Excerpt from OP’s Morning Review

1 Like

(UPM, Helsinki, 2 February 2021 at 10:30 EET)

UPM Timber is planning measures to enhance its operations, improve profitability, and strengthen competitiveness. The planned measures focus on reforming the sawmill management model and streamlining the supply chain. Additionally, there are plans to discontinue the small log line at Kaukas sawmill during 2021. According to the plan, Kaukas would focus on one sawmill line going forward. Plans also include optimising the operating rate of Korkeakoski sawmill.

UPM Timber will initiate co-determination negotiations related to these plans. The co-determination negotiations involve UPM Timber’s personnel in Finland, excluding sales personnel and production employees at Seikku and Alholma sawmills. The estimated total reduction need is a maximum of 60 positions.

2 Likes

UPM will soon no longer meet ethical investment criteria. Collective bargaining is a fundamental right of employees.

5 Likes

This was one of the reasons I returned to this top company back in the day. Jyrki Hollmen and humanity don’t fit in the same sentence. The Hakaniemi ayatollahs can fuss all they want, but nothing major will happen.

The labor movement seems scared.

I see the reform as an opportunity for both parties. I don’t see it as an opportunity for the employer to unilaterally dictate terms. In that case, the best workers will leave.

Local bargaining provides the best flexibility ![]()

2 Likes

Local agreements are always talked about by companies. In reality, local agreements don’t happen. Local factory management has no authority to negotiate anything. This means decisions are made centrally at headquarters. This practice is directly a problem for UPM and MG companies. Currently, people are voting with their feet against the current operating model and moving to competitors in large numbers. I’ve been following this struggle at different tables for 20 years, and it’s constantly moving towards a stiffer direction. That’s not necessarily the smartest way to handle things. In one rather critically important unit, nearly 20% of employees have resigned in the last couple of years. And more are leaving. There’s probably no problem here either, but the work these people did required several years of work history to gain enough experience to take responsibility for the tasks.

7 Likes

Related topic: Metsä Group rakentaa uuden sellutehtaan, Kemissä iloitaan jätti-investoinnista – Katri Heiskanen: "Työpaikkoja tarvitaan" | Yle

7 Likes

Good Q1 guidance from the Board

Metsä Board’s Q4 numbers were largely in line with expectations. The Q1 guidance was good, likely driven by a stronger pulp market and seasonally good demand for paperboards. The dividend increased, but with a lower coefficient than our forecasts.

In addition, Metsä Fibre’s Kemi pulp mill investment was confirmed. Metsä Board will also start a slightly complex investment program in Kemi (including bottleneck investments in the liner machine and the purchase of an unbleached pulp production line from Metsä Fibre).

The share price appears to have risen slightly into positive territory after initial hesitation.

8 Likes

Personally, I don’t like the arrogant operating methods of some domestic forest companies, whether we’re talking about personnel policy, environmental issues, or fair trade. For this reason, these companies will be missing from my portfolio, with the exception of Metsä Board, which also remains primarily because I inherited the fundamentals from my father.

As a forest owner, I have so far made all my timber sales with sawmills, even if the price received for the timber has not always been the best. If, on the other hand, I want to invest in the forest sector in some way, in addition to Kemira, which is in my portfolio, Ponsse will be the target.

EDIT: Proofreading

13 Likes

OP - Metsä Board Q4 earnings 11.2.2021

Yesterday, a very interesting acquisition was announced, especially from the perspective of Metsä Board and also Stora Enso, as Mayr-Melnhof is buying IP’s Kwidzyn mill in Poland. At Kwidzyn, IP produces folding boxboard, fine paper, kraft paper, and market pulp with a total of 4 machines and a capacity of 760,000 tons (likely mostly integrated with a 400,000-ton pulp mill). The mill was slated to exit IP at the end of the year to a spun-off (fine) paper company, where it would have been outside the core business. IP already sold its US consumer board business to Graphic Packaging a few years ago.

Mayr-Melnhof is paying EUR 670 million for the mill, which corresponds to an EV/S multiple of approximately 1.5x and an EV/EBITDA multiple of 7x. Last year, the mill achieved an operating margin of 18%. My understanding is that profitability has also been good or very good in the long run, and I don’t believe that Kwidzyn loses out significantly to Metsä Board’s and Stora Enso’s best board mills. There is a clear discount in acquisition prices compared to the stock market valuations of European board companies (cf. Metsä Board’s EV/EBITDA of 10x). In the USA, Graphic Packaging’s and WestRock’s multiples are roughly at these levels. No wonder Mayr-Melnhof saw the deal as good, and the stock is now up 3%.

What makes the arrangement particularly interesting is that the same Mayr-Melnhof recently acquired KotkaMills and its large folding boxboard machine. The Austrian company, with its renewed management (MM’s CEO is the former CEO of Mondi), has thus burst into competing in folding boxboards (MM has been a significant player in recycled fiber-based consumer boards in Europe). The folding boxboard market, important for Metsä Board and Stora Enso, has therefore consolidated, which is in principle a good thing for price discipline. On the other hand, in Mayr-Melnhof’s hands, KotkaMills and the Kwidzyn mill pose a couple of orders of magnitude more severe competitive threats to Finnish companies than an independent KotkaMills owned by private equity investors and Kwidzyn, which was on the periphery of IP’s strategy. It will be interesting to see how the market dynamics of folding boxboards develop and whether Mayr-Melnhof will continue aggressive market share seeking or if it will focus on generating cash flow to pay for the acquisitions.

16 Likes

(UPM, Helsinki, 17 February 2021 at 3:00 p.m. EET) – UPM has joined the EU Clean Hydrogen Alliance and is participating in the industrial clean hydrogen roundtable working group. UPM is also a member of the recently established hydrogen cluster in Finland. UPM is excellently positioned as the hydrogen economy develops and wants to proactively participate in its development and emissions reduction. The hydrogen economy is gaining significant importance as the European Union strives for climate neutrality by 2050.

“Clean hydrogen offers several interesting opportunities for UPM. We have our own renewable and CO2-free electricity, water resources, biogenic carbon dioxide, and practical experience in hydrogen production at UPM’s Lappeenranta biorefinery. Our expertise and resources enable the development of potential new business opportunities in the nascent hydrogen economy,” says Jyrki Ovaska, UPM’s Chief Technology Officer. Ovaska represents UPM in the EU Clean Hydrogen Alliance.

UPM has recently initiated the basic engineering for a new potential biorefinery, during which opportunities for green hydrogen production and utilization will be specifically explored. The potential biorefinery would produce 500,000 tons of high-quality renewable fuels for road transport, aviation, and as raw material for the petrochemical industry.

Clean hydrogen is seen by many industries as an important route to low emissions. Clean hydrogen is currently receiving a lot of attention, but large-scale scaling is still in its early stages.

“Several legislative preconditions related to the development of the hydrogen economy are still open. Through the alliances and cooperation networks now being established, UPM wants to be involved in creating an operating environment that promotes both investments and emissions reductions,” Jyrki Ovaska states.

17 Likes

Well, now we have another Finnish company joining Bezos’s project. That will at least increase international visibility. Currently involved are, for example, Amazon, Microsoft, and Neste.

4 Likes

It’s not really about pulp, but it is about Stora Enso.

What do you think about this, and is there more information about it: https://www.storaenso.com/fi-fi/newsroom/news/2021/2/selfly-store-by-stora-enso-for-automated-and-unmanned-retail

And here are the cabinets in use: Pieniä kassattomia ruokakauppoja putkahtelee kaikessa hiljaisuudessa ympäri pääkaupunkiseutua | HS.fi

https://circa-group.com/the-company

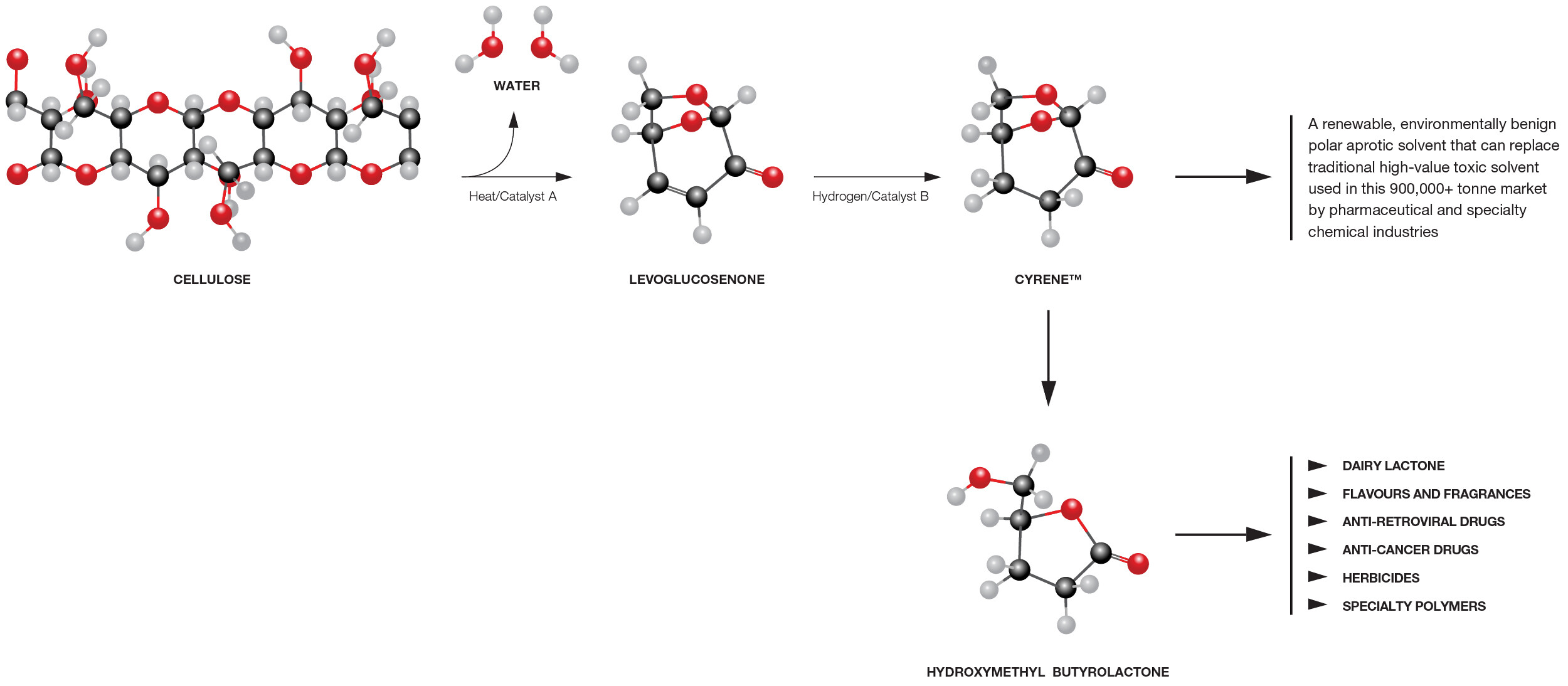

Tomorrow, this company, which belongs to the cellulose chain, will start on the Norwegian stock exchange.

The idea is to produce renewable solvents from agricultural and forestry side biomasses for use in the chemical and pharmaceutical industries.

I don’t know if this is a good investment, but what if I bought a couple of thousands worth of shares first thing tomorrow morning, and if it rises in the coming days, I’d sell them?

1 Like

Something like this in a couple of weeks ![]()

2 Likes

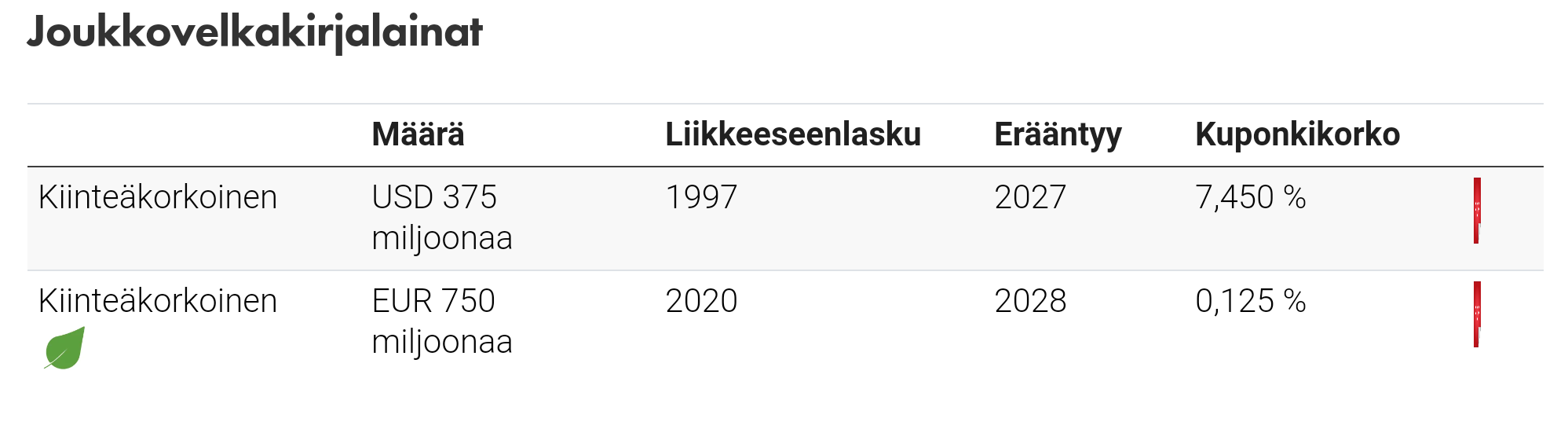

UPM has again secured cheap loans from the market. Not quite as cheap as the one sought in November (750M, fixed 0.125% interest, maturity 2028). Press release from yesterday:

https://www.inderes.fi/fi/tiedotteet/upm-laskee-liikkeeseen-toisen-vihrean-joukkovelkakirjalainansa

“UPM has successfully issued a new EUR 500 million green bond under its EMTN (Euro Medium Term Note) bond program and green finance framework. The bond matures in March 2031 and pays a fixed interest rate of 0.50%.”

The bond will be used to finance projects and investments enabled by UPM’s green finance framework, published in November 2020. The proceeds from the bond are initially planned to be used for the following framework categories: sustainable forest management, climate-positive products and solutions, prevention and management of environmental burden including waste prevention.

“The issuance of our second green bond was successful, and it was once again gratifying to see investors’ interest in it. This new green bond contributes to achieving the sustainability goals of our Biofore strategy,” says Tapio Korpeinen, CFO of UPM.

UPM now has to pay quite a different interest rate than before:

Source:

5 Likes