Communication technology company Savox Communications is planning to list on the main list of the Helsinki Stock Exchange.

Savox’s CEO Jerry Kettunen told Kauppalehti that the company’s goal is to go public in the near future.

“We are a critical communications systems company. Our customers include defense sector operators, security sector operators, and certain industrial customers,” Kettunen describes.

IPO pages:

The planned initial public offering and share sale are expected to consist of a share issue by the company of approximately EUR 30 million (gross proceeds) and a share sale by Savox’s largest shareholder, Savox S.A., which is a company controlled by the Chairman of the Board, Paul Ehrnrooth.

Danske Invest Finnish Equity Fund, DNB Asset Management, Elo Mutual Pension Insurance Company, Protean Funds Scandinavia, and Tesi (Finnish Industry Investment Ltd) have each separately committed to subscribe for shares in the company for a total of approximately EUR 26 million in the planned IPO and share sale under certain conditions and provided that the valuation of the company’s entire share capital before the proceeds from the share issue is no more than EUR 160 million.

The goal of the IPO and share sale is to support the implementation of Savox’s long-term business strategy and strategic objectives. The proceeds from the listing would strengthen the company’s balance sheet and financial flexibility, enabling the execution of its growth strategy. A stronger balance sheet would particularly support working capital management, the financing of customer and program projects, and long-term research and development investments, allowing for even greater financial maneuverability and flexibility in financing solutions. The listing would also allow Savox access to capital markets and the expansion of its ownership base among both domestic and international investors, which would increase share liquidity. In addition, the IPO and share sale are expected to benefit Savox operationally, improve Savox’s brand awareness among its customers, potential future employees, and investors, as well as other stakeholders, thereby strengthening the company’s competitiveness and supporting long-term value creation. The listing and increased liquidity would also enable the more efficient use of shares as consideration in potential acquisitions and in personnel incentive schemes.

In my opinion, Savox is the Fiskars of critical communication devices.

Based on my own experiences, Savox products are of very high quality. Seamless communication in critical and hectic environments is practically essential for achieving a good outcome. The demand for this type of equipment is certainly not going to decrease in the future.

Savox could hardly have planned a better time for an IPO, as the defense sector is under such intense hype, which will surely provide some kind of extra boost. However, the defense industry is a very challenging field, but if you manage to gain a foothold and prove yourself trustworthy, the end result can be very favorable.

Just a quick heads-up: Savox will be holding a presentation event tomorrow starting at 6:00 PM at Miltton’s premises. Before the main event, there will be an opportunity to get to know the company’s products while networking. If you can’t make it in person, you can follow the company presentation itself via webcast.

The subscription period begins tomorrow. The share price is 10.72 euros, and the emphasis is on the institutional side.

“In the Public Offering, a preliminary maximum of 233,208 Offering Shares are being offered to private individuals and entities in Finland. In the Institutional Offering, a preliminary maximum of 4,429,430 Offering Shares are being offered to institutional investors through private placements in Finland and, in accordance with applicable laws, internationally outside the United States. Depending on demand, the Company and the Main Owner may, without restriction, transfer Offering Shares between the Public Offering and the Institutional Offering, deviating from the preliminary number of shares.”

What are your thoughts on the company? I’m personally interested, so I’ll have to read the prospectus once it’s approved and available

Based on the intensity of the discussion, the investing public seems surprisingly indifferent toward Savox, even though its profile would typically be expected to generate significant excitement. Alternatively, there might be hidden interest, and the (very) small public offering could be quickly oversubscribed.

The valuation doesn’t provoke strong dislike; rather, it prompts positive nodding if one believes in the sustainability of the numbers. The company has roughly as much net debt as the proceeds expected from the offering, so the EV (Enterprise Value) would land around the 200 million mark. Guidance for the current year is 65-75 million in revenue and a 14-18% adjusted EBIT margin. Assuming the midpoint for both, the valuation would be around 17-18x EBIT for this year. There is an order book in place, so in 그 respect, it seems very realistic. If growth continues even somewhat similarly, the price isn’t bad at all. The company’s targets for 2030 are outright bold, with average annual revenue growth exceeding 20% and an EBIT margin also over 20% in that year. If we take the ended year 2025 as the starting point for calculations, revenue was 56.1 million; thus, at the lower end of the target, 2030 revenue would be 140 million, and at the lower end of the EBIT margin target, EBIT would be 28 million. With that level of performance, the company would offer truly delicious returns, but there is certainly a lot to prove. It remains to be seen how the situation develops.

Based on a quick Google search, the industry appears to be highly competitive with a large number of manufacturers. Based on that, the projected growth figures and margins seem questionable.

Sijoittaja.fi has also written about Savox; nothing particularly groundbreaking, and the rest of the article is behind a paywall.

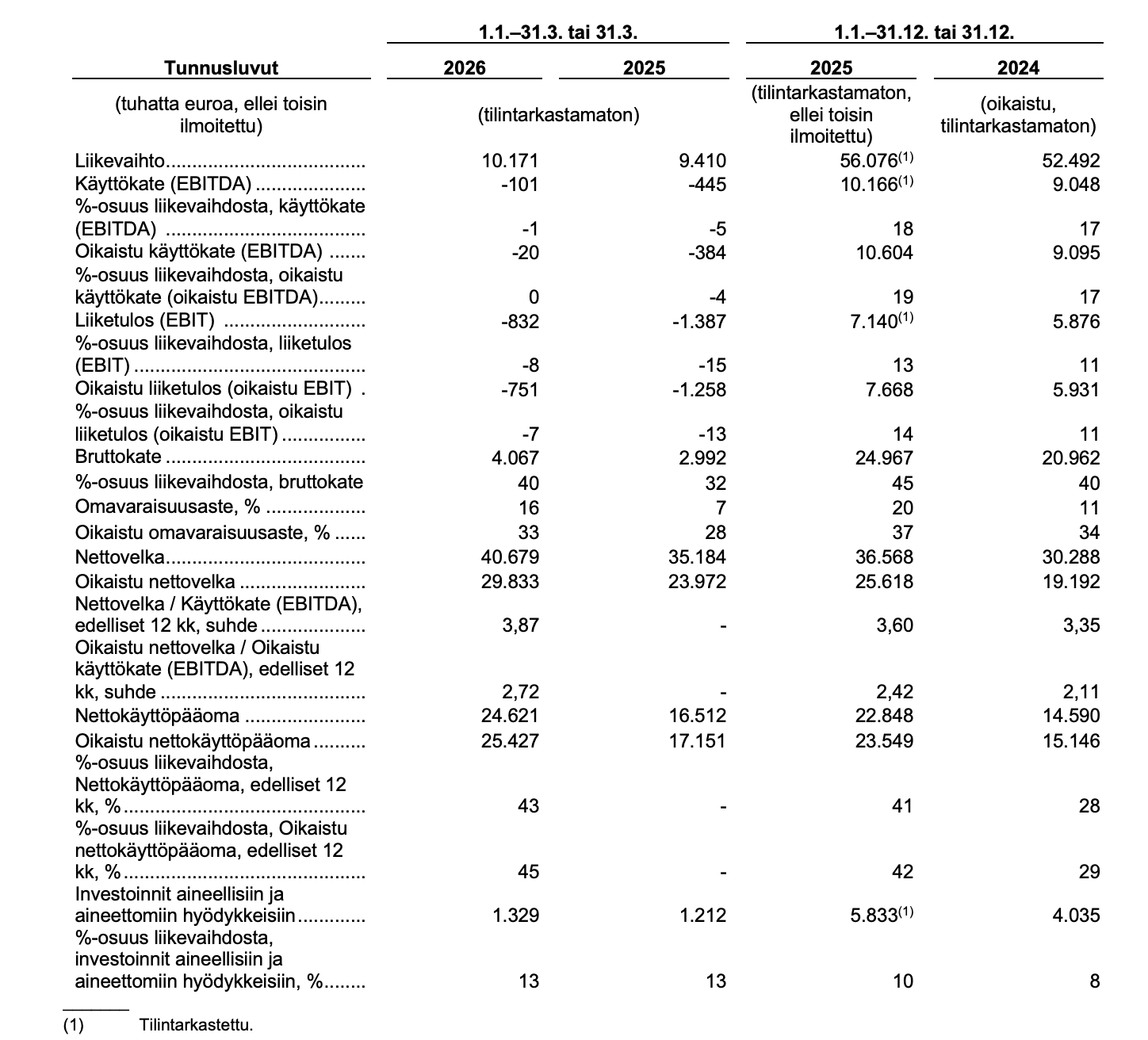

Savox’s net debt at the end of March was 40.7 million euros, of which 10.8 million euros were capital loans. Net debt adjusted for capital loans was 29.8 million euros, and its ratio to the rolling 12-month comparable EBITDA was 2.7x. The adjusted equity ratio was 33 percent. Thus, there is a fair amount of debt, but the share issue strengthens the balance sheet. Reducing indebtedness and financing working capital are at the core of the justification for the issue. A significant amount of working capital is tied up, as adjusted net working capital was 25.4 million euros, which is typical for a growing project-oriented equipment manufacturer.

Hate to disappoint you, but unfortunately Gemini didn’t quite nail this one. For example, Bittium’s valuation is in a completely different ballpark than what Gemini claims. For this year, P/S is ~8x, EV/EBITDA ~25x, and EV/EBIT ~40x. Based on historical figures, they are even significantly higher.

In general, just throwing out these AI responses isn’t very productive. Especially if one hasn’t bothered to verify its claims and assumptions.

But all in all: Savox’s pricing based on this year’s figures is not at the level of the top names in the defense industry, but clearly lower. And that’s how it should be, given the lack of track record, the products, and the scale. In any case, Savox also has a strong demand environment behind it, so there should be potential for strong growth.

Thanks, Master Mardi! Your feedback is quite valid; AI is indeed often a rather unreliable source of information.

There is very little expert analysis available on this, although there are some paid ones.

The industry certainly has momentum, and if it lists at a reasonable price and subsequently delivers a positive surprise, there could be an upside ahead.

Esa does great work, thanks Cadel - this fits in well here! * although these must be verified by everyone; Savox IPO financial targets, valuation, and dividends

Savox IPO share price: €10.72/share Savox market capitalization after listing: 190 million euros

Revenue 2025: 56 million euros Operating profit (EBIT) 2025: 7.6 million euros P/E ratio 2025: approx. 28

The company’s Board of Directors has set the following financial targets for the period ending at the end of 2030:

Revenue growth: Average annual revenue growth of at least 20 percent.

Profitability: Increasing the operating profit margin (% of revenue, operating profit (EBIT)) to over 20 percent over time.

Dividend policy: The target is a dividend payout ratio of 30–50 percent of comparable earnings over time.

I am slightly surprised that the public offering was not suspended today at 4:00 PM, which, according to the terms, was the earliest possible time for suspension. It was revealed in Tuesday’s presentation that everyone is guaranteed a minimum allocation in the public offering; this stems from stock exchange rules requiring 500 parties to own at least 500 euros worth of shares. The size of the public offering is therefore 2.5 million euros, and shares can also be transferred from the institutional side to the public side (at the company’s discretion).

Well, perhaps a press release will still be issued during the weekend. The institutional offering can be suspended on Monday at 4:00 PM.

Coincidence or not, but this release was timed well regarding the share issue:

let’s add that the company ‘promises’ 20% growth p.a., this deal will bring in about 1.5…3.5 MEUR per year (2027…2032)

→ so there is certainly room for 5-10 times this amount in the growth projection

INSIDE INFORMATION: Savox’s next-generation vehicle computer selected for vehicles delivered in the CAVS vehicle project

Savox Communications Plc’s (“Savox” or the “Company”) next-generation vehicle computer has been selected as part of the armored Patria 6x6 vehicles to be delivered within the framework of the multinational CAVS (Common Armoured Vehicle System) project.

The Company estimates the value of the vehicle computers’ lifecycle deliveries to be between approximately EUR 8–20 million, depending on the number of vehicle computers delivered. The Company estimates that the expected deliveries will be concentrated in the financial years 2027–2032. The Company’s estimates are based on information received during the competitive bidding process. Negotiations on the delivery terms for the vehicle computers are currently ongoing and are expected to be completed during the third quarter of 2026. This matter is not expected to have an impact on the Company’s guidance for the 2026 financial year.

The CAVS project develops and delivers modern 6x6 vehicles based on a common vehicle platform from which several different versions have been developed. The program also covers the maintenance phase of the vehicles. Savox considers its participation as a supplier in the orders placed from time to time within the CAVS project to be probable. In addition to the now-selected next-generation vehicle computer, the Company’s current offering for the CAVS project includes, among other things, situational awareness solutions and intercom systems. The timing of orders placed with the Company from time to time depends centrally on discussions related to the technical content of the vehicles, and the value of potential orders depends on the final scope of the systems purchased for the vehicles.

Jerry Kettunen, CEO of Savox, comments:

“Savox’s strategy is based on the seamless interaction between the dismounted soldier and vehicles, where integrated vehicle systems play a key role. Improving situational awareness emphasizes the importance of edge computing and system integration. The selection of Savox’s next-generation vehicle computer for the CAVS project is a significant step in the implementation of the company’s strategy and a continuation of the strong demand for the defense sector product portfolio during the current year.”

It is also very possible that this will be announced today in connection with information regarding a potential oversubscription of the institutional offering. The company and the lead shareholder have the option to reallocate the offered shares between the institutional and retail offerings. In that sense, the offerings are intertwined, and with the retail portion being a negligible share of the total offering, it might be convenient to close it at the same time as the institutional offering.

Irresponsible speculation: In any case, it is very likely that the offering is already significantly oversubscribed in terms of money, and everyone in the retail offering will be allocated something close to the minimum, which means they might still be waiting for the target number of individual subscribers to be met. If the minimum is slightly over 500 euros (50 x €10.72), the “absolute maximum” number of subscribers would be around 4,700 private individuals (/entities). So, they are likely still waiting for that to fill up, rather than waiting for monetary oversubscription. With minimum allocations, the share price would need to rise by over 10% for “stagging” (flipping for quick profits) to yield even a few dozen euros after costs. For many, it will certainly feel more natural to just hold or buy more. Many will likely top up their small positions once trading begins, which will drive a nice price rally for at least the first week. And tada—thus we have a “successful” IPO when the price rises above an already somewhat pricey subscription price. The advisors and managers can pat each other on the back for a job well done. But this is how these things work, both in the big world and the slightly smaller one. In the long run, however, the company’s business performance determines the final result, so there’s no need to place too much value on this.

So, most likely around 4:00 PM today, there will be a release stating that both Savox offerings were oversubscribed by large volumes and the party can begin. Of course, I could be wrong and this message might age poorly. Waiting with interest.

This (the supplement to the prospectus) further confirms that the deal was genuinely finalized only on Sunday. The company surely would have disclosed this in the prospectus already to “stimulate” demand if it had been confirmed before Sunday. No one is crazy enough to pay lawyers extra now just to have that phrased and included after the fact.

Due to the right of withdrawal resulting from the supplement, the subscription periods for the Public Offering and Sale as well as the Institutional Offering and Sale have been amended as follows:

• The subscription period for the Public Offering and Sale is expected to end on June 17, 2026, at 4:00 p.m.

• The subscription period for the Institutional Offering and Sale is expected to end on June 18, 2026, at 4:00 p.m.

I’ve been thinking that the negotiations behind this latest deal have likely been going on for quite some time.

It is entirely possible that it was already known on Friday that the signing would take place on Sunday. Or, at the very least, that signing was highly probable.

If the offering had been closed prematurely on Friday, there would surely be talk that “This was already known. It’s not fair play to close early on Friday and then announce on Sunday.”

Either way, in a few days we will know what the outcome is. In terms of euros, it is likely clearly oversubscribed.