A decent dividend was expected, but a dividend yield of over 10% at this share price, while at the same time a massive investment is announced. Management clearly has strong confidence in the future.

That low-emission steel seems to be a good competitive advantage in the coming years, and apparently, demand has been strong, considering the quick timeline for converting the factories.

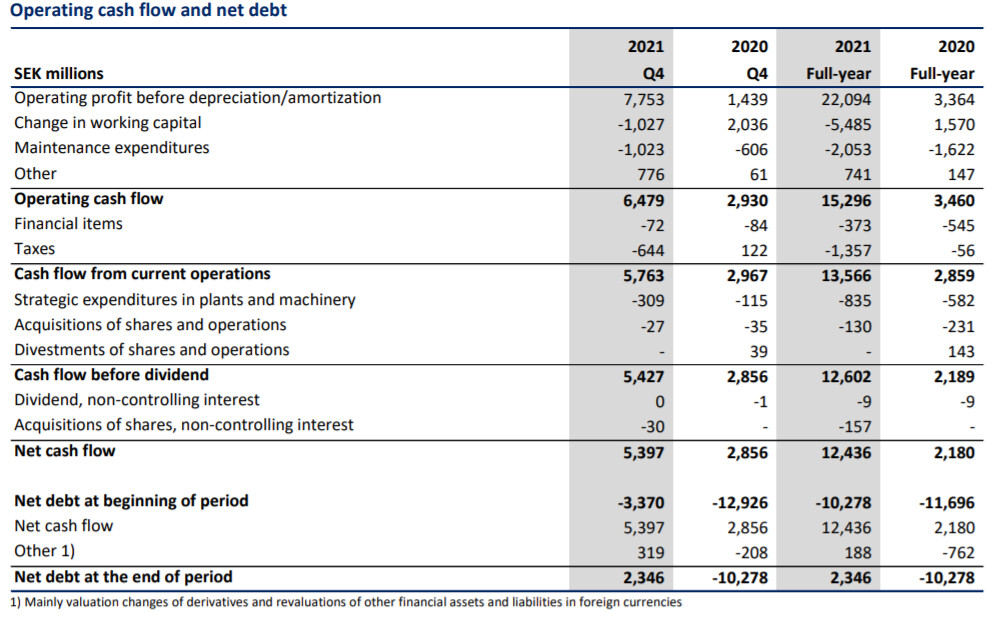

“Net cash is SEK 2.3 billion and the group is now debt-free.”

I can’t find a single weak point in the earnings report. The bears will, of course, complain that the steel cycle will turn soon, but as long as China isn’t allowed to spoil the price level, I think the results can remain strong. A ten-bagger stock.

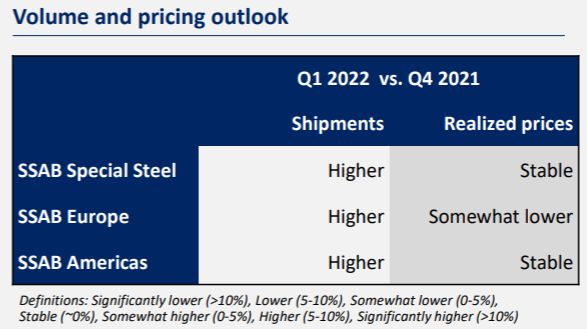

Are they planning to produce/deliver even more in Q1 than in Q4?

An absolutely brilliant year.

I had calculated based on 4 SEK in dividends, but this was a pleasant surprise, especially since I topped up during last week’s dip!

SSAB has been at the forefront of preparing for the future, which I believe is only positive in a world increasingly emphasizing CO2 neutrality.

Good point. Outokumpu is constantly tightening the screws with efficiency improvements, and apart from the Kemi mine, investments have been small. SSAB has a clear roadmap for moving towards the 2030s.

That’s a massive result, and the P/E ratio is under four. This stock was available for less than 2e a year or two ago. But when the steel cycle turns, these companies have previously been heavily loss-making, and SSAB hasn’t even paid a dividend since 2015 except twice (0.1e and 0.14). One shouldn’t look too much at a cheap P/E ratio, though.

It has been worthwhile to buy these steel stocks at the bottom of the cycle and lighten up at the peak. Nobody knows when that steel cycle peak is… not even Inderes :). Target prices vary and are such pure “guesses” that everyone should think for themselves what they believe in…

Net debt-free status probably helps, so at least there won’t be an issue in the near future. Is the situation different now, and is green steel coming? Everyone can ponder that on their own. By the way, American steel (US Steel) released its earnings last night, and the P/E ratio seems to be under 2, but the company is heavily indebted.

Great result. The quality of SSAB’s products is excellent, their product range, at least in special steels, is truly comprehensive, and now with green steel coming, the whole company is in a good position. I’ve been invested since 2015, and not much positive has happened for the stock price during that time, but now the company’s direction seems clear.

Excellent! Is the upcoming dividend paid only for SSAB AB ser A and B shares on the Swedish stock exchange? What about SSAB shares on the Finnish stock exchange?

From both series, the same 5.25 SEK. If you don’t have a SEK account in Nordnet (I don’t know about other brokers), the dividend will come to your account in euros at 0.5e per share (according to the current exchange rate). And it doesn’t matter if you buy from Sweden or Finland.

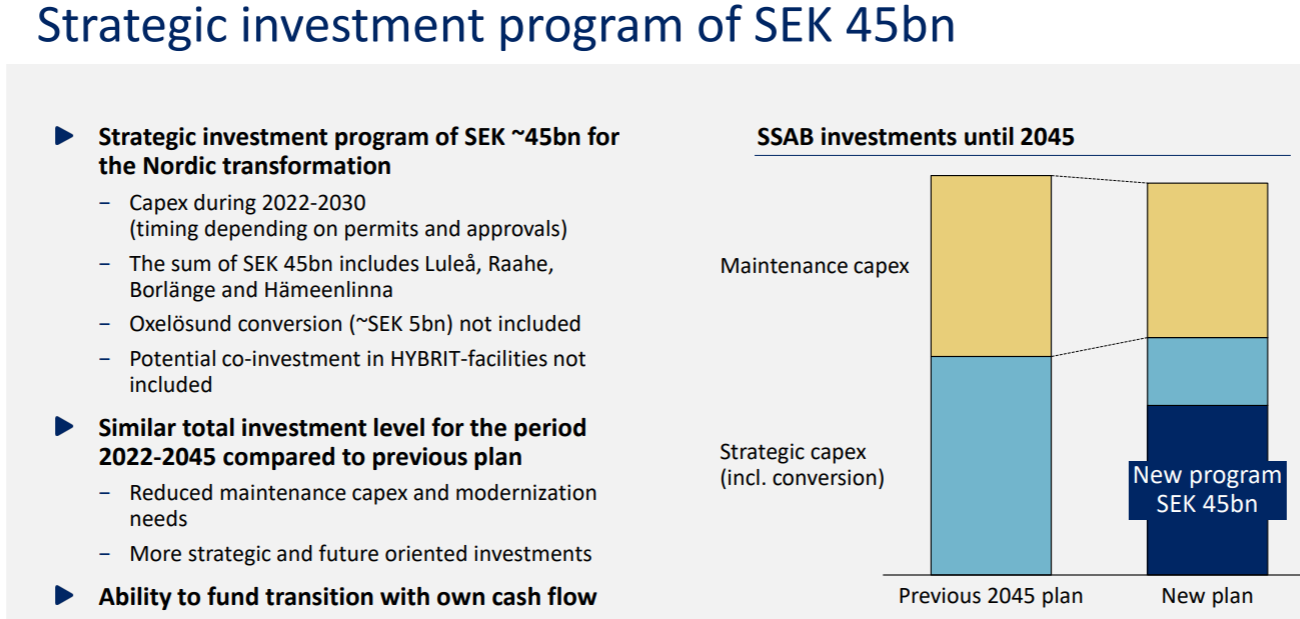

2022-2030 strategic investment program SEK 5 billion (Oxelösund) and SEK 45 billion (Luleå, Raahe, Borlänge, Hämeenlinna) = SEK 50 billion

This sum is apparently no more than the old plan, but the money will be raised over about 10 years (by 2030) vs 25 years (by 2045)

It is also stated that at the current CO2 price (EUR 90/t), emission allowances will result in a cost avoidance of SEK 7 billion/year starting in 2030, when the EU’s old free emission allowances are history.

If you look there, you can clearly see that SEK 50 billion by 2030 is not a particular problem with the 2021 cash flow (SEK 13.6 billion from current operations, and SEK 19 billion when including the increased Working Capital due to higher prices), but with 2020 figures, cash flow is not sufficient.

edit: With 2021 cash flow, the entire SEK 50 billion investment program would be in place in 3-4 years, even if dividends were paid as proposed. But…

Ref dividend 2021: SEK 5.25 x 1030 million units = SEK 5.4 billion

Unfortunately, SSAB does not disclose CAPEX needs as a large lump sum, nor does it properly highlight future investment needs such as blast furnace upgrades, which would also be encountered at least in Sweden by 2030.

SSAB also does not disclose the market pricing of fossil-free steel, i.e., the premium, which is the price difference to the conventional product. EDIT based on the telco, it sounds like there will be a premium initially, and then at some point fossil-free will be the standard.

The slides list (p21) the benefits of the update, such as product portfolio development, lower fixed costs, etc.

These issues certainly pose a big calculation challenge for analysts and financial markets!

This applies to all steel producers, which in my opinion makes the probability that it can still be passed on to others quite high.

I would consider it somewhat arrogant if they were to claim now that they know how pricing will develop, for example, 5-10 years from now, for a completely new product. I find it unlikely that it would be somehow inherently less profitable than black steel. The market will settle in such a way that the global trend is green, and if consumers are willing to pay a premium, or if the legislator forces everyone to use green steel, then either it will get a better price than black steel, or black steel will not be allowed at all, in which case green will be the new normal.

I do not see either of these mentioned as significant challenges.

So it’s down by one percent. Of course, the indexes are also in the red, but this again falls into the category of “I don’t understand anything at all.” Is this accelerating investment program so frightening, or is it that they didn’t dare to give guidance beyond Q1?

All-time record result, and good prospects for Q1 2022. Which should be around a repeat of the Q4 2021 record quarter (SEK 5.30 = EUR 0.50).

P/E at today’s closing price of EUR 4.48 is about 3.3, with earnings of SEK 14.24 = EUR 1.35.

Share price -2.65%.

It seems that, besides general market sentiment, the large figure of SEK 45/50 billion impacted the share price.

What SSAB revealed with that large figure was the Capex need for fossil-free production, and that it would be brought forward from 2045 to 2030. Apparently, the SEK 45/50 billion price tag had not been published before, and it came as a surprise.

Nor were the benefits of fossil-free production, or the concurrent improvements in the product portfolio, or the price tag of EU politicians’ CO2 policy (which was estimated at SEK 7 billion per annum in Cost Avoidance starting 2030, as now free quota emissions would have to be paid according to today’s price of EUR 90/t) mentioned. As @Cotr already estimated, since it concerns the EU’s large volume, it should not be a problem to pass on the costs. This aspect was probably not noted today.

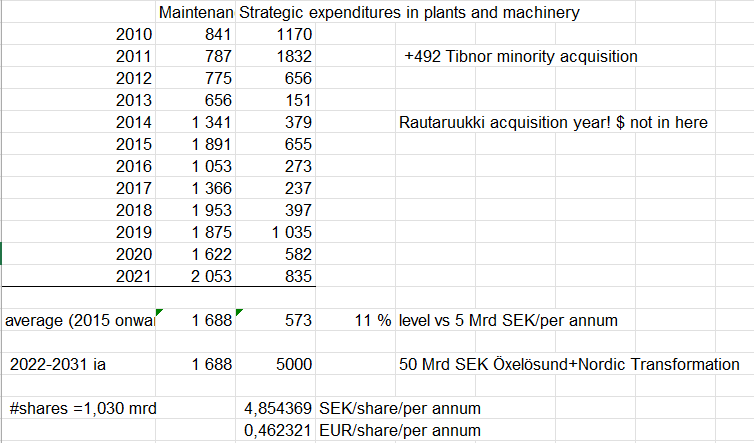

Anyway, I collected data from financial statements on how much money has historically gone into Strategic investments. An average of about SEK 573 million per year after the Rautaruukki acquisition, and now that figure will increase almost 10x for the next 10 years. With that money, of course, you get new equipment that can produce in-demand fossil-free products. According to the telco, by 2030, Luleå’s and Raahe’s 3 blast furnaces would have undergone major overhauls anyway. However, these were probably not in the analysts’ DFC calculations, and their price tag is also unknown.

Anyway, the next 10 years should generate SEK 4.85 / EUR 0.46 cash flow per share to implement this investment program, 90% of which is extra compared to the traditional investment pace. Selling emission allowances may provide some benefit depending on the rate of allowance removal that EU politicians decide on, as well as the initial price premium, product portfolio, etc.

This fossil-free steel case is quite expensive, even though all producers are more or less in the same boat. Although that extra/year is not even the Q4 2021 or Q1 2022 result. But these are excellent quarters.

Assuming that the 45 billion SEK by 2030 is what partly scared investors, I would trust the company’s management, who have the best information about the company’s situation and contracts. CEO Martin Lindqvist has been with SSAB since 1998 and as CEO since 2011, having experienced the difficulties of the 2010s from a front-row seat – one would think he wouldn’t be the first to let the company falter again. In addition, the company announced that it will finance this green transition with its own cash flow, which demonstrates the excellent level of the company’s current balance sheet and results, and strong confidence in future cash flow as well.

Another fear reflected in people’s comments is that SSAB is moving too far ahead with this green transition and, as a pioneer, will pay a heavy price for it. There are also comments that this is unnecessary greenwashing and hippification that will never pay for itself. I disagree with this. The force with which ESG issues have already hit the energy sector in just a few years is proof that this must be taken seriously. And if one thinks that ESG requirements only come from organizations, that is not true. ESG issues are currently at the top, if not second, on the agenda of capital markets. Funds, various indices, institutional investors, etc., are increasingly demanding either carbon neutrality by a certain year or at least a clear roadmap for sharply reducing emissions. This pressure does not only concern the steel industry but also the steel industry’s customers, who will have to meet similar criteria in the future. Therefore, as an owner, I am pleased that SSAB is moving ahead, but with a sustainable approach, towards climate leadership in its field.

-Doesn’t the smokestack industry always have to invest and continuously modernize factories, a new system here and there every few years? On average, one 500 million euro investment in a company the size of SSAB is “business as usual” per year to keep up with development and replace wearing parts (even large ones, for example, a blast furnace lasts about 15 years and has to be rebuilt). So, the average level of investment over the coming decade is why a relatively large dividend was dared to be paid.

“Historically, money has gone into strategic investments. Approximately 573 MSEK/year on average after the acquisition of Rautaruukki,”

That’s completely incorrect, in a 10 billion capital-intensive company, 50 million for equipment modernization per year?