Näitä samoja tarinoita on nyt kuultu ennen jokaista osaria mutta ei ole vaan tavaraa saatu montusta ylös. Miksi nyt olisi toisin? Onko joku käynyt paikanpäällä kirjaamassa millainen liikenne montusta ylös virtaa?

11 tykkäystä

Olen samaa mieltä. Liian usein on nähty, kuinka ennen osaria toiveikkaat viestit lisääntyvät ja kurssi nousee hetkellisesti terävästi ylöspäin, mutta lähes jokaisen osarin jälkeen suunta kääntyy jyrkkään laskuun. Näin on käynyt jo parin vuoden ajan. Olen itsekin ollut tässä aiemmin mukana, mutta en uskalla ottaa uutta aloituspositiota ennen seuraavaa osaria. Sen pitäisi olla oikeasti hyvä, ennen kuin harkitsen tätä enää uudelleen salkkuuni.

1 tykkäys

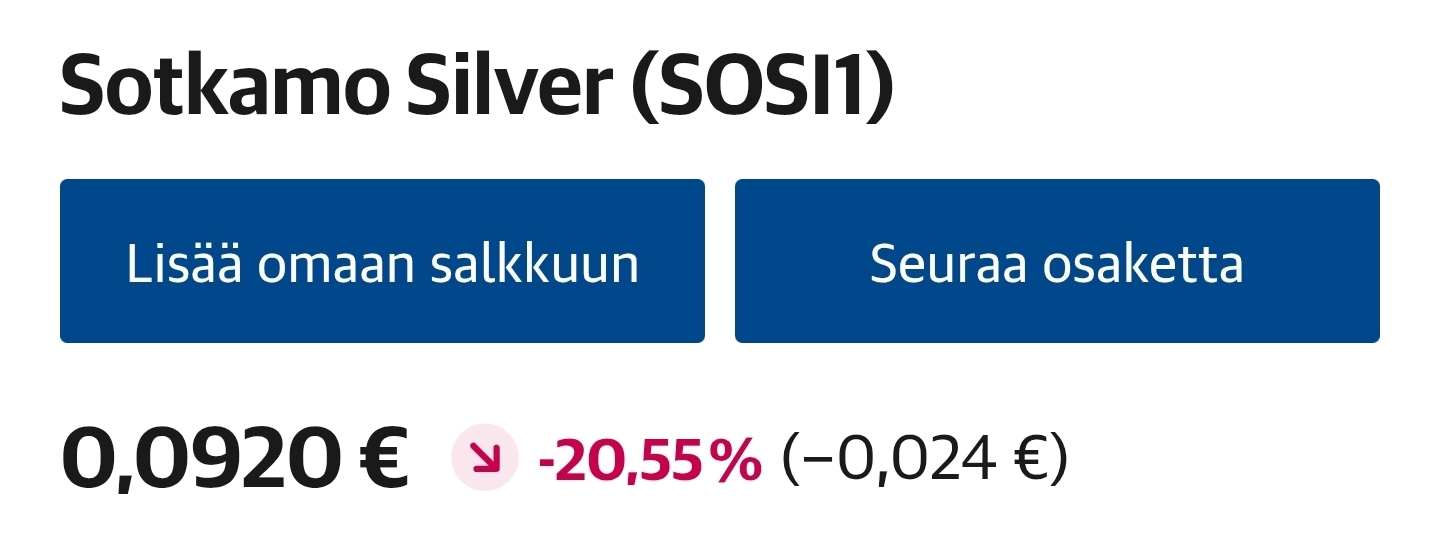

Eipä tuo taaskaan häävisti mennyt vai luuletko, että ylitöillä ja ämpäreillä selvitään tämän yhtiön kanssa?

2 tykkäystä

Tuotanto tavoitteesta tiedettiin että tullaan jäämään mutta käyttökate -% umpisurkea.

OK, kyllähän ne vähän käsikädessä kulkee, käyttökate vielä “vivulla”.

Kyllähän tuo aika iso varoitus oli. Käytännön 2 kuukauden tuotanto hävisi ohjeistuksesta. Väkisin herää kysymys, että onko tämä kuitenkin se normaali tuotantotaso, selittelyistä huolimatta? ![]()

2 tykkäystä

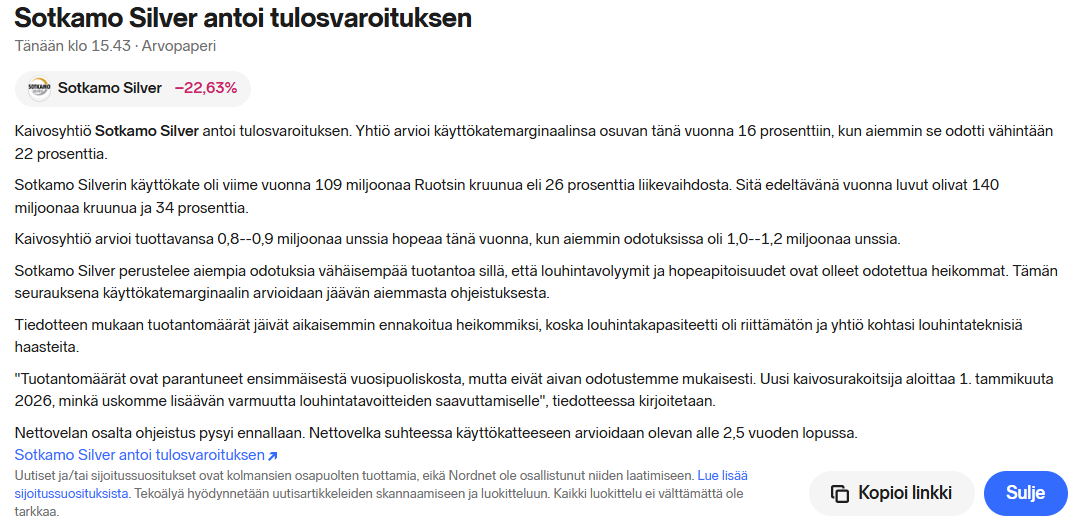

Tässä on Aapelilta yhtiöraportti tulosvaroituksen jäljiltä.

Sotkamo Silver laski perjantaina kuluvan vuoden tuotanto- ja kannattavuusohjeistuksiaan. Tuotanto-ohjeistuksen lasku ei tullut itsessään yllätyksenä, mutta oli kokoluokaltaan ennakoimaamme suurempi. Haasteiden pitkittymisen myötä laskimme lähivuosien ennusteitamme, sillä merkit tuotannon olennaisesta parantumisesta ovat toistaiseksi vähäisiä. Tuotantohaasteiden lisäksi riskitasoa kohottaa arviomme mukaan yhtiön heikko rahoitustilanne. Kokonaisuutta peilaten toistamme osakkeen vähennä-suosituksen, mutta negatiivisten ennustemuutosten ja tuottovaatimuksen noston myötä laskemme tavoitehintamme 1,00 SEK:iin (aik. 1,35 SEK).

2 tykkäystä

Edelleen ihmettelen miksi toimitusjohtajaa ei ole vaihdettu, ilmeisesti omistusrakenne on niin hajalla ettei siitä ole löytynyt yksimielisyyttä vai onko pörssitason kaivos-x-perteistä pulaa?

Kysyntä ylittää tarjonnan, joten ainakaan laskupaineita ei ole. Varmaan se todennäköisin skenaario on, että heilutaan nykytasolla ja vuoden päästä ollaan hiukan korkeammalla. Katse varmaan jo Q4:n ohi Q1:ssä uudella kaivospoppoolla, mitä saavat aikaan.

4 tykkäystä

En osta tuota johdon selittelyä kvartaalista toiseen että tuotanto jää urakoitsijan puutteellisten resurssien takia. Miksi resurssi tarvetta ei sitten tilata muualta? Onko urakoitsijalla sopimuksessa joku yksinoikeus louhintaurakointiin? Mikäli näin on niin pitäisi olla myös vastuu riittävistä resursseista. Kyllä se on johdon tehtävä varmistaa että kaivoksella on riittävät resurssit operointiin.

2 tykkäystä

Eiköhän johdollakin ala palli vapista, mikäli Tapojärvi ei heti Q1 saa tuloksia aikaan. Ilman hopean hintarallia Jalasto olisi ajanut kaivoksen jo konkurssiin…

4 tykkäystä

Kaikki vaihtoon, todella suuri epäonnistuminen kaikilta, 626k osaketta vaan hallituksella/johdolla, eiväthän ne itsekään usko yhtiöön.

7 tykkäystä

Q3 analyysissä kerrottiin, että hopean hinta on laskelmissa $37-48. Onko Aapelin näkemys, että hopea tulee vakiintumaan tuolle tasolle?

Toki Sosin kohdalla hopean hinnalla ei ole merkitystä, jos montusta ei saada tavaraa nostettua😄

2 tykkäystä

Nämä on surullisia lukuja. Ei tuolla hallituksessakaan sitten ole ketään, kenellä olisi oma nahka pelissä. Tuskin kiinnostaa muu, kun että hallituspalkkio kilahtaa tilille.

1 tykkäys

Moi,

Maanantaina julkaistussa päivityksessä tuo haarukka nousi sitten noin 37–50,5 USD/oz. Ennustehaarukka perustuu tällä hetkellä pitkälti Bloombergin konsensusennusteisiin ja yleensäkin tämä jossain määrin ennusteiden taustalla on. Viime aikoina etenkin noissa omissa lyhyen pään ennusteissa tuli käytettyä kuitenkin jonkin verran preemiota suhteessa Bloombergin konsensusennusteisiin, jotka laahasivat selvästi spot-hinnan kehitystä perässä. Sen sijaan tuo konsensuksen pidemmän aikavälin taso on ollut nyt jonkin aikaa melko vakaalla tasolla (35–37 USD/oz) ja tähän tullut nojauduttua pitkän pään ennusteiden osalta. Mutta vastauksena alkuperäiseen kysymykseesi, tuo haarukka on/oli viimeisin paras arvio.

Noh, tätä kirjoittaessa hopean spot-hinta huitelee jo lähempänä 52 USD/oz, eli juuri nyt näyttää, että olisi kannattanut jatkaa preemiolinjalla lyhyellä aikavälillä ![]() Toki SoSin kannalta merkitystä on sitten vasta kuukauden keskimääräisellä hinnalla. Mutta yleisellä tasolla, niin kyllä volatiilin hyödykkeen, kuten hopean osalta, arviota pitää pystyä muuttamaan etenkin lyhyen pään osalta melko nopeasti. Luonnollisesti metallien hintaennusteita tarkistetaankin säännöllisesti jokaisen päivityksen yhteydessä, ja kyllä metallien hintakehitystä ja -ennusteita tarkkaillaan myös jatkuvasti (vaikka muutokset aina tämä ei johda päivityksiin saman tien).

Toki SoSin kannalta merkitystä on sitten vasta kuukauden keskimääräisellä hinnalla. Mutta yleisellä tasolla, niin kyllä volatiilin hyödykkeen, kuten hopean osalta, arviota pitää pystyä muuttamaan etenkin lyhyen pään osalta melko nopeasti. Luonnollisesti metallien hintaennusteita tarkistetaankin säännöllisesti jokaisen päivityksen yhteydessä, ja kyllä metallien hintakehitystä ja -ennusteita tarkkaillaan myös jatkuvasti (vaikka muutokset aina tämä ei johda päivityksiin saman tien).

Viestiisi liittyen tuli mieleen vielä pari yleisen tason ajatusta metallien hintoihin liittyen, vaikka nämä varmaan SoSi- ja kaivossijoittajille ovatkin tuttua juttua. Eli vaikka esimerkiksi juuri tällä hetkellä onkin vaikea nähdä merkittäviä ajureita alaspäin hopean (tai kullan) osalta, on kuitenkin historiaan peilaten hyvä pitää mielessä, että hinnat voivat laskea (pidemmäksikin aikaa). Miltä tasoilta ja koska tämä sitten ikinä mahdollisesti tapahtuisikaan ja mille tasolle laskeneet hinnat asettuisivat (nämähän voivat toki olla sitten nykyisiä tasojakin korkeammalla) ovat sitten avoimia kysymyksiä. Hopean hinnan pidemmän aikavälin taso on kuitenkin pitkässä juoksussa (esimerkiksi olettamalla Hopeakaivoksen elinkaaren jatkuminen vuoteen 2035) niin merkittävässä roolissa, mikäli tuotanto piristyy ja rahoitustilanne kestää investointisuunnitelmat. Siten tietyn ajanhetken hintatason ekstrapolointi pitkälle tulevaisuuteen voi johtaa väärille raiteille volatiilissa hyödykkeessä sekä positiivisesti että negatiivisesti. Metallien hintatasot (ja niiden aiheuttamat markkinaliikkeet) tarjoavat toki sijoittajalle merkittäviä mahdollisuuksia ottaa erilaisia näkemyksiä. Mutta kuten totesitkin, niin SoSin kohdalla tällä hetkellä kriittisempää on kuitenkin tuotantotasojen onnistunut nostaminen kireä rahoitustilannekin huomioiden.

2 tykkäystä

saisko joku näihin veijjareihin yhteyden? eikö heidän pitäny ilmottaa niitä kairaus tuloksia mutta tais neki unohtua😅

1 tykkäys

Oma käsitys kairaustuloksiin liittyen on, että näiden pitäisi tulla ihan loppuvuodesta. Raportointihan ei välttämättä ole täysin yhtiön omissa käsissä, joten siinä mielessä julkistuksen venymistä tammikuulle ei voi pitää täysin poissuljettua.

1 tykkäys

Tämä kuvaa hyvin yhtiön tilannetta:

- tuotanto ei ole omissa käsissä

- raportointi ei ole omissa käsissä

- johdolla ei ole osakkeita omissa käsissä

- hallituksella ei osakkeita omissa käsissä

Sotkamo Silver on pelkkä kuori mistä voi vain hyötyä olemalla palkkalistoilla.

4 tykkäystä

Vahvat Talvivaara vibat kun lukee viimeisimpiä postauksia, yhtiö ei ole varma pitoisuuksista ja suurta vaihtelua sekä kaivostoiminta sakkaa kiitos eri haasteiden kuten kallioperän ja vesien suhteen.

Eli hopeaa voi tulle 110g per tonni tai sitten ei joka taitaa olla nykytilanne kun hopean hinta noussut paljon ja silti yhtiö antaa tulosvaroituksen.

4 tykkäystä