“A significant improvement in results from a loss-making comparison period and Q1 is a given”

The forecasts for Raute didn’t quite hit the mark. Poor performance.

“A significant improvement in results from a loss-making comparison period and Q1 is a given”

The forecasts for Raute didn’t quite hit the mark. Poor performance.

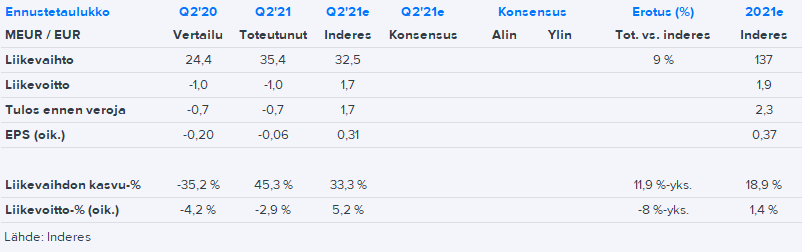

Indeed. Revenue was good and higher than forecasts, and the mix seems quite good (good revenue in services). Even with these essentially high-quality ingredients, a clear loss was generated, as costs accumulated significantly more than forecasts on every line. This will require some thought for a while. On the bright side, orders were good, but they cannot turn the report to profit.

edit: I have Rautes’s quarterly income statements from Q1’14 onwards in my accounting records. Higher personnel costs and other operating expenses than Q2 have only been recorded in Q4’18, when revenue was EUR 54 million. A lot has been done during the quarter.

In a way, it sounded good and could turn out well, but this is precisely where the weakness of the manufacturing industry in special situations (I mean components and raw materials, where prices have risen and have been offered at a fixed price) becomes apparent. In such cases, one is certainly partly at the mercy of luck as to how much and in which direction those prices will change.

I personally don’t currently own any other “real” manufacturing company besides Harvia, but in a certain sense, I would be interested in cyclical specialists in their field like Raute.

Are the large projects still ongoing, on top of which these smaller, more profitable projects could accumulate at some point?

In the spring, it was reported that Finnish companies Uponor and Raute could benefit from the US construction boom (and the infrastructure package?). Is this still just speculation, or are there some concrete prospects here?

This, in my opinion, is comparing apples and oranges.

Uponor manufactures and sells products to wholesalers and stores.

Raute manufactures and sells machines that produce machines for manufacturing products.

Excerpts from old news

https://www.inderes.fi/fi/tiedotteet/raute-oyj-rautelle-noin-16-miljoonan-euron-tilaus-venajalle

In addition, Segezha Group has a large birch plywood mill in Galich, Kostroma region, Russia, in the installation and commissioning phase, to which Raute is also supplying the production process (stock exchange release 1.10.2019).

https://www.inderes.fi/fi/tiedotteet/rautelle-noin-55-miljoonan-euron-tilaus-venajalle

Machinery and equipment will be delivered between the end of 2021 and the beginning of 2022. Production at the plywood mill will start during 2022.

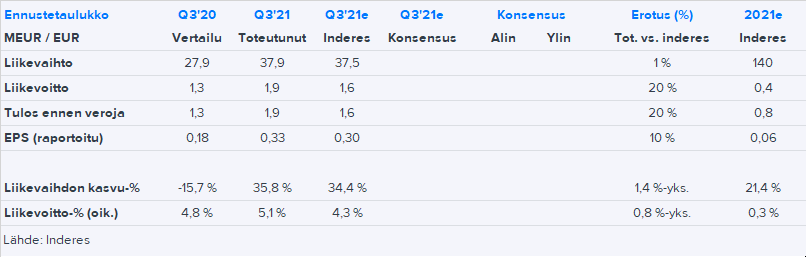

Of Segezha’s large plywood project, only the tail end is likely left in the order book, while the large Plitwood project is almost entirely there. The Lithuanian LVL project is also practically entirely in the order book, and currently the same applies to Segezha’s fresh July deal (this was not yet in the Q2 end order book). On top of that, there’s a good number of smaller projects and services (incl. modernizations). In my opinion, Raute’s order book is relatively normal, and its gross profit structure should be already good these days. There are so many large projects involved that it’s probably not a particularly good structure yet, but this order book is no longer dominated by a single large project, which has been the situation for the past year and a bit.

Overall, Raute’s Q2 report was, in my opinion, disappointing due to challenges in profitability. The path to good profitability is also not at all clear due to inflation and delay risks in the rest of the year, and on the other hand, profitability has been somewhat symptomatic even earlier. Earnings forecasts came down despite positive market developments, and at the same time, return expectations also melted away. The morning comment is here.

It’s hard to be surprised that no one is in control of the big picture.

Based on a Twitter sample, Rautes’s (Rauate) CEO’s passions seem to lie elsewhere than in the company.

Raute announced yesterday that it had cleared its Russian order book and secured an EUR 18 million plywood mill order from Red October. The comment is here. Raute is securing a good share of orders from Russia due to its strong market position and highly competitive technology, and the entire order book may not yet be cleared.

The revenue from the project secured yesterday is expected to be recognized mostly in 2022, and there are no acute pressure for changes in the forecasts, considering the growth expectations already in the forecasts. Of course, the risk associated with next year’s forecasts, and thus the entire stock’s risk profile, decreases as the order backlog strengthens. In the near future, attention at Raute will largely focus on the margin the company will ultimately squeeze out of its high-level order backlog.

Metsä Group’s Äänekoski investment decision seems to lack a formal plan (hardly a problem). With a relatively high probability, Raute will get significant business from this next year and possibly in the coming years. The comment is here.

The Raute preview is here, the results will be published on Friday morning. Orders have probably come in quite well, but in the report, it is exceptionally interesting to see what kind of margin can be squeezed out of the order book.

I will interview Tapani before Friday’s event. If any question suggestions arise, I can pick them up from this thread as much as possible!

Q3 was a step in the right direction, but as the company CEO noted in their review, the level is not yet satisfactory. Orders were strong and the order book is at a record level. The market remains very polarized, with Western countries and Russia pulling ahead, while developing countries are struggling. However, it is not yet time to breathe a sigh of relief regarding margins, as risks to the profitability of sold orders due to inflation were flagged. On the other hand, with new orders, Raute’s “cost plus” pricing model is unlikely to face major difficulties. Overall, there are many moving parts in Raute (as well).

Question to @Antti_Viljakainen, Raute’s CEO: How has Raute performed in the challenging world of overflowing order books compared to its competitors? The demand for all kinds of wood products is currently absolutely insane, and sawmills are booming, so at least the market is really hot right now.

Uncle Masse, FA, Wood and Masse, two of today’s non-fossil, recyclable, and ultimately biodegradable hit products ![]()

![]()

The company started to pique my interest… are the risks related to the global economy higher, like with other cyclical stocks? The company’s small size concerns me, is the daily trading volume quite low?

All trends seem to be in Raute’s favor, and Inderes also sees the long game as interesting. It seems to hinge more on the fact that profitability expectations have not yet been met, and there have been some minor disappointments in this regard. Yes, the daily trading volume is small, so if you decide to invest, it’s worth noting.

I personally see this small size (and also the low trading volume) as a kind of opportunity. This stock hasn’t yet caught the “fever,” which you can tell by how little is written about it. I’ve been holding a small position in this for a few years, and I’m not in a hurry with this story.

Are there challenges in acquiring the desired amount from the market, or offloading a large block, when there simply isn’t enough supply on the bid/ask?

The Inderespodi (inderesPodi 64: Riskit osakesijoittamisessa - Inderes) discusses liquidity risk among other investment risks.

Thanks for the link! Good stuff in the podcast. I think many investors have the misconception that a company with low trading volume is riskier…

Raute issued a negative profit warning. The primary reason was the new accounting treatment for SaaS software (must be expensed, not capitalized), so this is not a particularly bad negative profit warning. Regardless of how it’s treated, the money leaves the account at the same time, and it’s just a matter of when the expense is recognized. The secondary reason was production problems caused by the coronavirus. What was peculiar about the negative profit warning was that Raute retroactively announced that it would recognize SaaS expenses for 2020 of €0.9 million. That doesn’t seem possible, so I don’t understand something in this whole picture.

It might also be an original interpretation of the possibility of capitalizing cloud services on the balance sheet.

Exactly.

My gut feeling is that I’ve seen such retrospective corrections sometimes. My memory doesn’t stretch to an example, though, and it’s not typical.

However, the BIG4 auditors and/or consultants (PWC for Raute, if I remember correctly) are involved, so I don’t believe there’s any fumbling with interpretations, even if this IFRS accounting requirement, too, doesn’t align with common sense. It’s interesting in itself because Raute isn’t the only company with an ERP project underway (Valmet and Digia come to mind at least), and no similar message has been heard from others yet. Perhaps it’s possible to circumvent this by putting ERP costs into adjusting items? Raute has guided its reported operating profit, so this couldn’t have avoided the unnecessary (and admittedly minor) negative.

Of course, Q4, adjusted for the accounting change, would have fallen short of our modest earnings forecasts. A long list of burdens was also mentioned in the release, and these ultimately eroded the margin more than we expected, even though we were anticipating a subdued end to the year.