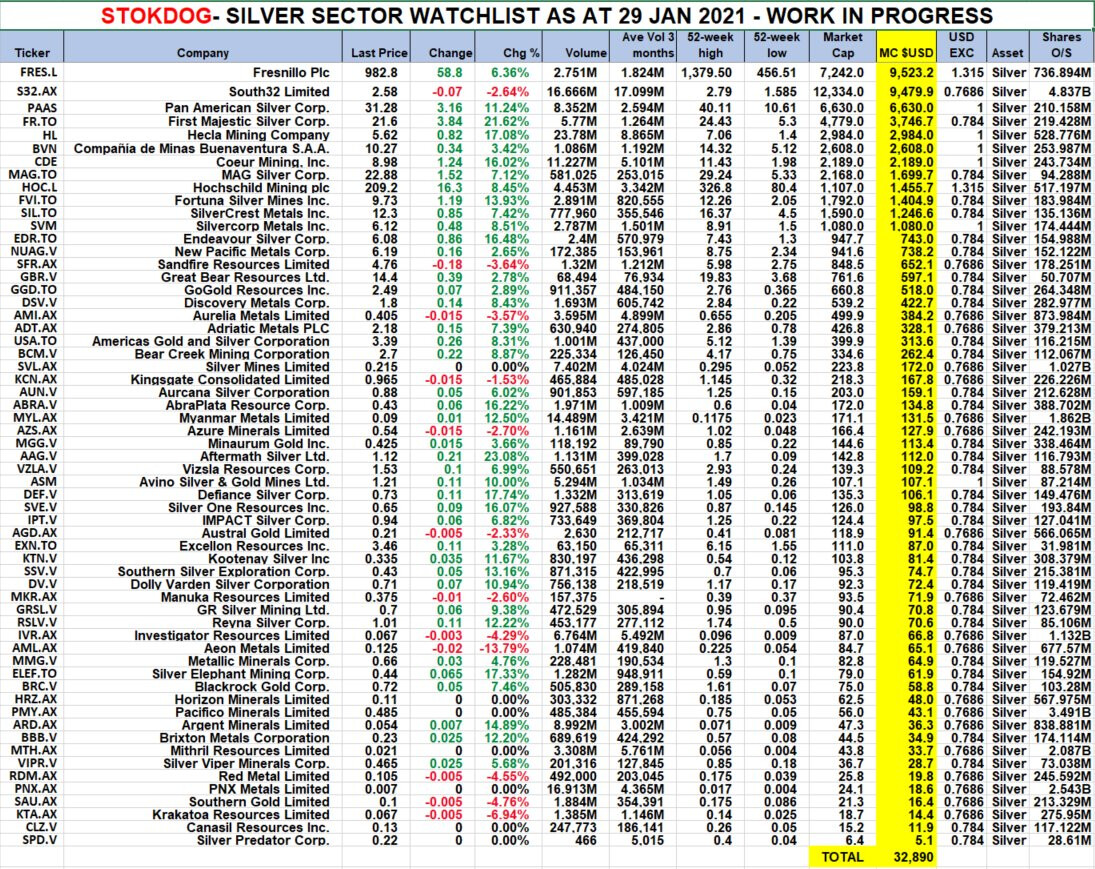

Hopea noussut parrasvaloihin WSB:n shortqueeze-episodien kautta ja nyt etenkin twitterissä tägi #silversqueeze on noussut voimalla esille. Itse tutustunut hopeaan ja hopean tuottajiin tarkemmin viimeisen vuoden ajan ja tässä omaa näkemystä tuon markkinan potentiaalista.

Hopea on siis arvometalli, jonka pääkäyttötarkoitus on sijoituskysynnän lisäksi nykyään elektroniikassa, mutta myös lääketieteessä, valokuvauksessa, aurinkopaneeleissa ja koruissa. Hopealle nähdään etenkin käyttöä huomisen vihreissä teknologioissa mm. sähköautoissa ja kenties kasvavassa määrin myös akuissa. Lisätään mixiin vielä negatiiviset reaalikorot, jotka kilpailevat holvissa istuvien arvometallien kanssa markkinaosuudesta, tässä kilpailussa arvometallit voivat pärjätä “tuotottomalle riskille”.

Pidemmän ajan funda:

-

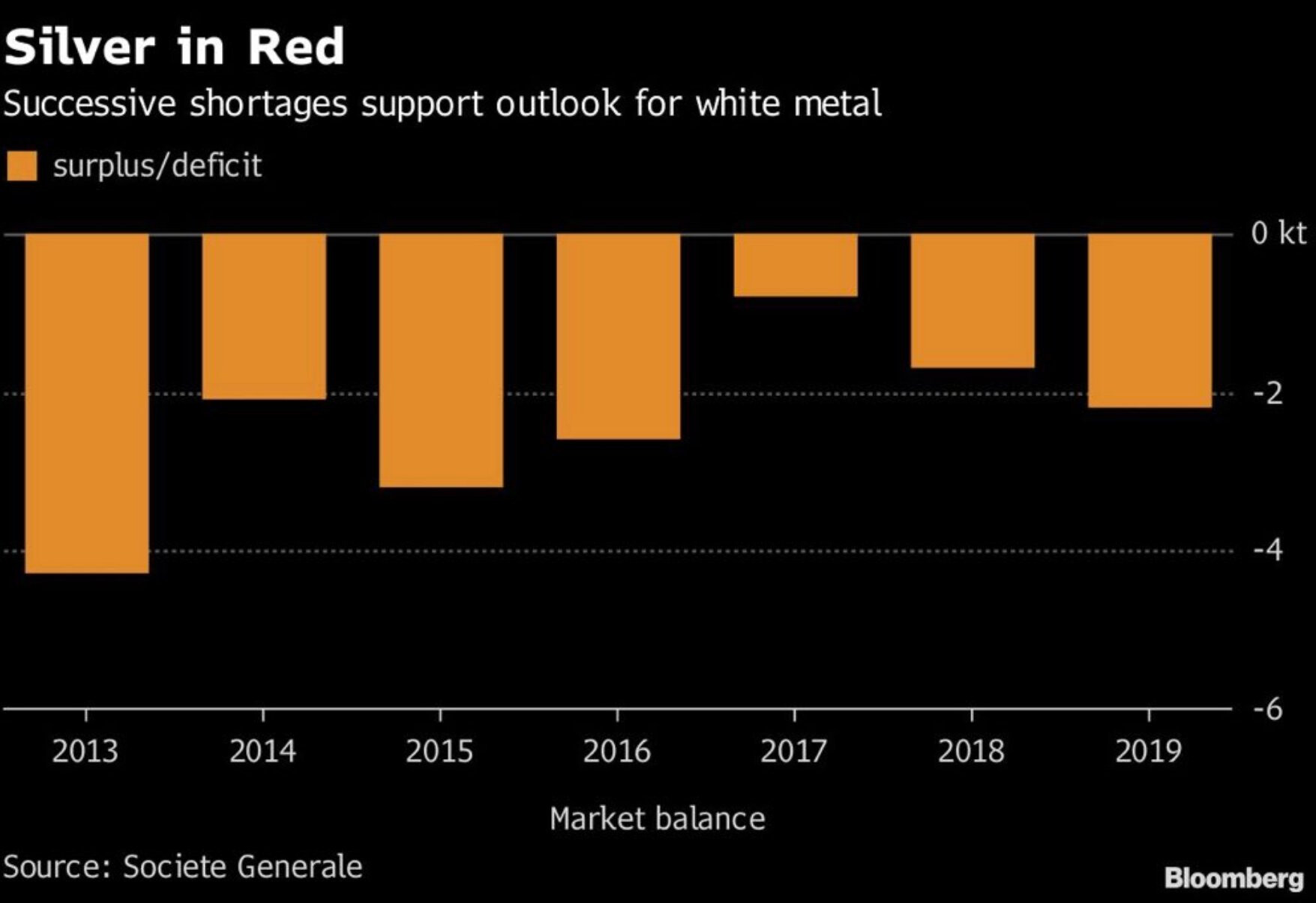

Vuonna 2020 fyysisen hopean tarjonta oli pienin, mitä se on ollut vuosikymmeneen.

-

Hopean tuotanto on viime vuodet ollut jatkuvasti alijäämäinen, maailman lisääntyvästä kysynnästä huolimatta.

-

Hopea on kaivostoiminnassa pääosin sivutuote. Alalle ei ole ollut myöskään kovia insentiivejä tulla, kun viimeisen vuosikymmenen ajan hopean tuottaminen oli alhaisista hinnoista johtuen usein taloudellisesti kannattamatonta. Tuotannon lisääminen tulee olemaan erittäin hidas prosessi ja vaatii useita vuosia.

-

Fundan puolesta sijoitusteesi solidi, kysynnän voi helposti odottaa kasvavan, kun taas tarjonta on epäelastinen ja vaatii oman aikansa vastatakseen tuohon.

Miksi hopea? Koska hopea liikkuu, kuten muut raaka-aineet erittäin syklisesti, mutta etenkin kullan kanssa sekulaarisen muutoksen aikana. Siinä missä osakkeet, kiinteistöjen hinnat, ym. liikkuvat talouden kasvun ja business-syklin aikana, niin arvometallit ovat performoineet historiallisesti loistavasti fiat-valuutan arvonalenemisen, poliittisten riskien, sodan ja vallankumousten aikana. Arvometallien korrelaatio muihin omaisuusluokkiin on myös melko vähäinen, minkä vuoksi mantra “jokaisen tulisi omistaa arvometalleja” on monelle sijoittajalle tuttu. Tarkemmin lisää linkin takaa.

Mutta miksi kirjoitan tätä viestiä juuri nyt. Arvometallimarkkinoiden ympärillä on ollut vuosikausia spekulaatiota, että päätöksentekijät ja isot pankit yrittäisivät pidätellä niiden hintaa kurissa johdannaismarkkinoiden kautta. Tälle argumentille on myös tullut valoa viime vuosina ja toimijat, kuten JPM ja Deutsche ovat saaneet näpäytyksiä ranteelle.

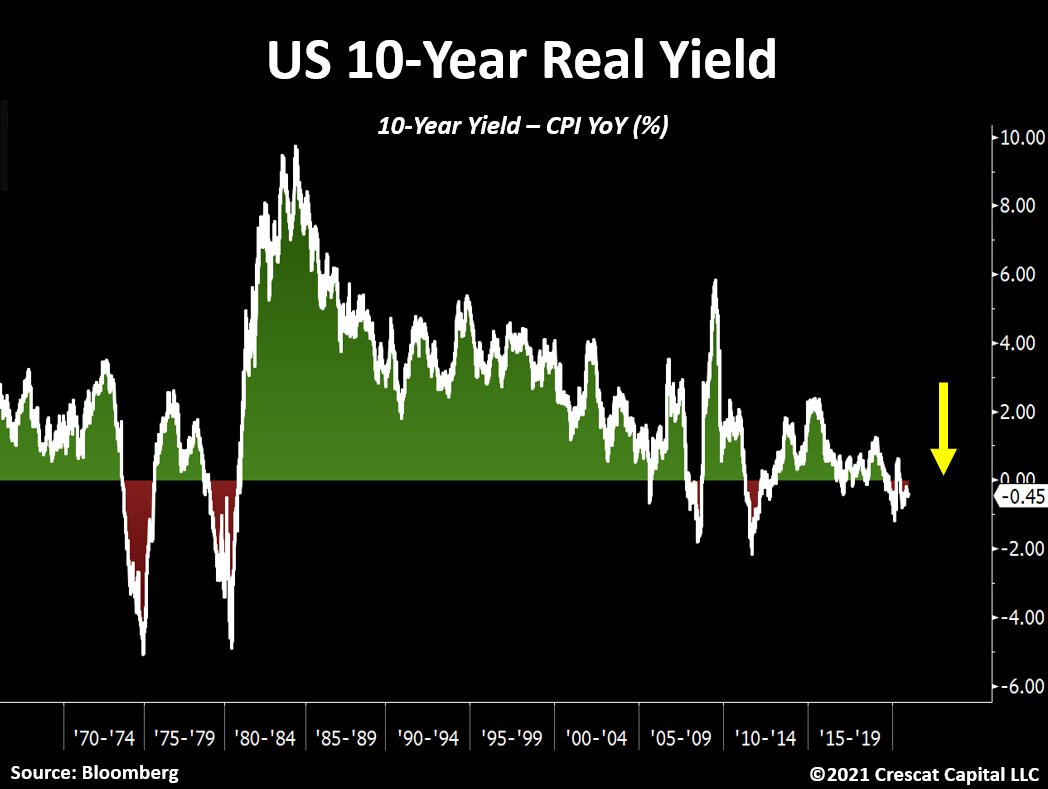

Vajaan vuoden ajan arvometallimarkkinaa tarkemmalla fokuksella seuranneena itse vakuutuin tuon hinnan tukahduttamisen mahdollisuudesta ja hyppäsin mukaan sillä uskomuksella, että tämä voisi olla tulossa tiensä päähän. Koronan jälkeen fyysisiin arvometalleihin on kohdistunut tuomionpäivän kysyntää ja ihmiset ovat vaatineet johdannaissopimusten sijaan fyysistä tuotetta toimitettavaksi COMEX:ista sen sijaan, että toimitusta oltaisiin rullattu eteenpäin, kuten on ollut tapana. Esim. 2020 hopean toimituskuukausina huhti-, kesä- ja elokuu toimitettiin enemmän hopeaa COMEX:ista asiakkaille, kuin vuosina 2016-2019 yhteensä. Muuan Paul Volcker kommentoi myös 1970 luvun inflaatioon liittyen, että kullan hinnan päästäminen nousuun oli luultavasti virhe. Arvometallit korreloivat hyvin vahvasti reaalikorkojen ja rahan määrän kanssa. Foliohatun kireyttä säädellen jokainen voi sitten tutkia, miksi tälläisessä ympäristössä arvometallit eivät ole vielä lähteneet sen enempää liikkeelle, kysynnän ollessa valtaisa.

Tällä hetkellä hopea on hinnoiteltu edelleen johdannaisten kautta, jota on fyysistä hopeaa kohden liikkeellä ainakin moni-satakertaisesti. Olen ollut toivossa, että jossain vaiheessa tuo hinnoittelumekanismi muuttuisi metallien hinnoittelusta paperilla kohti fyysisen tuotteen kysyntä-tarjonta hinnoittelua. Tällä hetkellä, olen tuosta yhä vakuuttuneempi.

Tämä #silversqueeze-liike on ajanut ihmisiä ostamaan fyysistä hopeaa isolla volyymilla erittäin lyhyessä ajassa. Ympäri maailmaa arvometallien jälleenmyyjät ovat kohdanneet todella merkittävän kysyntäpiikin ja useita raportteja nähty jo tuotteen täysin loppumisesta. Samalla muut hopeaan sidotut instrumentit, kuten hopea-ETF SLV kohtasi perjantaina historiansa suurimmat ostot, mitkä vastaavat 1150 tonnin hopeaostoja yhdessä päivässä. Tämä mekaniikka asettaa tietysti painetta hankkimaan tuotetta, mistä on muutenkin vajausta.

Se, mistä ei ole tähän liittyen ollut puhetta ja minkä koen kaikista merkittävämmäksi on kuitenkin paine, minkä tämä suuntaus asettaa teollisuusalan toimijoille. Tulevaisuudessa oletettavasti kovaa kysyntää omaavien tuotteiden (sähköautot, aurinkopaneelit, elektroniikka) valmistajille on ensisijaisen tärkeää turvata välttämättömän materiaalin saatavuus. Tämä asettaa painetta isoja teollisuuden toimijoita kohtaan tehdä ratkaisuja tuon turvaamiseksi, hinnan ollen toissijainen. Jokunen kuukausi sitten nähtiin esimerkkiä mahdollisesta tulevasta kehityskulusta, kun Tesla liittyi yhteistyöhön litium-yrityksen kanssa.

Vielä riittäisi sanottavaa mm. isoista hopean shorttipositioista, jotka ovat määrältään 180 päivän edestä hopeaa koko maailman tuotannosta, tällä hetkellä olevista isoista preemioista fyysiselle tuotteelle, mitkä ovat myös positiivisia ajureita hinnalle, mutta katkaistaan tähän. Vahva uskomus kuitenkin, että tämä liike voi koitua paljon merkittävämmäksi, miltä se alunperin vaikuttaa.