I think Röko (or other “perpetual” owners) has certain advantages at the negotiating table with SMEs. While PE guys in their puffer vests or suits would be coming to the family business office after the transaction to straighten out EBITDAs and give advice, Röko instead gives entrepreneurs full autonomy to work.

With this approach, Röko specifically looks for SMEs where the entrepreneur-owner and/or other key personnel would stay on to run the business with an entrepreneurial spirit (as minority owners). This approach can be very attractive to a seller in certain deal situations, but not all.

For example, if a family business had a successor in the next generation or among key personnel, but they didn’t have the personal risk tolerance to buy 100% at once, Röko could be an attractive option. In this case, the next generation/key personnel can stay and run the company as minority owners with entrepreneurial freedom, while Röko carries the risks of the majority owner. The seller can trust that the company will preserve its brand, culture, and employees in the eternal home provided by Röko. Meanwhile, in PE, an aggressive five-year plan would be hammered out to cover those outrageous costs and generate returns on top.

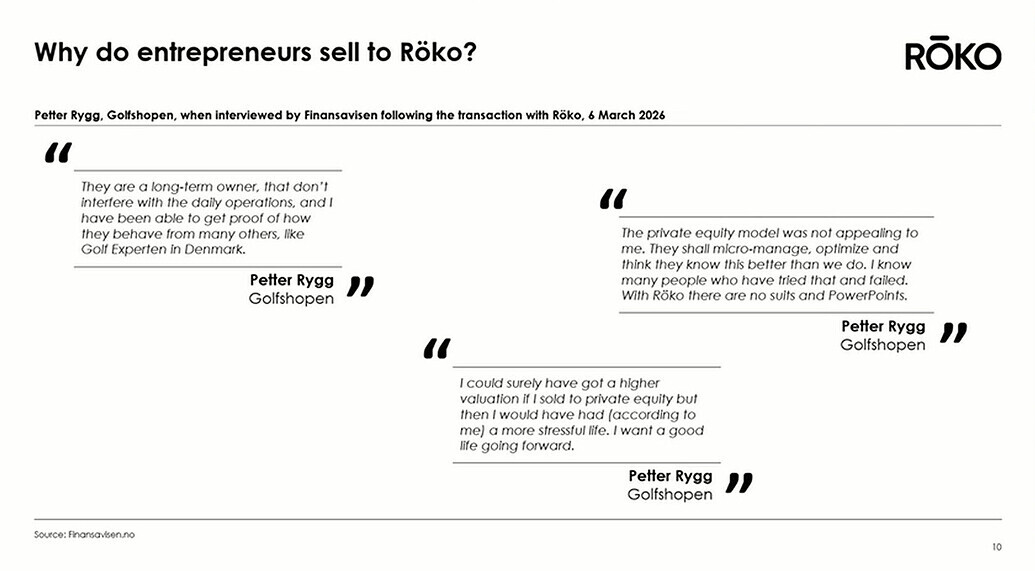

This is a bit of “soft” stuff, but for some SMEs and entrepreneurs, these can be very personal and important matters. An entrepreneur may know all their employees very well—they might even be family members or relatives—and would primarily want to preserve their jobs under a new owner. Röko can also be an option for an entrepreneur to diversify their ownership well before retirement age to provide security for their family. They sell the majority to Röko and then run the business as a minority owner, just like before. There were some fun highlights on this slide, where an entrepreneur who recently sold their company to Röko was interviewed in a magazine:

I agree regarding the position of a Röko investor. It requires guts and a truly long-term investment strategy, for which every investor is, of course, responsible to themselves. For a completely rational Röko investor, continuous liquidity is just an opportunity to buy more as the expected return improves, even if the sellers are those small-cap funds with their paper-handed owners. As you said, Mr. Market has factored in the value creation potential of such a business quite efficiently, so the opportunities brought by volatility and a long holding period must be utilized to achieve good returns.

In my opinion, Röko’s remuneration and incentives are generally in a completely different ballpark considering the position of a retail investor compared to PE. In practice, the Röko team only has fixed salaries, and everyone has significant share ownership.

You still have to do a bit of stock picking among serial acquirers, as there are plenty of them listed nowadays, often with a very similar-looking narrative ![]() That mediocrity and seediness, at least in terms of returns, might be left behind over time

That mediocrity and seediness, at least in terms of returns, might be left behind over time ![]() But yeah, you won’t get the next fast multi-bagger out of this no matter how hard you try, unless Mr. Market goes crazy again—so this is boring!

But yeah, you won’t get the next fast multi-bagger out of this no matter how hard you try, unless Mr. Market goes crazy again—so this is boring!