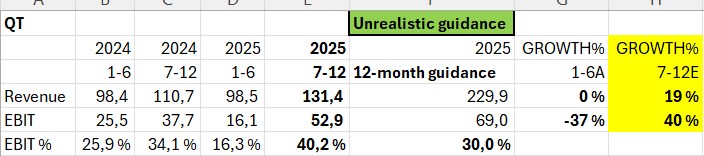

Revenue should grow by 19% year-over-year in the latter half of the year, and EBIT by 40%.

This way, the lower end of the guidance would be reached.

It’s hard to believe that even the lower end will be achieved.

Revenue should grow by 19% year-over-year in the latter half of the year, and EBIT by 40%.

This way, the lower end of the guidance would be reached.

It’s hard to believe that even the lower end will be achieved.

Surely, the company’s management should be asked when that growth will start coming again. Investing in this now is based on the assumption that at least reasonable growth is expected in the coming years. Now it comes to mind, was the previous acquisition made precisely for growth?

I don’t know the company well enough myself, but I’ve started to consider joining the ranks of owners someday. However, due to the main lines, this idea of buying shares is starting to get a bit bumpy. At least this now requires clarification for myself.

The report states the following in the CEO’s words:

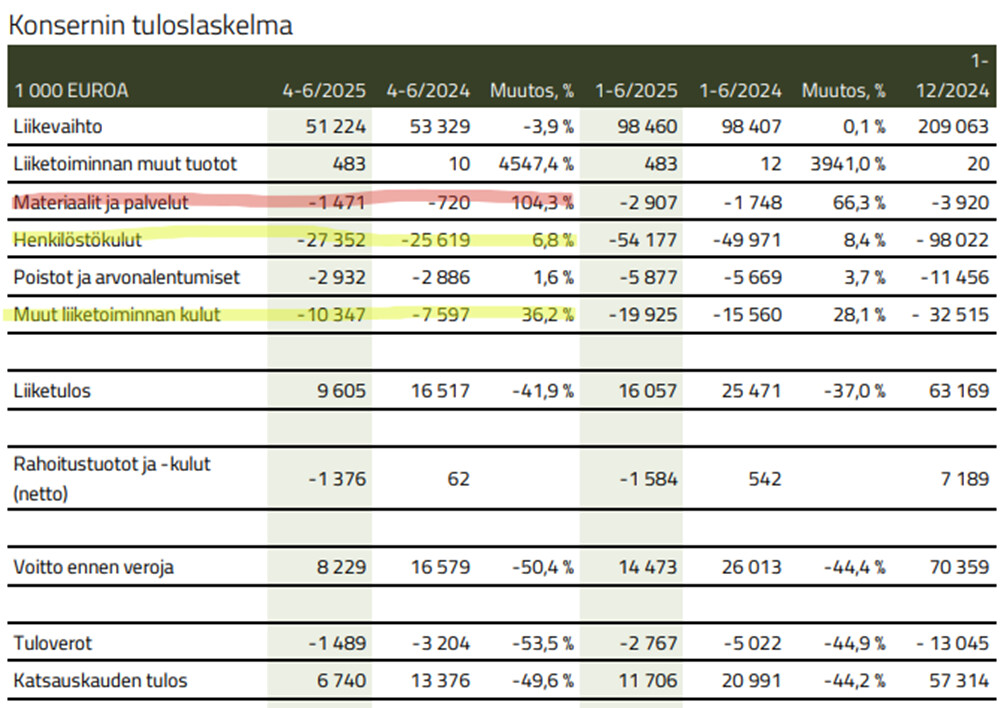

“Due to the decrease in revenue and increased personnel costs, operating profit decreased in the second quarter compared to the previous year.”

Then, when looking at the income statement, it doesn’t directly match this, as personnel costs rose by 6.8%, and by approximately 1.7 M euros in monetary terms. Operating profit thus weakened by 6.9 M euros, so this is not the only explanatory factor.

As a smaller expense item, materials and services increased by as much as 104.3%, bringing an additional cost of 0.8 M euros compared to last year. Quite a lot, but why?

And as a larger factor, other operating expenses grew by 36.2%, and 2.8 M euros. It has risen exceptionally much, but why?

Those who know the company better could tell whether this is some bump along the way, or if there is a slight change in the earning logic… or perhaps a bit of both? At least the sharp rise in those other operating expenses could indeed be temporary - or could it?

That was a terrible half-year review. Hopefully, in the earnings info, a lot of pressure will be put on Varelius regarding the problems. Hopefully, these problems are solely due to the prevailing general market situation. As @Passi (if I remember correctly) has already pointed out above, other companies aren’t doing any better either.

The report was weak, which was entirely expected as the trade war inevitably puts a brake on sales. In terms of revenue, from Qt’s forecast accuracy perspective, there was an unusually small deviation (-4%), and from this perspective, we didn’t take much more of a hit than expected, but this flowed (driven by higher-than-expected personnel costs) with leverage to the bottom line, where we were then 25-40% below forecasts.

Achieving the guidance at this H1 level certainly looks difficult; this will require at least a rapid launch of R&D projects for H2. We need to clarify what has been thought about this in the earnings info ![]()

![]()

For me too, it has been weighing on my mind for the past couple of quarters that Varelius is not being entirely honest about everything. What’s foremost in my mind is the Q1 excuse that revenue stalled because of the trade war. Most of the quarter had proceeded quite normally, and the worst phase was well into the second quarter already, so the explanation wasn’t entirely convincing. There are always external factors, but now it really feels like everything else is being blamed except their own actions. At least their communication and delivery could be improved.

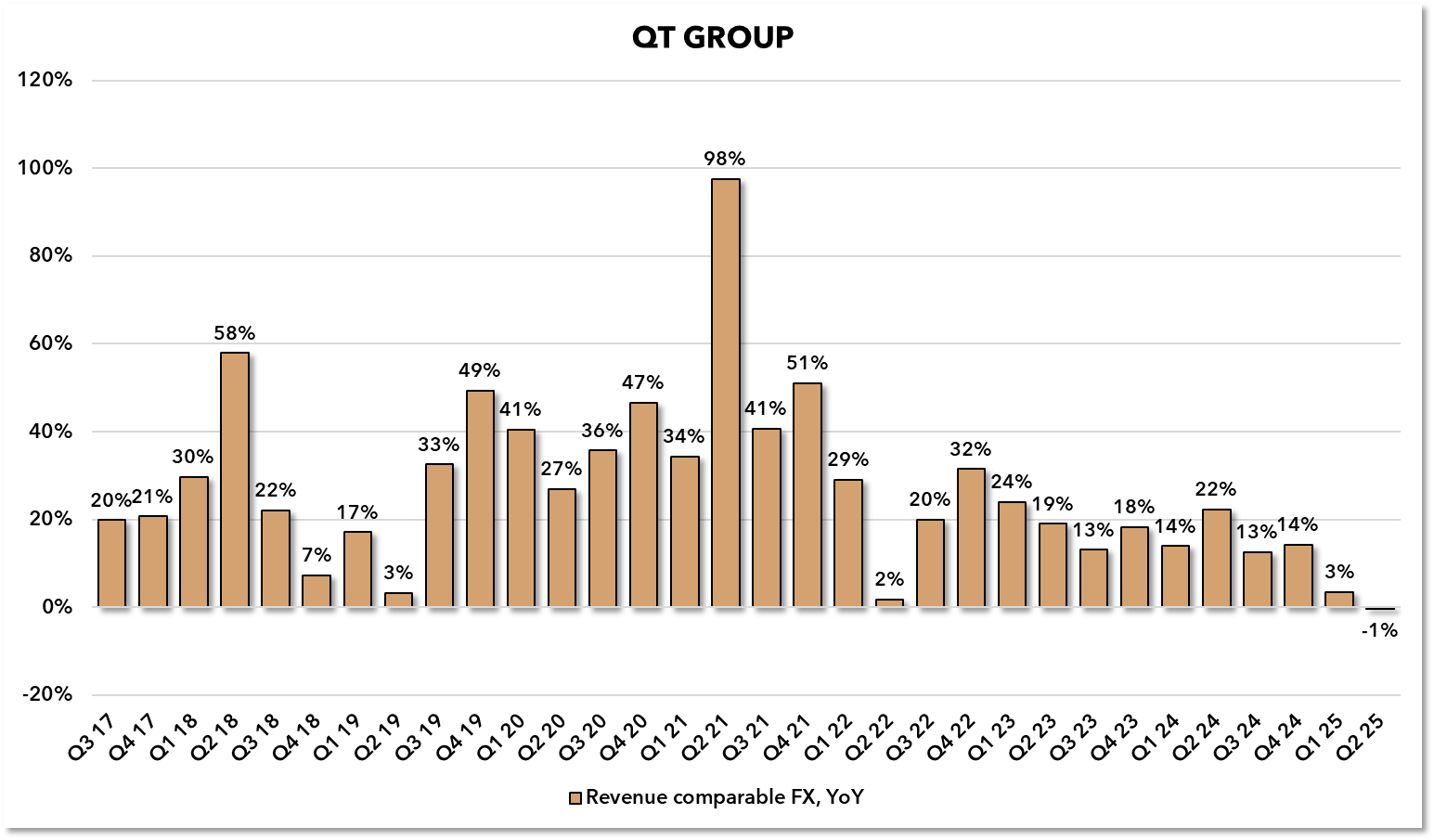

For the first time in the red since comparable currency-adjusted growth began to be reported in Q3 2017.

Is it a coincidence that the dismal Q2s have occurred every 3 years? Those years have been saved by an incredibly strong year-end, especially Q4. I’ll be interested to see how this year turns out.

The cliché about the trade war seems like a forced, universally applicable excuse. Tariffs remained unchanged for a quarter. The claim lacks concrete evidence.

Qt’s result (e.g., earnings per share collapsed) was abysmal.

It’s just that sales fell short. The customs complications certainly created uncertainty and a brake on investments.

How is there concrete evidence of this in Qt’s US market?

Now we are almost in the middle of Q3, so by now there should already be signs of improvement in sales for there to be any hope of reaching the current guidance. It looks quite bleak if this isn’t communicated in the webcast. If no improvement has been observed yet, then the rest of the year seems like a ‘hope for the best’ situation.

Could this line also include some one-off costs related to the acquisition (consulting fees, etc.)?

E.g., representation expenses, marketing expenses, travel expenses, purchased services..

So yes, it can probably be included.

What bothers me most is that if it’s stated that the weakness in results is due to personnel costs, and then if there were significant costs related to an acquisition or, for example, to that Qt World Summit event… and these are not then given as reasons for the weakness in results, can one then trust what the company management says about other matters? So if a policy is chosen not to disclose everything directly, and to hide things a bit, then surely that applies to everything the company says.

That result was ugly, but I certainly didn’t hesitate to buy more on the dip today. Pretty strong drivers for a few years, a new bigger acquisition in the pipeline, and surely the world economy will clear up a bit from this, which will have positive effects.

In itself, a perfectly valid question was thrown around on the forum earlier: “what kind of growth company is this, anyway?” Probably not a COVID-era growth company, but a growing company nonetheless.

There’s a lot of buzz here about H1’s situation.

At this point, the focus should be shifted to whether QT’s investment case is broken?

If the case isn’t broken, the price is quite juicy.

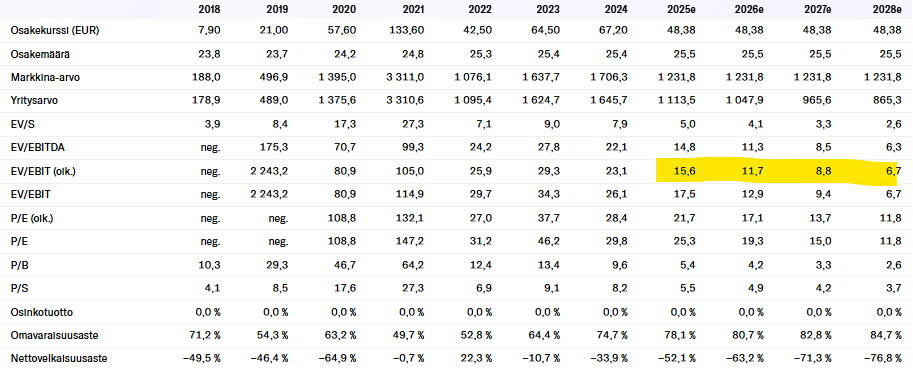

EV is 1100M€

If we drop Inderes’s 71M€ EBIT level to 65M€. —> EV/EBIT ~17

What kind of growth from here on?

If QT doesn’t grow at all from here on, by changing cost discipline, EBIT can be brought to a cautious ~5%/a growth. —> 2028 EV/Ebit 14

Current price is OK.

If growth is ~5%, EBIT will also grow ~5% (or more) —> 2028 EV/Ebit 14

Current price is OK.

If growth is ~10%, EBIT will grow ~10% (or more) —> 2028 EV/EBIT ~12

Starting to be cheap.

If EBIT growth is ~20%/a as in current forecasts. —> 2028 EV/EBIT ~7

Cheap as dirt.

So, the current market seems to think that QT will grow 0-5%/a in the coming years.

I’d be happy to hear views on whether to believe more in analysts’ 20%/a EBIT growth or the market’s perceived 5%/a EBIT growth.

What factors have changed the case such that the previously estimated growth potential is no longer realistic in the longer term?

Just to ask as someone who doesn’t know… You used adjusted figures in the example, I have the reported figures below.

During H1/25, operating profit was 9.4 M euros (16.1 M € vs. 25.5 M) from the corresponding period of the previous year, and revenue remained the same. In turn, in H2/24, the company made an operating profit of 37.7 M euros.

And for QT to reach that 65 M euro operating profit… considering the comparable figure, and that in Inderes’ calculations, reported and comparable figures differ by 8 M €, and taking this into account → QT would need to make a comparable operating profit of 40.9 M € in H2/25. Without knowing the company better, this is probably possible but perhaps doesn’t sound realistic!?

So what makes one expect that H2/25 would be better than H2/24 even though the beginning of 2025 has been clearly weaker than last year? This is an essential question for my potential investment case, and I’m trying to get an answer to it.

Edit:

Even though I am very critical for several reasons, I nevertheless bought a very small opening position (and purchases are probably somewhat ongoing). The drop is so steep that I see a possibility for a bounce in the coming days.

EBITA is a good metric for QT. A goodwill amortization of €2M is made every quarter.

Considering EBITA, old forecasts for Q3-4:

Q1 €8.5M

Q2 €11.6M

Q3e €12.7M

Q4e €35.1M

2025e €67.9M

EBITA for H2/24 was €41.7M

That €65M would require approx. 7.7% EBITA growth for H2.

Given the current momentum, this might be challenging, but if QT itself didn’t foresee any growth for H2, they should have naturally issued a negative outlook already today. Of course, that doesn’t eliminate the risk of a negative outlook, and even that €65M realization would be a cause for a negative outlook.

In the negative guidance issued in January this year, it was stated to be due to large deals shifting to this year:

The company’s weaker growth than previously guided is mainly due to the fact that at the end of 2024, the company was negotiating several significant deals, of which more than estimated shifted to 2025 and therefore are not yet reflected in the 2024 results.

As I recall, in the Q1 webcast, it was said about these that they are not yet coming in Q2. Hopefully, these will be asked about in the QA section of the current webcast, whether they are coming during H2, as was stated earlier in the year.

So, just guessing… Now that the guidance wasn’t lowered, management knows that H2 is solid, and this aforementioned expensive event has provided a better outlook for the rest of the year & 2026.