A couple of updates, very different views from industry professionals, although both are naturally above today’s price:

DNB: 90 → 100 SEK (9.38 EUR) & Buy

Credit Suisse: ?? (Outperform) → 57 SEK (5.35 EUR) & Neutral

however, on Credit Suisse’s own website, the previous target was 51 SEK & Hold

2022-02-22 08:59

STOCKHOLM (Nyhetsbyrån Direkt) DNB Markets raises its target price for SSAB to 100 kronor from 90 kronor. The buy recommendation is reiterated.

Can anyone explain how much SSAB’s share of the profit is from this material, which is currently sure to sell, or which companies use it in their own products?

SSAB’s stock price has performed well—so far—throughout the Ukraine crisis.

The company, which has become net debt-free, may also be influenced by its 2022 P/E ratio of 4-5, as well as restrictions on steel imports from Russia/Ukraine. The dividend of SEK 5.25 (approx. EUR 0.5) is still attached to the stock.

Of course, the communicated SEK 45 billion investment in the transition to CO2-free production, as well as the potential cut in the EU’s free carbon emission allowances in 2025-2030, still loom as shadows. The company has also not been able to communicate the pricing power of carbon-free steel other than that demand is good and some premium will apply initially.

2022-03-02 08:57

Index calculator Qontigo is implementing changes to the Stoxx Europe 600 Index. The changes will take effect before the market opens on March 21, according to a press release.

For Sweden, this means that SSAB B will be included while Afry will be removed.

Among other changes, it can be noted that Norway’s Kongsberg Gruppen will be included.

A pretty good summary of SSAB’s situation. But I disagree that the investment program is some kind of shadow. I mean, often in Finland companies are criticized for not investing.

Do you mean that the investment in green steel would be a bad investment? In that case, the other issue you mentioned, i.e., emission allowances, shouldn’t be a problem, meaning they wouldn’t be tightened if green steel isn’t needed. You can’t have both.

A significant amount of money will be spent on CO2 investments

These investments will not generate additional returns, meaning it will not be possible to achieve a better price in the market.

Currently free emission allowances are being phased out, and new ones will have to be acquired from the market at rising market prices. This could happen even before carbon-free steel is technically possible on a large scale, or before it’s possible through the availability of CO2-free electricity.

Carbon tariffs have been discussed, meaning importers of steel into the EU would also have to acquire emission certificates. In reality, an importer could bring the “clean” part of their production into the EU without certificates, and leave their “dirty” production elsewhere in the world. China’s target was, if I recall correctly, 2050, and India’s 2070…

SSAB spoke of “Cost Avoidance” of SEK 7 billion/year from 2030 onwards if emission quotas had to be purchased entirely from the market at today’s price of EUR 90/t.

So, these investments must be made, but whether they will ultimately be good business for SSAB or not is a bit unclear. It is also clear that customers are more than interested in carbon neutrality.

It’s good to remember, of course, that some of these green investments would have been necessary anyway in the early 2030s, as blast furnaces also need to be renewed. This means that the production machinery is very fresh/renewed, which reduces CAPEX needs in the 2030s.

NOTE! The flip side of the risk is opportunity, meaning pricing power will emerge and trade will be conducted with a premium that at least covers the extra costs, or more.

And SSAB’s starting point is by no means the weakest among steel companies…

production volumes of new fossil-free products relative to demand and compared to old technology and demand

It is worth noting that when moving to fossil-free steel, steel production volumes may geographically decrease, but demand may even go in the opposite direction. Steel itself is an excellent material, and with it, environmentally friendly steel is, in my opinion, an almost perfect material.

As you mentioned, investments must be made, and I suspect the same will happen in Europe as in the paper industry, meaning total production volumes will decrease with the transition. What happens to demand is, in my opinion, a very essential question.

I’ve been thinking that as long as politicians keep environmental issues on the agenda, the return on investments is somewhat guaranteed. In other words, costs can be passed on to customers. Loopholes for Chinese importers can be closed. For example, selling black steel elsewhere has already been widely discussed, and I’m sure that can also be prevented or taken into account in customs duties.

In addition, a turnaround in steel prices has not yet been seen, so it could be quite realistic to achieve an EBITDA of 1.5-2 billion in 2022. That’s over a third of the investment need, which was estimated to last until 2030. So, for the years 2023-2030, there would be perhaps 2.5-3 billion “to be earned,” which no longer sounds very extreme (300-400 million EUR/year).

Of course, if steel prices start to fall and the business becomes unprofitable again, the owners will ultimately pay for it, but so far so good.

It’s unclear to me how badly the potential electricity and energy crisis, possibly caused by Russia sanctions, would affect SSAB’s operations and profitability?

In the long run, the cost of proactive environmental friendliness is now a concern. Investment costs can be defended by arguing that they will be incurred in one form or another anyway, but there are now many uncertainties related to energy prices and availability.

“When we do all production with hydrogen reduction and by using recycled steel, our electricity consumption would increase an estimated 6–7-fold.”

I personally sold my remaining SSAB shares because the share price curve shows a bit of dividend fever, and in my opinion, in the long term, the stock has many risks compared to more defensive stocks. The current phase of the cycle is also, of course, a worry.

SSAB doesn’t use electric arc furnaces on a large scale yet, but rather coke and coal. So, the price of electricity won’t significantly impact their profit until years from now, and even then, only if the cost cannot be passed on to end customers. The price of electricity also increases competitors’ costs, so why would they sell at a loss?

A downturn in the cycle is a big risk, but the current geopolitical situation, in my estimation, supports the persistence of high prices (steel is needed, imports from Ukraine and Russia are stopping).

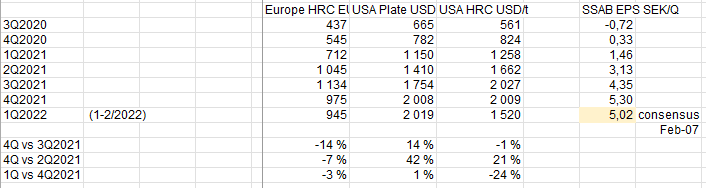

If the Q1 report confirms promised results similar to Q4 figures, and perhaps guides a flat Q2, then an operating profit of almost EUR 1.5 billion will already be made during H1.

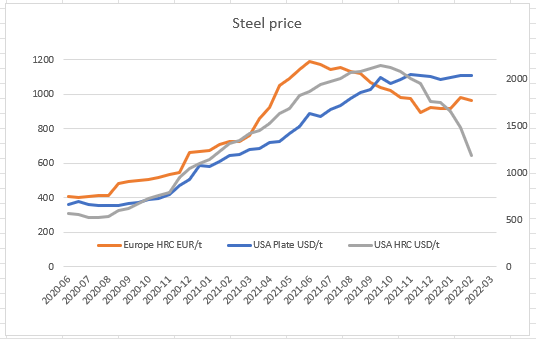

I updated the Steel Benchmarker data for steel curves

Looking at the history:

The European (40%+ SSAB) HRC spot reference peaked last summer, and since then the price level has stabilized at 900-1000 EUR/t (HR Coil). Of course, SSAB sells more refined products in this segment than HR Coil.

USA (20%+ SSAB) Plate, on the other hand, continued its rise and has since stabilized at just over 2000 USD/t, even though the USA HR Coil reference has dropped significantly. SSAB’s US production is Plate, not basic coil products.

Special steels (20%+ SSAB) have their own price levels agreed upon with customers.

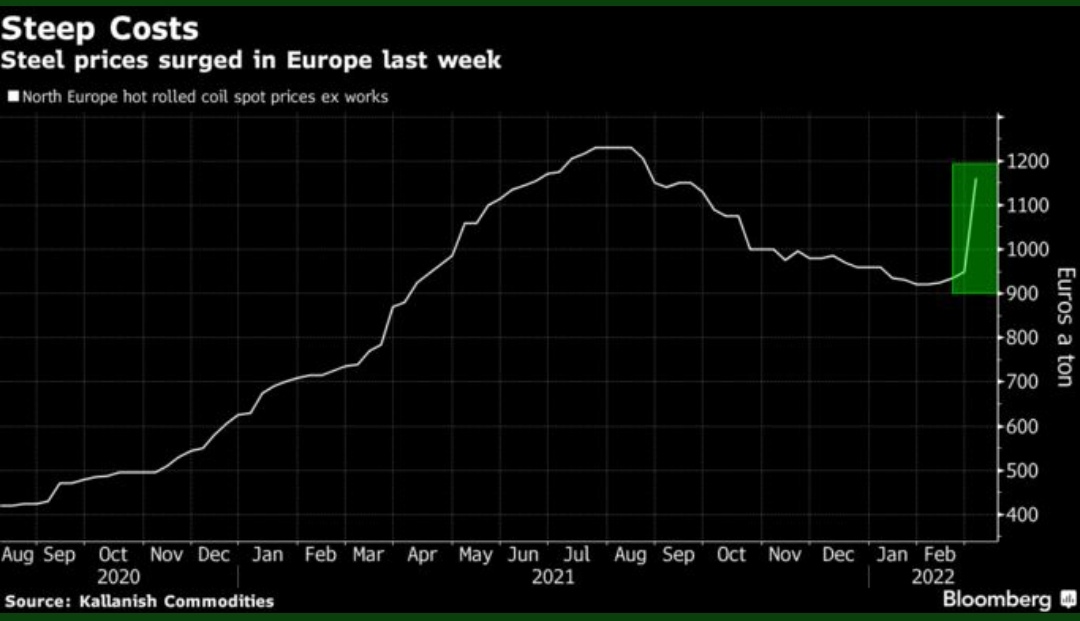

Now that Russia/Belarus/Ukraine have practically dropped out of the steel market unexpectedly for an indefinite period, European HRC offers have clearly risen to around 1150 EUR/t, close to last summer’s peaks.

It’s also good to note and weigh:

2022 annual contracts are, by all accounts, clearly better than those agreed for 2021.

During the autumn and this year, input factors such as energy have also risen. Ukraine has also pushed up iron ore prices, coking coal has increased, etc.

One blast furnace in Raahe is down (for repair), as SSAB announced. However, the impact is limited (cf. estimated 60 MEUR / 5.8c/share loss vs EPS 4Q=0.52 EUR).

The war creates uncertainty on the demand side. On the other hand, there’s demand from the slowly recovering automotive sector due to semiconductor bottlenecks, the impact of infrastructure packages is only on the horizon, green transition (even accelerating) investments, etc.

SSAB has its own safety net, as there is a lot of production not only in Finland, but also in Sweden & USA.

Time will tell how the stock price fares, but YTD +22.5% in my portfolio (-10%) in its class.

How easy is it to acquire that kind of iron ore from elsewhere? One would think that SSAB could get a fairly good replacement from Sweden’s own mines, meaning they would still be in a better position than competitors in this regard. But how does Raahe compensate if they can no longer get it from there?

More than anything, the article gives me the feeling that prices will rise, and this will be reflected in SSAB’s numbers. But I guess turbulence could mean a sharp/unexpected upward trend?

At least according to this, Russia’s iron ore procurement has ceased without affecting SSAB’s production.

SSAB’s ore needs are marginal on a global scale, but how the price will ultimately develop when Russia/Belarus/Ukraine are on the market remains to be seen.

Hopefully, the annual contracts will account for these and other raw materials in some way if a major change occurs.

One more thing about the previous point: iron ore is now at the same level as at the beginning of 2021, i.e., 150 USD/t. However, it’s an increase from the 115 USD/t level at the turn of 2022.

Iron ore prices refer to Iron Ore Fine China Import 63.5 percent grade Spot Cost and Freight for the delivery at the Chinese port of Tianjin

Will that Russian iron ore now go to China, India, Indonesia, etc.? Russian raw materials are likely to be sold at steep discounts to those who will take them.

SSAB states that electricity is procured from the spot market to a lesser extent, with a limited impact and no effect on production. Rising energy costs affect overall costs, and European market prices have increased.

SSAB: LIMITED IMPACT FROM ELECTRICITY PRICES, NO PRODUCTION STOPS PLANNED - PC

Friday, March 11, 2022, at 4:13 PM

STOCKHOLM (Nyhetsbyrån Direkt) SSAB buys a smaller share of its electricity directly from the spot market, so short-term fluctuations in electricity prices have a limited effect on the steel manufacturer.

“Today, we have no plans for production stops; instead, we are running as planned. Rising energy prices mean increased costs. How this affects profitability then depends on how steel prices develop, and steel market prices in Europe have risen in recent weeks,” states the Swedish steel company’s press officer.

It will be interesting to see how SSAB manages to navigate the framework of high costs and high prices. Last year, SSAB’s prices and thus margins reacted significantly faster than Outokumpu, in my opinion, so it might be that SSAB does not have any extremely long supply contracts and reacts to the situation relatively quickly. If this is the case, there could still be several very profitable quarters ahead.

If the contracts do not commit to anything else, all rising production costs below can be fully passed on to customers when demand is strong.

The price increase has been steep since the start of the Ukraine crisis, and I would think that profitability should hold up at these prices, even with rising costs.

In addition, Ukraine and Russia will be absent from the European steel markets for a reasonably long time, so I would expect good times for the remaining steel producers?