Welcome to the thread! I’ll answer based on my understanding after familiarizing myself with the company. A big disclaimer: I’ve been buying shares for some time on a declining price, and my position is such that my thoughts are guaranteed to be biased towards optimism. So, it’s worth listening to answers from someone more pessimistic or digging for answers from other sources ![]() This is, however, excellent practice to respond when someone questions things a bit, so a big thank you!

This is, however, excellent practice to respond when someone questions things a bit, so a big thank you!

My understanding is that Röko only acquires companies where the entrepreneurs remaining as minority owners do not intend to retire anytime soon. It could be that an entrepreneur sells to Röko long before retirement age to diversify their assets, if it’s already clear there are no successors among heirs, for example, or simply to provide security for their family.

Another example could be a situation where an entrepreneur is about to retire, and the company’s operational activities have already been significantly managed by other members of the management team/key personnel for a good while. This group might be interested in continuing, but their risk tolerance isn’t enough to buy 100% of an SME all at once. A similar situation can occur in a family business’s generational change.

In such cases, Röko takes on the risks of the main owner, but the company’s key personnel/next generation essentially get to run the business with entrepreneurial freedom, while minority stakes keep incentives aligned. Röko pays dividends to minorities, so such a deal can be very attractive to many. Entrepreneurial freedom and “drive,” but with controlled risk and appropriate reward for good results. In the best-case scenario, Röko can be on the same journey with minority owners for a very, very long time.

If and when minorities eventually exercise their options and are about to retire, Röko primarily recruits a successor internally. If none is found, they search externally. My understanding is that the option arrangements made will last at least beyond the medium term (3-5 years?), even if the entrepreneur plans to leave as soon as possible.

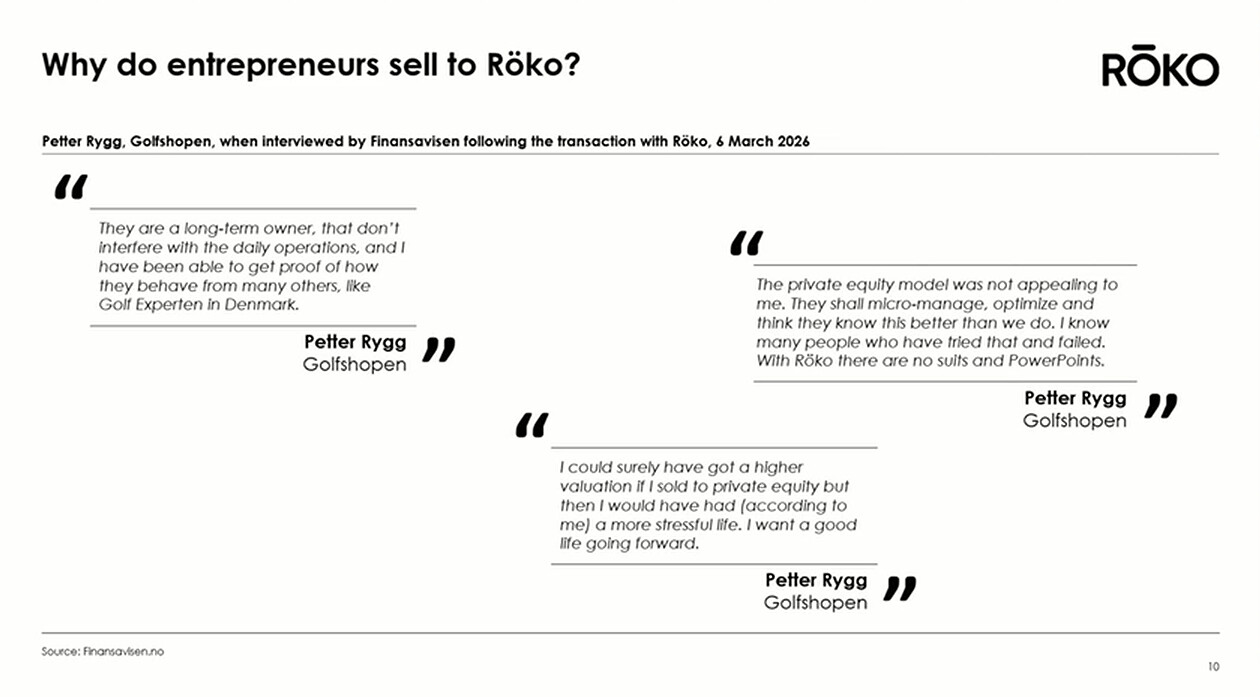

This brings us to how this entire model requires really strong trust between the parties. Röko’s management must also have excellent “people skills” to handle these diverse, often very intimate situations where an entrepreneur is partly giving up their life’s work and beloved “child.” Think about how these SME entrepreneurs have often practically put all their eggs in one basket, and 100% of their wealth can be in that company built from scratch ![]() Well, this went a bit off-topic, but the intention was to emphasize that price is not always the deciding factor, and an entrepreneur can remain a minority owner for a long time. In this regard, a recent presentation had a good slide:

Well, this went a bit off-topic, but the intention was to emphasize that price is not always the deciding factor, and an entrepreneur can remain a minority owner for a long time. In this regard, a recent presentation had a good slide:

This brings us to why the serial acquirer model is so effective. In principle, the model can thrive with very modest organic growth that beats inflation, e.g., 3-5% over time is enough for good results. Of course, higher organic growth is always better if it comes with a good return on capital.

If companies are then acquired at, say, 8x EBITA, that implies a return on capital of approximately 12.5% before taxes, with businesses being capital-light (=low capex). If such a 12.5% return can be achieved over decades by reinvesting, say, 80-90% of the cash flow, the company can grow by approximately 10% through acquisitions. Add to this 3-5% organic development, and the compounding machine, at its best, grinds out about 15% annual growth. Not bad if it can be done for decades. At this rate, the company quadruples in about 10 years.

This is why niche companies with limited growth opportunities but pricing power fit the model so well. In the best-case scenario, organic growth can then be achieved through price increases ![]() And price increases are good because they don’t require capex

And price increases are good because they don’t require capex ![]() So a compounder doesn’t need compounders within it, but rather cash flow with low maintenance investments! Constellation Software, for example, is a textbook example of this with its thousands of software companies. Of course, many serial acquirers also have organic success stories within them, which has given the machine even more momentum.

So a compounder doesn’t need compounders within it, but rather cash flow with low maintenance investments! Constellation Software, for example, is a textbook example of this with its thousands of software companies. Of course, many serial acquirers also have organic success stories within them, which has given the machine even more momentum.

On the other hand, organic growth opportunities should not be stifled either, but their returns on capital and profitability must be very strictly compared to the returns achievable through acquisitions. In other words, disciplined capital allocation. Of course, you can’t buy any slowly dwindling companies in sunset industries; fundamentally, they should still exist decades from now. A good aspect of the model is also that sometimes you can let a business wither if something happens to it. It doesn’t break the machine if there are dozens of companies.

[quote=“Osinkohaukka, post:45, topic:68981”]

And what kind of a player is this new CEO? I haven’t had a chance to watch Bladh’s interviews yet, but Karlsson certainly hypes him up a lot. With Bladh becoming CEO, the CFO position is taken by a 27-year-old guy named Douglas Kressner. He could, of course, be a very capable person, but I find it a bit strange that someone almost fresh out of university takes on the CFO role of a listed company. In quite a few companies, the CFO has a very strategic role. Of course, there are differences between companies in the scope and criticality of that role, but this decision puzzles me a bit.

[/quote]I’ve understood that when Fredrik and Tomas founded Röko, they deliberately wanted to bring in very passionate and talented young people from the start. For example, Johan has been involved for 7 years, starting from the second acquisition. In my opinion, Röko has been built very patiently from the beginning, so potential successors have been identified well in advance. In a company like this, however, culture is so hugely important that it would be good for successors to come from within the company. This is how successors were nurtured, for example, at Berkshire and elsewhere. Röko is, of course, still a very young company, but it originated from a model that was probably already refined during the founders’ previous tenures ![]() In this way, culture and continuity were built from the beginning with a long-term perspective and very clear goals.

In this way, culture and continuity were built from the beginning with a long-term perspective and very clear goals.