Fredrik and Johan were presenting Röko at RedEye’s serial acquirers conference last week. The recording can be viewed here:

4 Likes

Here is a panel discussion from the same event, in which Röko participated:

3 Likes

Is Röko the new Berkshire? A place to compete for who gets the worst eye roll or cry of anguish from the CEO or Deputy CEO for their question? The beginning of a legend.

5 Likes

Thank you for this excellent point and for discussing the benefits of wider margins. I agree.

Considering these potentially inflationary times, wide margins and capital lightness are not a bad thing, because

i) pricing power is available, and

ii) investment needs are minimal. Note that investments also become more expensive with inflation, which easily weakens their returns.

One more thought on Röko’s company repertoire, which many investors are pondering.

The company indeed requires 10 years of good numbers to show. I have a hunch that for companies selling to other businesses (B2B), this could also be a good sign of strong customer retention. But is it enough data for the consumer side? Are the same beauty products always in fashion? What about beers? All of us who have examined beer shelves have noticed that even large brands sometimes face tighter competition on the shelves…

On the other hand, the fate of individual brands doesn’t shake the overall picture much, as there are over 30 companies and about a third are consumer businesses. And even those are diverse. For example, student caps, at least based on Finnish experience, are eternal and expensive.

9 Likes

I’ve skipped Röko’s thread several times while browsing Inderes, but curiosity finally got the better of me, and this turned out to be a rather interesting case. There’s clearly strong expertise behind it, and I’m always fascinated by the idea of decades-long compounding stories in serial acquirers.

I’ve now superficially researched the company, and one thought-provoking aspect relates to Röko’s model of keeping the incentives of acquired company owners aligned with the group. Röko typically buys a majority stake and leaves a significant minority share to the founders. Often, there’s also a condition that Röko will later buy out the remaining shares, or alternatively, the owner has the right to sell them. In the medium term, incentives are clearly aligned because the founder still has a significant financial stake in play. But what happens after Röko buys the rest? The founder will likely step aside, and a salaried management will take over. In such cases, the entrepreneurial spirit may inevitably weaken when the business is no longer “their own” in the same way. I don’t know how far these option structures extend, but in the long run, this could impact the culture and performance of the subsidiaries. This, however, seems to be a fairly common challenge for serial acquirers, and even more so for those who buy companies entirely immediately. What then is the best way to operate, or does such a way even exist?

Another thing that puzzles me a bit with many serial acquirers is the scarcity of organic growth. Röko’s Q4 presentation shows that organic growth has been moderate over the last four years: 2022: 8%, 2023: -2%, 2024: 2%, and 2025: 2%. Why doesn’t a compounder buy compounders? On the other hand, if targets were growing strongly organically, acquisition multiples would be on an entirely different level than, for example, EBITA x8. But does modest organic growth indicate that companies operate in such narrow niche markets that simply no more growth is available, or that the companies genuinely lack competitive advantages? In Röko’s case, an EBITA margin of about 20% would nevertheless suggest some pricing power. For example, with Teqnion, I often wonder if the holdings are of poorer quality and lack clear competitive advantages, and there, margins are also lower. On the other hand, it might also be that precisely such a combination (moderate growth + reasonable acquisition price) yields the best return on capital, as investments pay for themselves quickly, but it would be nice to see a bit more organic growth.

And what kind of a player is this new CEO really? I haven’t had time to watch Bladh’s interviews much yet, but Karlsson certainly hypes him up. With Bladh becoming CEO, the CFO position is taken by a 27-year-old named Douglas Kressner. He could, of course, be a very capable person, but I find it a bit odd that a nearly freshly graduated person rises to the CFO position of a publicly listed company. In many companies, the CFO plays a very strategic role. There are, of course, differences between companies in the scope and criticality of that role, but I’m somewhat puzzled by this decision.

Every now and then, I get excited about a new company, and this seems to be the latest case, even though a few things I didn’t care for about the company have already emerged. My usual way is to take a small initial position very quickly if, after light familiarization, the business seems interesting and the valuation at least reasonable. After that, deeper familiarization begins, and often these companies end up being sold within a few months, but sometimes longer-term holdings are also found. Could this be one of them?

19 Likes

Welcome to the thread! I’ll answer based on my understanding after familiarizing myself with the company. A big disclaimer: I’ve been buying shares for some time on a declining price, and my position is such that my thoughts are guaranteed to be biased towards optimism. So, it’s worth listening to answers from someone more pessimistic or digging for answers from other sources ![]() This is, however, excellent practice to respond when someone questions things a bit, so a big thank you!

This is, however, excellent practice to respond when someone questions things a bit, so a big thank you!

My understanding is that Röko only acquires companies where the entrepreneurs remaining as minority owners do not intend to retire anytime soon. It could be that an entrepreneur sells to Röko long before retirement age to diversify their assets, if it’s already clear there are no successors among heirs, for example, or simply to provide security for their family.

Another example could be a situation where an entrepreneur is about to retire, and the company’s operational activities have already been significantly managed by other members of the management team/key personnel for a good while. This group might be interested in continuing, but their risk tolerance isn’t enough to buy 100% of an SME all at once. A similar situation can occur in a family business’s generational change.

In such cases, Röko takes on the risks of the main owner, but the company’s key personnel/next generation essentially get to run the business with entrepreneurial freedom, while minority stakes keep incentives aligned. Röko pays dividends to minorities, so such a deal can be very attractive to many. Entrepreneurial freedom and “drive,” but with controlled risk and appropriate reward for good results. In the best-case scenario, Röko can be on the same journey with minority owners for a very, very long time.

If and when minorities eventually exercise their options and are about to retire, Röko primarily recruits a successor internally. If none is found, they search externally. My understanding is that the option arrangements made will last at least beyond the medium term (3-5 years?), even if the entrepreneur plans to leave as soon as possible.

This brings us to how this entire model requires really strong trust between the parties. Röko’s management must also have excellent “people skills” to handle these diverse, often very intimate situations where an entrepreneur is partly giving up their life’s work and beloved “child.” Think about how these SME entrepreneurs have often practically put all their eggs in one basket, and 100% of their wealth can be in that company built from scratch ![]() Well, this went a bit off-topic, but the intention was to emphasize that price is not always the deciding factor, and an entrepreneur can remain a minority owner for a long time. In this regard, a recent presentation had a good slide:

Well, this went a bit off-topic, but the intention was to emphasize that price is not always the deciding factor, and an entrepreneur can remain a minority owner for a long time. In this regard, a recent presentation had a good slide:

This brings us to why the serial acquirer model is so effective. In principle, the model can thrive with very modest organic growth that beats inflation, e.g., 3-5% over time is enough for good results. Of course, higher organic growth is always better if it comes with a good return on capital.

If companies are then acquired at, say, 8x EBITA, that implies a return on capital of approximately 12.5% before taxes, with businesses being capital-light (=low capex). If such a 12.5% return can be achieved over decades by reinvesting, say, 80-90% of the cash flow, the company can grow by approximately 10% through acquisitions. Add to this 3-5% organic development, and the compounding machine, at its best, grinds out about 15% annual growth. Not bad if it can be done for decades. At this rate, the company quadruples in about 10 years.

This is why niche companies with limited growth opportunities but pricing power fit the model so well. In the best-case scenario, organic growth can then be achieved through price increases ![]() And price increases are good because they don’t require capex

And price increases are good because they don’t require capex ![]() So a compounder doesn’t need compounders within it, but rather cash flow with low maintenance investments! Constellation Software, for example, is a textbook example of this with its thousands of software companies. Of course, many serial acquirers also have organic success stories within them, which has given the machine even more momentum.

So a compounder doesn’t need compounders within it, but rather cash flow with low maintenance investments! Constellation Software, for example, is a textbook example of this with its thousands of software companies. Of course, many serial acquirers also have organic success stories within them, which has given the machine even more momentum.

On the other hand, organic growth opportunities should not be stifled either, but their returns on capital and profitability must be very strictly compared to the returns achievable through acquisitions. In other words, disciplined capital allocation. Of course, you can’t buy any slowly dwindling companies in sunset industries; fundamentally, they should still exist decades from now. A good aspect of the model is also that sometimes you can let a business wither if something happens to it. It doesn’t break the machine if there are dozens of companies.

[quote=“Osinkohaukka, post:45, topic:68981”]

And what kind of a player is this new CEO? I haven’t had a chance to watch Bladh’s interviews yet, but Karlsson certainly hypes him up a lot. With Bladh becoming CEO, the CFO position is taken by a 27-year-old guy named Douglas Kressner. He could, of course, be a very capable person, but I find it a bit strange that someone almost fresh out of university takes on the CFO role of a listed company. In quite a few companies, the CFO has a very strategic role. Of course, there are differences between companies in the scope and criticality of that role, but this decision puzzles me a bit.

[/quote]I’ve understood that when Fredrik and Tomas founded Röko, they deliberately wanted to bring in very passionate and talented young people from the start. For example, Johan has been involved for 7 years, starting from the second acquisition. In my opinion, Röko has been built very patiently from the beginning, so potential successors have been identified well in advance. In a company like this, however, culture is so hugely important that it would be good for successors to come from within the company. This is how successors were nurtured, for example, at Berkshire and elsewhere. Röko is, of course, still a very young company, but it originated from a model that was probably already refined during the founders’ previous tenures ![]() In this way, culture and continuity were built from the beginning with a long-term perspective and very clear goals.

In this way, culture and continuity were built from the beginning with a long-term perspective and very clear goals.

15 Likes

Has anyone compared this company and Kinnevik? I mean, as an investment target, the situation, outlook, valuation, etc.

I wouldn’t compare it to Kinnevik, as the strategy and portfolio investments differ so much that it doesn’t really make sense to compare them. You can find better comparable companies.

Röko is more like a basic serial acquirer / PE company. Kinnevik is more like a VC.

2 Likes

Let’s save this observation here, which might partly explain the share price drop in many serial acquirers, including Rökö.

10 Likes

Annual report published. This time it’s also translated into English!

4 Likes

I read through the annual report tonight. Probably not much new for those following the thread. The report concisely covers Röko’s acquisition principles and model. What needs to be written is written. The results speak for themselves.

However, Röko’s accounting is not the clearest. Röko usually acquires companies with a 60-85% ownership stake, leaving the old owners/management to operate the companies. The company reported a net income of 755 MSEK in 2025, of which 0 SEK would go to minority owners. However, minority owners received 148 MSEK in dividends. This reporting method is due to the company having a put/call option arrangement to buy out minorities from the companies, which is why it records the entire profit as attributable to shareholders. For this reason, when estimating the share price, I believe it’s worth using EV/adjusted EBITA (currently approx. 19x) or EV/NOPAT (24x) as metrics, which account for these liabilities. Röko has full control over the companies’ cash, and it should be noted that money is not withdrawn from there haphazardly.

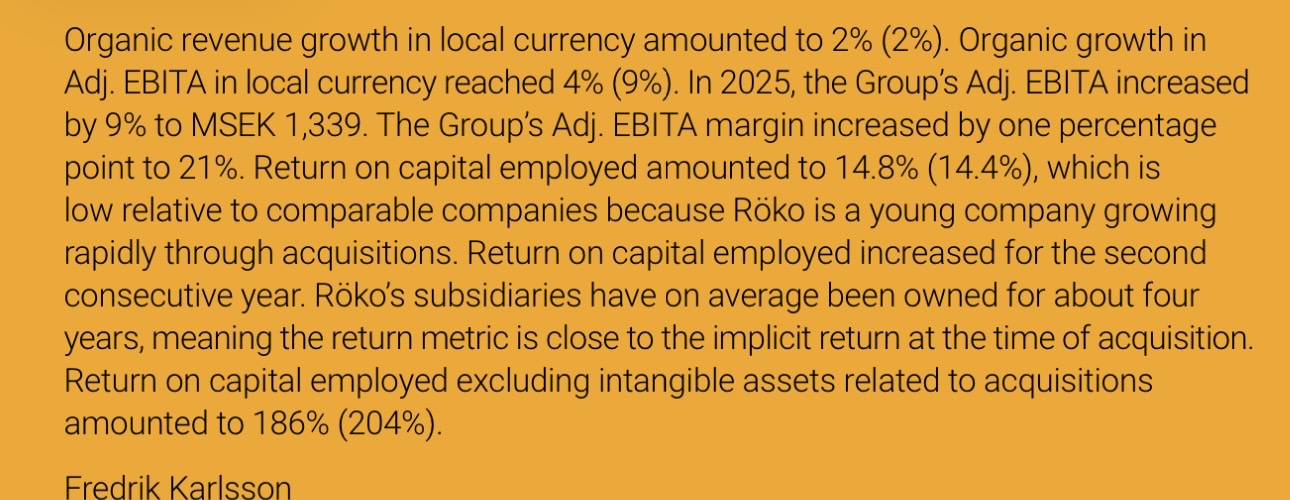

Last year’s numbers did not show exceptional development, but currency changes had a significant impact. The report shows the development of key figures throughout history, and the progress is impressive. Since 2023, no new money has had to be raised by diluting shares. Indebtedness has decreased. It should also be mentioned that no key personnel have sold shares since the listing.

Other amusing side notes:

- The chairman of the board, Tomas Billing (the other main owner), and Fredrik Karlsson share the same salary, 4925 TSEK (~500,000 EUR). While the salary for the chairman of the board is quite high (Nordean’s chairman’s remuneration is 440,000 EUR!), it is reasonable for a CEO. It’s surprising that Fredrik even draws it.

The upcoming CEO, Johan Bladh, already earns more.

I meant to write others too, but these accounting observations are not amusing. ![]()

Addition. I meant to mention in the thread that if we adjust for amortization of intangibles and other non-cash flow or less recurring items, such as listing expenses, last year’s operational “cash flow result” (a kind of NOPAT) would have been approx. 1034 MSEK, or 70 SEK per share. Hence the EV/NOPAT multiple of 24x which I wrote above.

22 Likes

It’s a bit of a side note for the investment case, but as I understand it, Röko has another Finnish connection, and of course, through student caps ![]() Röko’s subsidiary AJAT Group apparently includes C. L. Seifert Finland Oy, which in turn acquired the Fredrikson brand, familiar to many, in 2024.

Röko’s subsidiary AJAT Group apparently includes C. L. Seifert Finland Oy, which in turn acquired the Fredrikson brand, familiar to many, in 2024.

It seems there’s currently an attempt to introduce a culture to Finland where student caps would be more customized, and some extra (and expensive) frills would be ordered along with them ![]() This is apparently already quite common in Sweden and Denmark, for example

This is apparently already quite common in Sweden and Denmark, for example ![]()

Such a germ of organic growth on this front in Röko’s B2C segment ![]() The margin also improves if you can sell sparkling velvet or some pin for an additional price with the cap

The margin also improves if you can sell sparkling velvet or some pin for an additional price with the cap ![]()

7 Likes

Do you have a long-term assumption that Røko could grow significantly faster organically or improve the profitability of already acquired companies, given that the return on capital is not particularly high (14.8%) at the moment?

With a high acquisition rate, capital also grows, and it’s challenging to increase returns if acquisition prices remain similar to historical levels.

Isn’t Røko structurally a more moderate grower if the goal is to acquire companies at around (under) 8 times EBITA?

2 Likes

Personally, I would expect a couple of percentage points of growth, roughly in line with or slightly above nominal economic growth in Europe, where Röko’s companies operate. Based on the companies’ profitability and Röko’s criteria (10 years of proven growth and profitability), they seem better than average, but I would still only assume cautious organic growth.

The return on capital is still low compared to high-quality serial acquirers, as the company is in its “early stages.” Returns will improve on paper over time.

It’s essential that acquisition targets are bought at an EV/EBITA of 8x or less. That’s roughly a 10% cash flow yield after taxes, simplifying things.

10 + 2% = 12%.

When you take on debt, growth is faster. On the other hand, according to Fredrik’s comments, even the best in the industry make mistakes in about one in twenty acquisitions.

Röko, if I recall correctly, aims for about 15% growth, doubling its size every five years. It’s by no means impossible.

For example, the much larger Lifco once again doubled its size in 2020–25, mainly by acquiring twice the amount of revenue compared to Röko’s current size. The last five years include bubbles and stimulus, but also recessions and crises. ![]()

18 Likes

This is precisely what I tried to address above.

The company reiterates the same, for example, in its annual report, but how does this happen?

The “improves over time on paper” argument holds true, doesn’t it, if either of the following occurs:

-

The pace of acquisitions slows down/stabilizes relative to the portfolio size, and the acquired companies continue to perform, diluting the goodwill in the denominator.

-

The acquired companies grow organically/improve profitability significantly faster than new goodwill comes in.

With acquisition prices remaining the same, ROCE improvement is more of a promise than a mechanical consequence because the denominator grows faster than the portfolio’s organic growth/profitability improves.

A clear ROCE improvement would require either that the acquisition targets’ prices are lower than targeted and/or that the growth/profitability of the existing portfolio improves.

10 Likes

ROIC/ROCE improvement is based on organic growth. The acquisition cost is “fixed” on the balance sheet, but over time, the numerator of the equation grows due to organic growth. With a young serial acquirer, this development has not yet had a chance to occur to a significant extent.

6 Likes

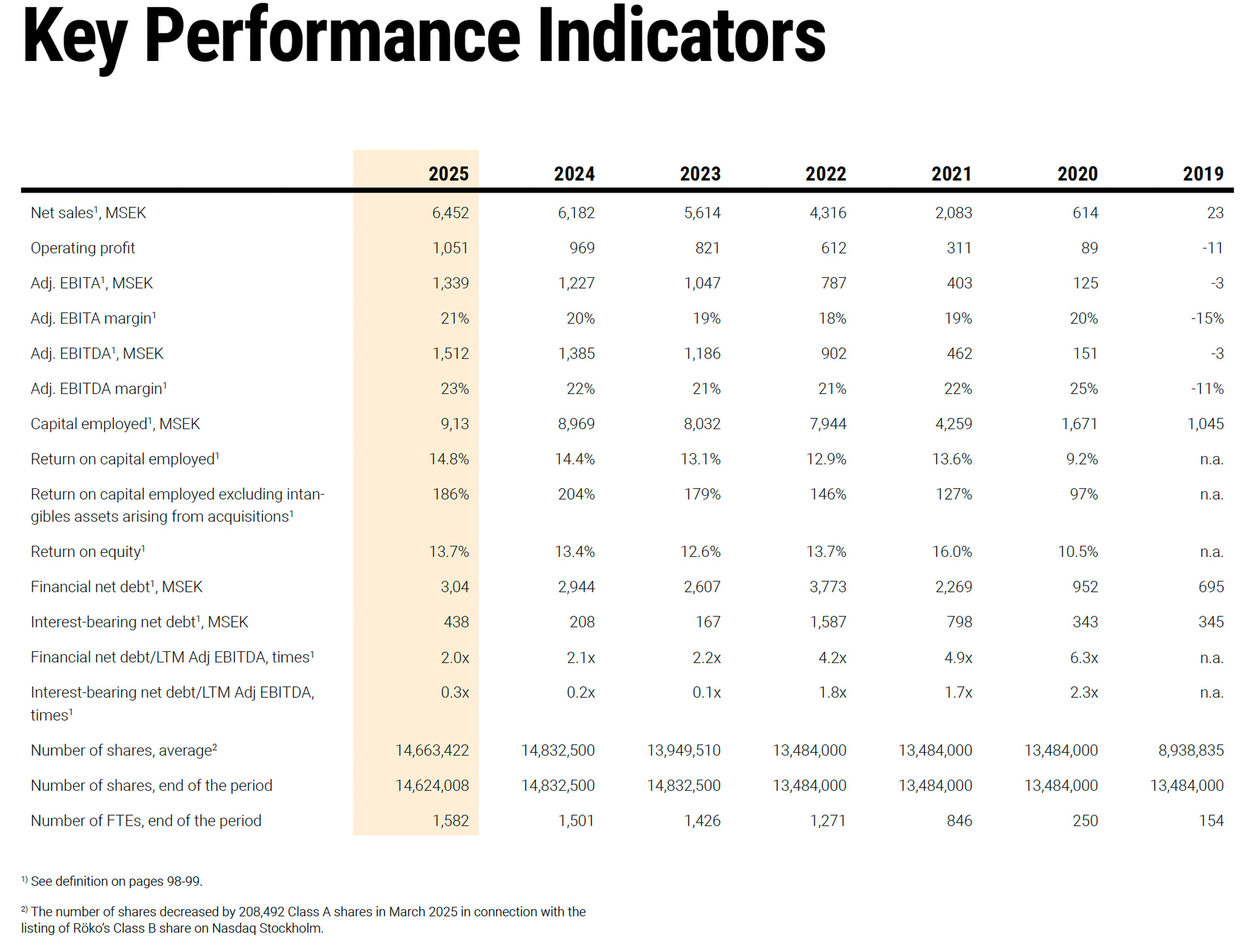

In the screenshot, Fredrik advertises that the return on capital employed (ROCE) of the companies owned is 186% without intangible assets related to acquisitions. Based on this, Röko’s management particularly believes in point 2, i.e., acquired companies grow organically, and through that, the return on capital employed increases. In addition, point 1 is certainly also true.

4 Likes

Yep, the companies are very asset-light, so organic growth is almost “free” from an investment perspective.

The most essential thing about serial acquirers is i) how well capital generates returns in acquisitions and ii) how good they are as perpetual owners. If they make poor acquisitions, the return on capital weakens and shareholders won’t be smiling. If they operate the companies they own poorly, the whole entity suffers equally.

The rough return on new invested capital, as I presented above, is approx. 10% after taxes. Small organic growth nudges the figure slightly upward, perhaps to 12%. Without taking on debt, the company’s growth rate is thus 12% over time.

That might not necessarily sound high if you have growers like Palantir in mind. But 12% is a strong figure if you can maintain it for a long time. Guess what Microsoft’s average revenue growth has been for the last 25 years? 10%! No more than that.

And serial acquirers have good opportunities to continue this kind of growth for a very long time, because there is plenty to buy in the SME field and for now, economies as a whole are growing. For many companies, as they grow in size, sensible investment targets run out and they turn into cash cows, or they start consolidating a mature industry with large and often expensive acquisitions. In other words, they turn into laggards, and even the best ones often become “arch-laggards.” With a serial acquirer, if the team and owners know their stuff (the owners choose the team), this transformation into an arch-laggard can be postponed for even decades.

15 Likes

Good discussion. I’ll add to the ROCE% discussion that, as I understand it, in IFRS accounting, goodwill is not automatically amortized but is instead “tested” (for impairment). If the acquired company were to then go bankrupt for one reason or another or, for example, shrink significantly, the goodwill would have to be written down.

However, in IFRS accounting for acquisitions, part of the purchase price is allocated not only to goodwill but also to things like customer contracts and trademarks, which in turn are amortized (PPA amortizations) over a certain period. Thus, the portion of the purchase price allocated to these customer contracts and trademarks is amortized in the income statement, even if their actual value doesn’t necessarily decrease. For this reason, serial acquirers are usually tracked using EBITA instead of EBIT, because the “A” component includes these PPA amortizations, which do not affect cash flow.

Consequently, by buying companies at 8x EBITA, one gets a static pre-tax return on capital of approximately 12.5% (1/8). Then, if the company develops favorably organically—by raising prices or other capital-light means over, say, the next 10 years—the profit component grows, but the invested capital for that specific company decreases within the group. In this case, the original 12.5% pre-tax return can grow significantly, depending indeed on that organic development. Doing this successfully for long enough, the entire group’s ROCE% should gradually tick upwards, as it has done in Röko’s case.

On the one hand, this is just accounting fluff, but it partly explains why more mature acquirers can typically have a higher ROCE/ROIC. After all, every euro of that original purchase price was paid from cash flow. Verneri already summarized well what actually matters here. One could actually add to this that the amount of cash flow the company reinvests also matters. If a company pays out, say, 30% in dividends, it cannot grow as fast if other factors (leverage, acquisition multiples, organic development) are identical. Luckily for us, Röko does not pay dividends ![]()

So, in my opinion, the 15% growth targeted by Röko is possible with appropriate leverage and by paying approx. 8x EBITA for companies, provided they grow organically even faster than inflation with stable margins. This 15% is starting to be near the maximum unless one finds incredible organic success stories, buys at significantly lower multiples (e.g., turnaround companies in a PE style), or prints shares recklessly. When it comes to serial acquirers, I personally spend the most time thinking about which companies can sustain this “moderate” ~15% growth for as long as possible. Miracles happen with this kind of disciplined approach over, say, a couple of decades. So, for me at least, time is the most important thing in these. Such 10-15% growth over several decades is, however, an absolutely phenomenal performance that only a few can achieve.

16 Likes

@jp199 makes a very good point: as a result of IFRS, part of the purchase price flows through the income statement as PPA amortizations, which can mechanically improve ROCE (assuming operational performance does not deteriorate).

I have been trying to evaluate how to better measure the “true” ROCE of serial acquirers. Based on this, I have decided to adjust the invested capital by adding back the accumulated amortization of intangible assets found in the notes to the financial statements.

In Röko’s case, according to the 2025 annual report, the accumulated amortization was 895 mSEK, so I add this item to the invested capital in my own calculations. Below is a screenshot from Röko’s notes (note 15).

9 Likes