdoton mitata, analysoida ja lyödä raportille tavoitehintaan. Mutta sen toki kaikki tietää, että jos sijoituspäätöksen tekee toteutuneiden lukujen perusteella ollaan kaikki yhtä köyhiä jatkossakin.

4 tykkäystä

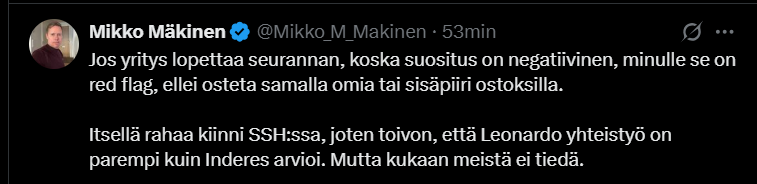

Hallituksen puheenjohtaja on avannut sanaisen arkkunsa LinkedInissä. Harvemmin on kyllä sattunut omaan silmään, että hallituksen puheenjohtaja ottaa näin kantaa analyysiin. Onneksi ennusteet ovat lopulta vain ennusteita, ja yhtiö saa nyt ‘ampua alas’ nämä “varovaiset” ennusteet omalla tekemisellään. Kyllä se arvostus sitten seuraa perässä ![]()

24 tykkäystä

Luonnollisesti tällaista toteamusta pitäisi seurata sisäpiirin osakeostot laajalla rintamalla, ja miksei myös omien ostot ja mitätöinnit.

Muutenhan tuo on vain noloa; kun se voisi olla myös omistaja-arvoa luovaa (mikäli Österlund aidosti uskoo mitä kirjoittaa), ja noloa.

30 tykkäystä

Perinteisesti ollut huono merkki, kun yhtiön johto tai sisäpiiri ottaa kantaa osakekurssiin. Kuten edellä todettiin, jos osake on aliarvostettu, kättä taskuun vaan.

Put your money where your mouth is.

43 tykkäystä

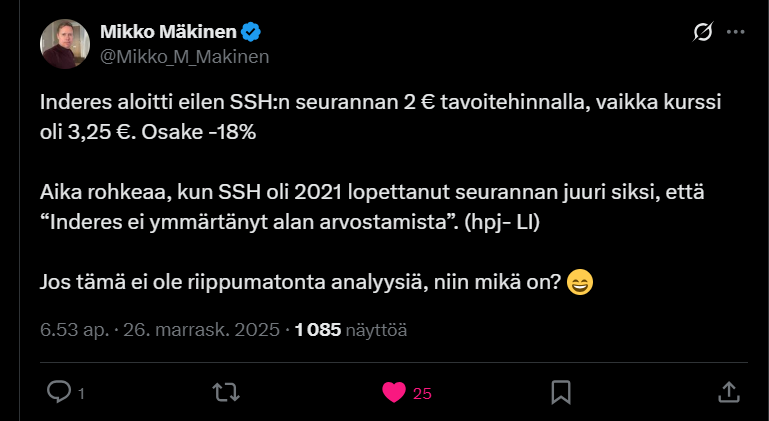

@Mikko_Makinen on tehnyt pienen ja hyvän “tviittiketjun” aiheesta ![]()

https://x.com/Mikko_M_Makinen/status/1993543621581455507

41 tykkäystä

Noniin, nyt on Henri Österlund myös ostanut itse 2500kpl SSH:n osakkeita.

15 tykkäystä

1,7 prosentin lisäys entiseen määrään mutta on se jotain!

5 tykkäystä

Aika pieni kannanotto.. 50K osto ois vähän luottamusta herättänyt, tämä muutaman tonnin oston ois ollut sama jättää tekemättä.

Jos julkisesti kehtaa ottaa kantaa kurssiin, niin näyttäisi nyt sitten kunnolla myös lompakollaan missä mennään.

Edit. Tai nyt hän näyttää todella missä mennään. . Touhutonneilla kun ostaa, niin ei taida paljoa luottoa löytyä tällä kurssinhinnalla. Hänellä se paras tieto on ![]()

21 tykkäystä

Poikkeuksellista kommentointia Österlundilta, sijoitusviihteen kannalta mukava seurata.

Mutta, jos ihan tarkkoja ollaan, niin ei kai Österlund missään vaiheessa ole sanonut, että nykyinen osakekurssi olisi halpa, jolloin “put your money where your mouth is” ei ihan toimi. Ymmärtääkseni on vain narissut Inderesin target pricestä.

1 tykkäys