-It’s more about image politics, which I think is only a good thing. Why would a pioneer’s cost be higher? For example, several modern electric-heated (instead of gas) blast furnaces are already in use globally, and it’s not “rocket science” nor particularly expensive.

P.S. Now that more electricity transmission capacity has been established between Sweden and Finland, it would be essential to get the Pyhäjoki power plant construction project moving; it could also provide energy to SSAB’s factories on the Swedish side.

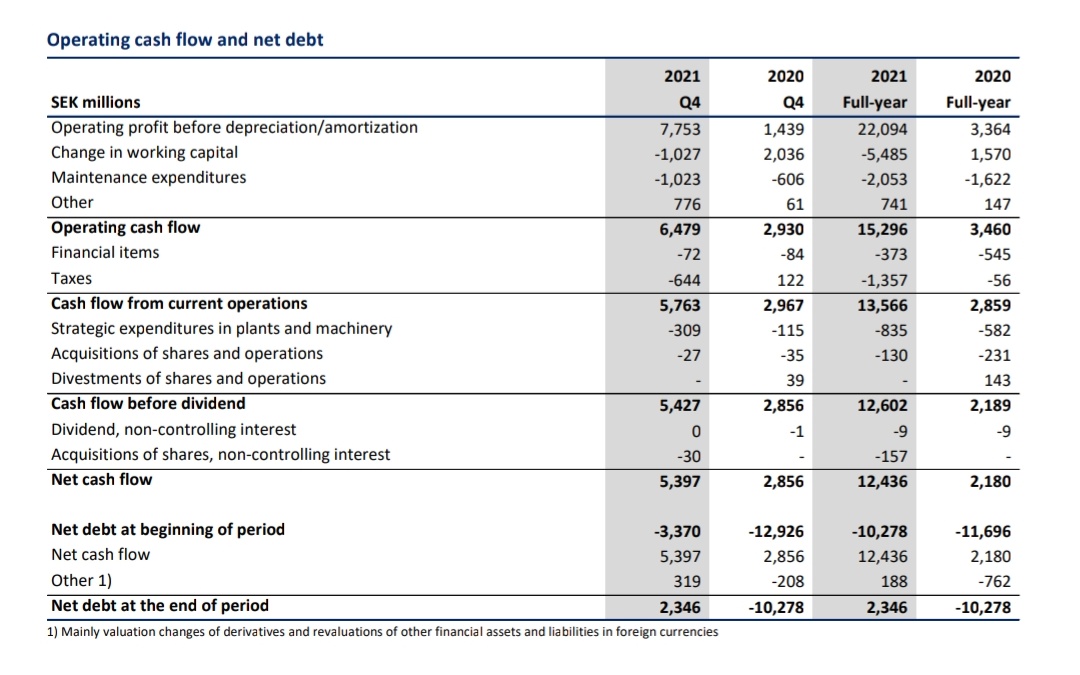

There are the figures for Maintenance / Strategic expenditures, which are used to maintain capacity and develop new products. A total of just under SEK 3 billion last year.

When I looked at the image in the previous post, visually it looks like the SEK 45 billion bar is part of a total bar of approximately SEK 100 billion for Maintenance + Strategic combined.

So, an extra SEK 2 billion, or EUR 190 million/year, meaning an extra cost of EUR 0.185 / share for the next 23 years.

However, the SEK 50 billion will be spent this decade, so the money will be front-loaded. Blast furnaces would have been replaced anyway, but no one’s DCF calculations have remembered that.

It’s a shame that SSAB didn’t open this as a cash flow roadmap; they themselves created unnecessary uncertainty and confusion.

The investment program is quite good if only the earnings level could be maintained. Otherwise, it will be difficult.

Finns are often accused of paying dividends when they don’t see investment opportunities. SSAB management clearly sees them now, and if a small investor trusts management’s assessment, then it’s worth being involved.

If, by chance, 2022 were to be like its brother 2021, then the first SEK 15 billion would be accumulated for investments.

OP, unsurprisingly, maintains its bullish outlook.

Buy recommendation and target price of €6.80 (SEK 70.00) remain unchanged.

Brief summary:

The demand environment has not changed significantly, so the outlook is bright. Q4: revenue 2% better than consensus and adjusted EBITDA 10%. OP expects Q1 results to be on par with Q4 results.

Behind the investment plan is strong customer demand. This has no impact on dividend policy. The dynamics of the steel market have changed compared to before.

The German bank, on the other hand, lowered its target price, presumably as a result of the communicated investment program.

EDIT: Handelsbanken also lowers its target price.

I will add others as I encounter them.

2022-02-01 08:54

STOCKHOLM (Nyhetsbyrån Direkt) Barclays Capital lowers its recommendation for SSAB to Equalweight from Overweight. The target price is lowered to 63 from 66 Swedish Kronor.

2022-02-01 06:42

OP Corporate Bank raises SSAB’s target price to 71.20 Swedish Kronor (70), reiterates Buy - BN

2022-02-01 06:42

Goldman Sachs raises SSAB’s target price to 69 Swedish Kronor (67), reiterates Buy - BN

2022-01-31 09:55

DNB raises SSAB’s target price to 90 Swedish Kronor (75), reiterates Buy - BN

2022-01-31 07:10

STOCKHOLM (Nyhetsbyrån Direkt) Deutsche Bank lowers its recommendation for SSAB to Hold from Buy. The target price is lowered to 59 from 64 Swedish Kronor.

2022-01-31 08:11

Handelsbanken lowers SSAB to Hold (Buy), target price 50 Swedish Kronor (60)

STOCKHOLM (Nyhetsbyrån Direkt) SSAB’s Chairman of the Board Lennart Evrell has bought 20,000 shares in the company, according to Finansinspektionen’s transparency report. The shares were purchased on January 31 at a price of SEK 48:63, or a total of close to SEK 1 million. SSAB’s website states that Lennart Evrell already owns 20,000 SSAB shares, according to a listing as of April 2021

SSAB Rises to Investment Grade with S&P. This will likely reduce borrowing costs, even though net indebtedness is now a thing of the past.

SSAB (MW): S&P late Friday upgraded the company’s BB+ rating to BBB-/Stable, which means that SSAB again fulfills the requirements for an investment grade rating.

SSAB : Unplanned production outage in Raahe, affects first quarter results

One of SSAB’s blast furnaces in Raahe, Finland has been affected by an unplanned outage. Repair work is expected to last throughout February and SSAB Europe’s first quarter 2022 earnings are expected to take a SEK 600 million hit.

One of the blast furnaces at SSAB’s steel mill in Raahe, Finland has been shut down for repairs. Repair work is expected to last throughout February after which it is expected the blast furnace can be restarted. The outage will result in lost production and shipments, as well as repair costs. The earnings of SSAB Europeare expected to be impacted negatively by around SEK 600 million in the first quarter of 2022. SSAB will make every effort to minimize the negative implications for customers.

It is estimated that CO2-free direct reduced iron (sponge iron) will be produced and imported from Sweden. The number of employees at the Raahe plant would decrease from approximately 2500 to a range of 700-1100. Well, it doesn’t matter from the company’s perspective.

After the reform, Raahe might not have all the current production stages. Hydrogen reduction may be carried out elsewhere, and the final product of the reduction, direct reduced iron (sponge iron) used as raw material, will be imported for processing in Raahe’s electric arc furnaces from Kiruna, Northern Sweden.

If not all current work stages were needed, the factory would shrink. The Raahe steel mill employs approximately 2,500 people. In the future, the number of employees could be somewhere between 700 and 1,100.

-In those processes and facilities that require large investments, there is a phenomenon where maintenance costs begin to be minimized at an early stage when closure is known, and if it breaks down prematurely, it is no longer repaired for reuse but completely shut down. One could confidently say that if both blast furnaces were decided to be shut down in 2030, at least one of them would certainly have been shut down by 2028 for the aforementioned reason. For example, the regular renewal of the blast furnace’s inner lining is an expensive affair; the entire inner shell must be manually inspected, and bricks and so on replaced. This would not be done at all if, when the need for maintenance arises, the remaining operating time of the blast furnace were short.

Cyclical companies must be valued using different valuation levels and metrics; you can find more on the topic in this discussion or in Petri’s excellent thoughts published yesterday, in the Outokumpu discussion.

Outokumpu can be considered a relatively good benchmark for SSAB.

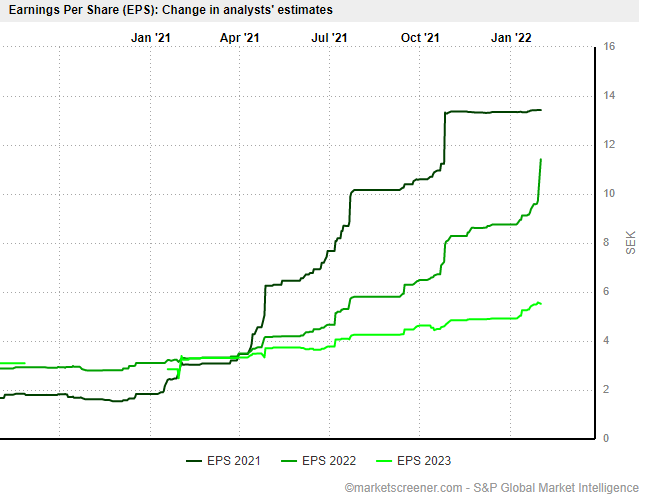

based on their estimates for EBITDA increase in 2022 & 2023, they raise +50% for 2022 and +40% for 2023 respectively

For reference, SSAB’s 2021 figures. Perhaps Kepler refers to “rörelseresultat” as “rörelseresultat före avskrivningar” i.e. EBITDA (earnings before depreciation and amortization). 2021 22.1 billion SEK yielded 14.24 SEK/share (1.35 EUR/share), so something should remain under the line from Kepler’s 20.7 billion SEK (2022) and 17.5 billion SEK (2023).

If the 2021 EPS (1.35 EUR) is cut in proportion to Kepler’s EBITDA calculation, the 2022 EPS would be -6%, or 1.26 EUR, and the 2023 EPS would be -21%, or 1.07 EUR. Well, maybe it can’t be done like that, but it’s a calculation.

The translator says:

Uncertainty about sheet prices in the United States

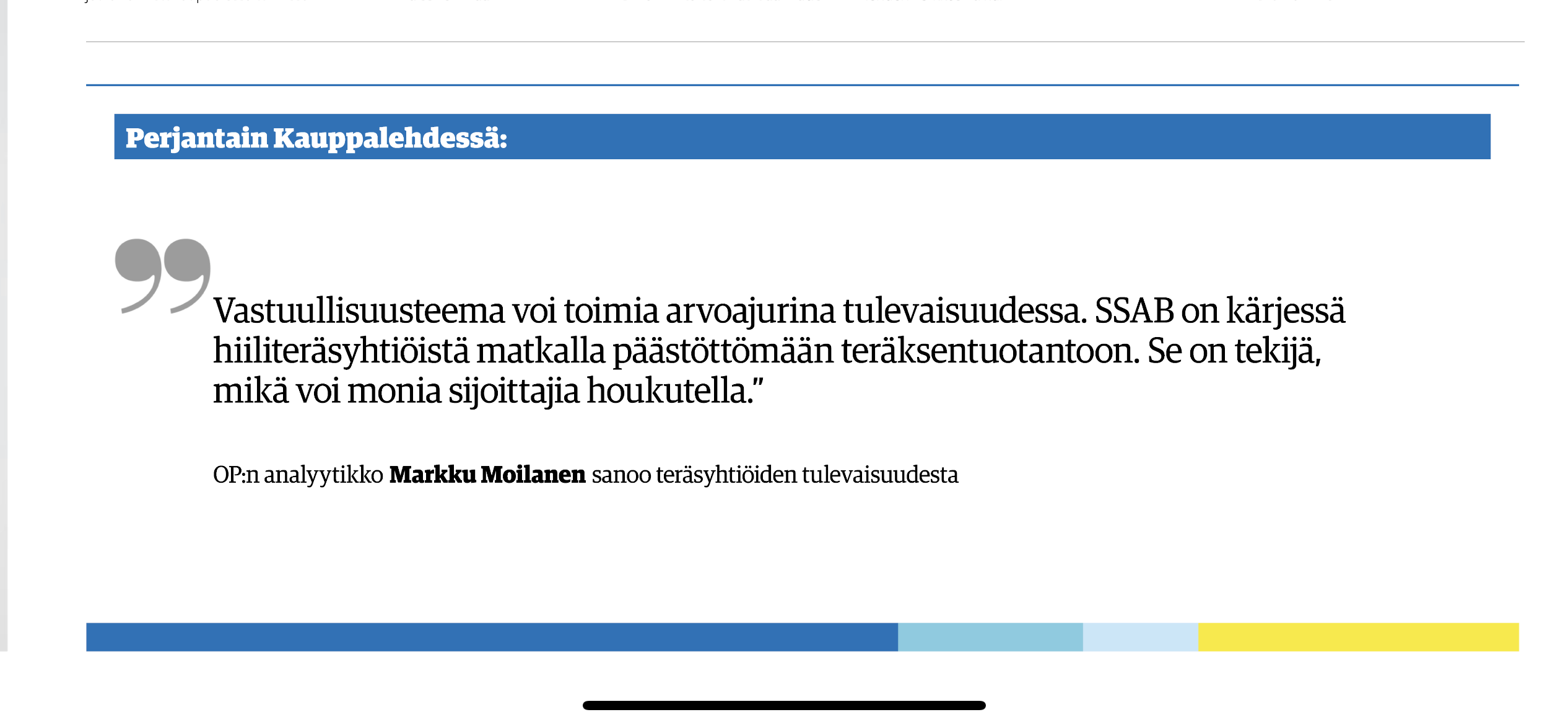

SSAB’s Q4 report was important. In addition to exceeding expectations, they announced they would accelerate their efforts to reduce carbon emissions by 15 years: SSAB now aims to be carbon neutral by 2030. Despite sharply raised EBITDA estimates for 2022-23, we maintain our Retain recommendation. This is due to the product mix appearing unfavorable at the beginning of 2022. The outlook for 2022 remains favorable, as steel prices are expected to remain better than forecast. However, we see an increasing risk that sheet metal prices will fall in the United States. We are increasing our 2022 EBITDA by 50 percent to 20.6 billion kronor and for 2023 we are increasing it by 40 percent. The company’s announcement to accelerate its carbon emission investments by 15 years is a strong statement that demonstrates the company’s commitment to being a market leader in fossil-free steel. We expect steel deliveries to grow by 2.0 percent (compared to 2 percent previously) in 2022 and 2023. Our model’s EBITDA per ton is 20,653 kronor in 2022 and 17,447 kronor the following year. We reiterate our Hold recommendation and raise our target price to 65 kronor (50).

The current situation in Ukraine (even if it resolves without armed conflict) should also be a driver for steel price increases in Europe and the United States, or am I completely wrong in my deduction?

=> at the same time, it would naturally reflect positively in steel companies’ stock prices

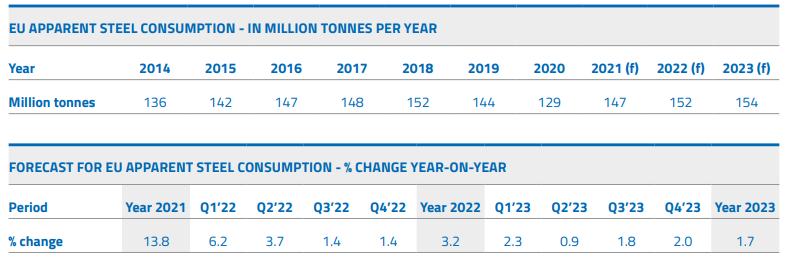

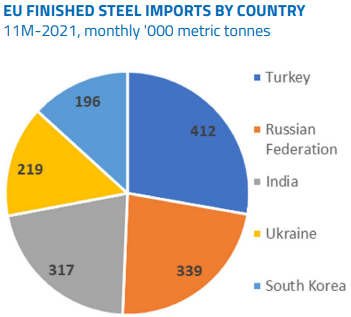

EU steel consumption (apparently net of imports and exports) in 2021 was about 147 mtons, and the growth estimate for 2022 is 3.2% on top of that = 152 mtons

Imports from Ukraine 1-11/2021 0.219 mtons/month, or 2.7 mtons runrate

Imports from Russia 1-11/2021 0.339 mtons/month, or 4.1 mtons runrate

→ i.e. 6.8/152 = 4.5% somehow perhaps disrupting the picture for the EU

Of course, both Ukraine and Russia export a lot to areas other than the EU, so potential disruptions will have wider repercussions

Possible disruptions would likely have price-supporting effects, unless the situation in Ukraine somehow affects global development / progress and thus demand outlook.